The physical bank bill rate and the 3 month BBSW both increased by 3bp to 2.07%. Both rates are now at a 57bps margin to the official cash rate. There has been quite a bit of commentary on the gap between BBSW and the expected path of RBA rate increases recently but the consensus seems to be there is nothing to worry about…

The gradient of the government bond yield curve steepened as yields rose along the curve and the swap rates moved in a broadly similar manner with some minor differences. The 1 year swap gained 5bps to 2.02%. 3 year, 5 year and 10 year rates each increased by 6bps to 2.28%, 2.63% and 2.93% respectively while the 15 year rate gained 5bps to 3.10%.

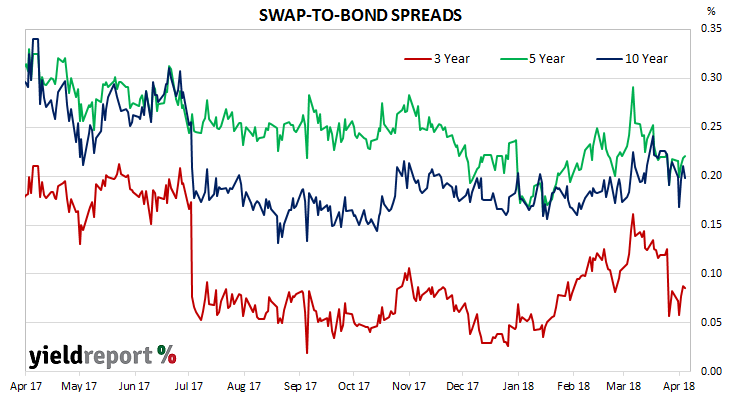

As a result, swap-to-bond spreads were a little wider at the front of the curve and a little tighter at the long end. The 3 year spread gained 1bp to 9bps, the 5 year spread was unchanged at 22bps and the 10 year spread tightened by 1bp to 20bps .

AFMA BBSW - SWAP RATES

| TERM TO MATURITY | Closing Rate | Δ WEEK | Δ MONTH |

|---|---|---|---|

| 30 Day | 1.87 | 0.03 | 0.16 |

| 90 Day | 2.07 | 0.03 | 0.27 |

| 180 Day | 2.16 | 0.03 | 0.20 |

| 1 Year | 2.02 | 0.05 | 0.15 |

| 3 Year | 2.28 | 0.06 | 0.12 |

| 5 Year | 2.63 | 0.06 | 0.08 |

| 10 Year | 2.93 | 0.06 | 0.02 |

| 15 Year | 3.10 | 0.05 | -0.01 |