Summary:

Just as we noted previously, directionally, Australian bond yields, both corporate and government, have since the beginning of the year being set by the direction of the US bond market. Tuesday provided no better indication than this. Despite the RBA cut, the 10-year government bond yield and, more notably, the more interest rate policy sensitive 2-year government bond yield increased 10 and 9 basis points, respectively. Over the course of the week, yields on the 10-year note increased 5 basis points to 4.50% after peaking at 4.57% earlier in the, near its highest level in over a month.

Flash PMI figures released on Friday indicated continued expansion in Australia’s business activity in February, supported by growth in both manufacturing and services sectors. Meanwhile, earlier data released on Thursday showed that the country’s labour market remained strong in January, complicating the case for further interest rate cuts.

Following the hawkish commentary from the RBA on Tuesday and again Thursday, the market materially repriced interest rate expectations. The market is now implying only a 10% probability of another rate cut in April and suggests just 40bps of easing for 2025, equivalent to fewer than two rate cuts.

So what we can probably take away from last week is that Australian corporate yields are likely to remain range-bound over the foreseeable future, and at elevated yields, given the tenor of the economic data we are seeing. Australia currently is not unlike the US – we are seeing a tug of war between what is generally solid and resilient economic data release yetgenerally solid and resilient economic data release is yet weak-ish consumer and business sentiment.

Furthermore, it is the elevated yield levels that have been fund manager demand for Australian government and corporate bonds. Over the last few weeks, we have noted the very high levels of oversubscription for both bond types, and notwithstanding the historically narrow spread levels. It is the latter that is the ‘tail’ risk for bonds, here in Australia and the US.

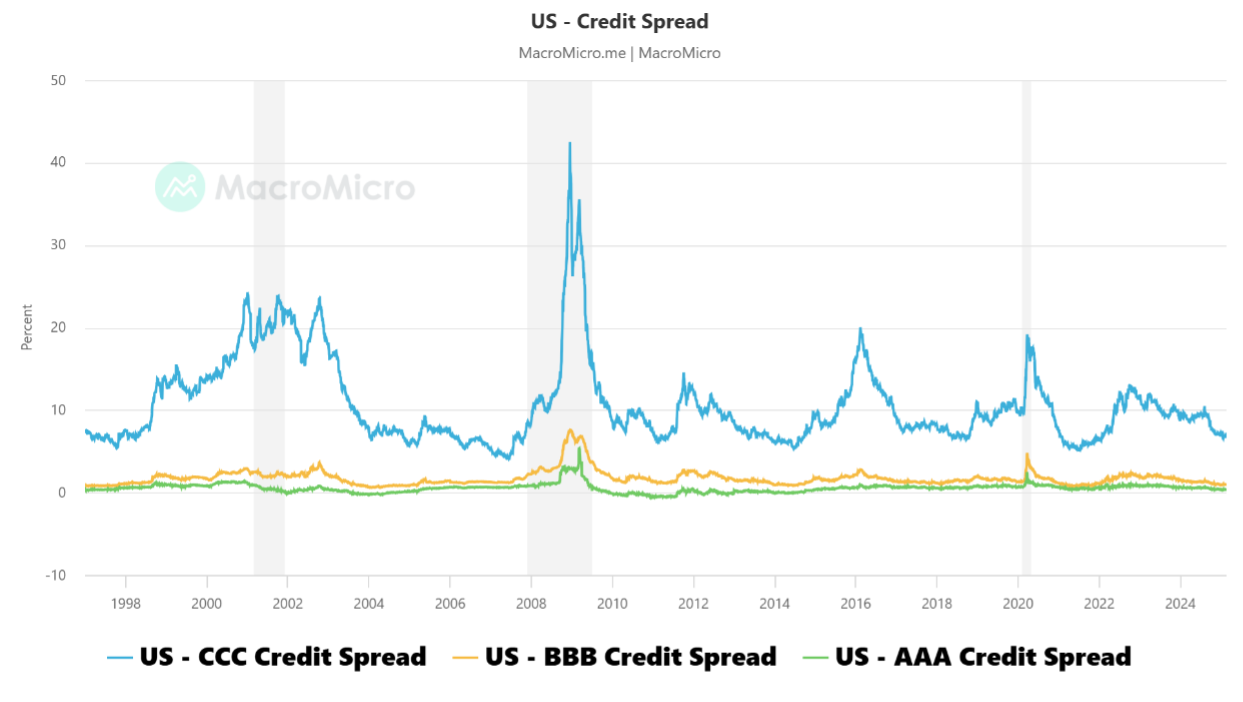

On the topic of spreads, refer to Exhibit 1. Spreads are historically narrow. On the corporate bond side, both IG and HY, spreads across the developed market landscape – e.g. US, Europe, Australia, credit spreads are at record lows and credit is undoubtedly expensive across the quality spectrum. Issue is – what is going to lead to a widening in spreads?? But investors should be mindful of the event risk implicit here.