Summary:

After two months of relative calm, Wall Street has been jolted by renewed credit concerns. The collapses of First Brands Group and Tricolour Holdings, followed by fraud-related write-downs at Zions Bancorp and Western Alliance, wiped more than $100 billion from U.S. bank valuations in a single day, reigniting fears of hidden credit losses. Despite this, the S&P 500 gained 1.7% for the week, extending a rally that’s added $28 trillion to global equities, helped by President Trump’s retreat from tariff threats. Yet volatility is rising—high-yield bond spreads widened 25 bps to 2.92%, and $3 billion flowed out of junk bond funds, signalling investor unease.

The VVIX, a measure of volatility-of-volatility, reached its highest since April, while tail-risk hedging demand spiked to a six-month high. Still, corporate credit fundamentals appear stronger than in past cycles. Goldman Sachs notes that even the high-yield segment is “less junky than ever,” with safer issuers dominating public bond markets as weaker firms shift to private debt. However, many investors feel undercompensated for corporate debt’s thin yields and are shifting toward equities or government bonds.

While inflows remain robust, analysts warn that any sustained outflows could trigger a “massive panic,” underscoring the market’s fragile balance between confidence and caution.

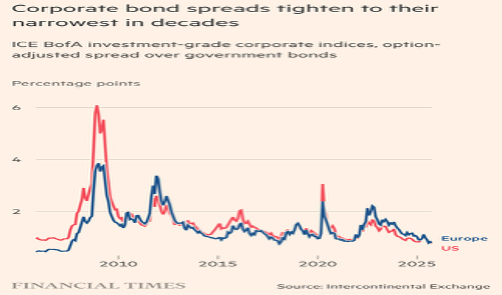

Figure 1: US & European Corporate Bond Yield Spreads

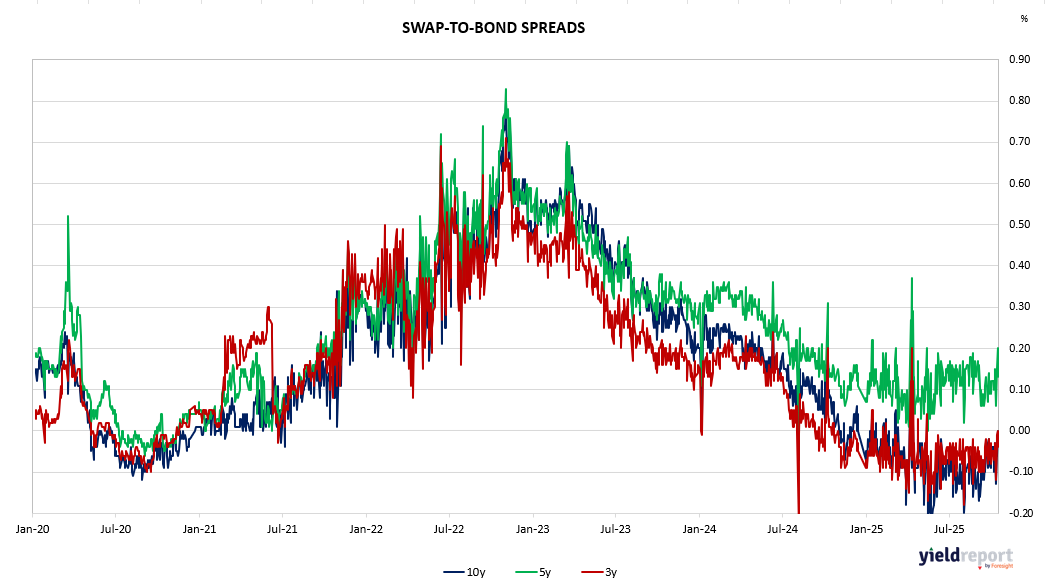

Figure 2: Australian Swap to Bond Spreads