Summary:

Australian Corporate Bond Primary Issuance Market Re-opens

Primary issuance of Australian corporate credit is open again. During the last two weeks there was one issuance. Sydney Airport printed a $600mn 7-year senior secured transaction. The deal was 1.7x over-subscribed. The 1.7x compares to an average of 2.4x over the last 12-months. Over this period, Australian corporate debt was experiencing record over-subscription, a trend replicated in the US. Given the recent volatility, it is not unexpected that demand levels are likely to be trimmed moving forward for a while

As we noted last week, global recession fears spooked financial markets two weeks ago with many questions left unanswered regarding the impact to company balance sheets. Positively, however, Australia was left relatively unscathed from a credit fundamental perspective with the Trump administration opting to impose the minimum 10% tariff on AU imports. For context, the US accounts for ~4% of Australia’s total exports, suggesting the first order impacts should be relatively manageable.

While the medium-term outlook remains clouded, particularly should larger trading partners (such as China and Japan) slow in terms of economic growth, international revenue (ex. New Zealand) from Australian issuers in the AusBond non-financial corporate universe appears moderate at approximately ~16% on our estimates. That said, international issuers make up around 22% of the non-financial corporate AusBond Credit index which has put greater upward pressure on the credit spread of the index.

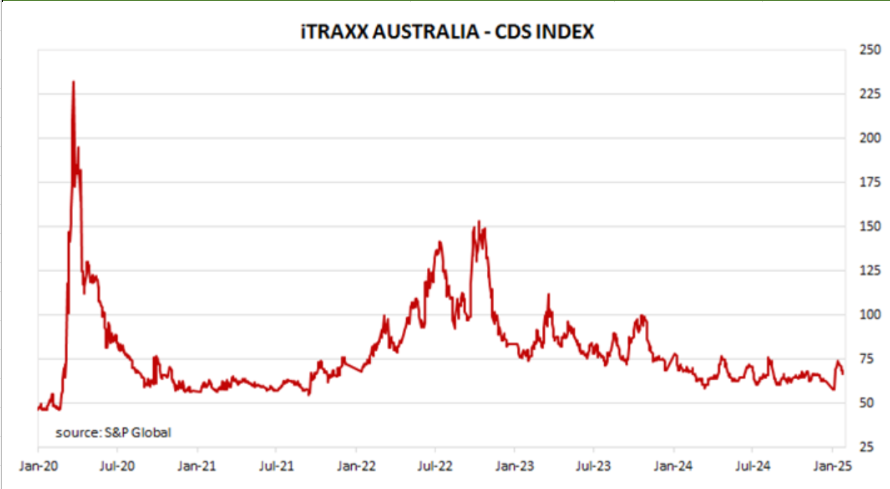

Spreads have tightened across the market since the peak reflecting the change/delay in the tariff policy implemented by the Trump administration, however, still remain broadly wider than year-to-date peaks.

The potential flow on impact of a domestic recession arising from the potential deterioration in economic conditions from key trading partners cannot be discounted, but we expect credit ratings to remain robust all else equal should Australian corporate credit remain in its bubble.

Meanwhile, in the US corporate bond market, all risk measures declined over the week. Spreads narrowed, both the Markit CDX North American Investment Grade Index and the Markit CDX North American High Yield Index (both which measure perceived credit risk) softened, and the high yield primary issuance opened up for the first time in 2 weeks.

In the Investment Grade space, despite the increase in volatility driven by US economic and policy uncertainty, investment grade credit will likely continue to demonstrate resilience compared to riskier asset classes such as US high yield and US equities.

In High Yield Credit and Bank Loans, worth considering the following. The financial consequences of efforts to improve US government efficiency are challenging to predict precisely, as there is no historical precedent for such measures. However, we are aware of potential implications for the aerospace, defence, and healthcare sectors. All sectors are recipients of large government contracts. This latter dynamic seems to have flown under the radar to a degree. There are 2.5x more employees in these government contract related sectors than in the government itself. For instance, lower Medicaid reimbursements could impact certain healthcare facilities. Pockets of stress.

|

Exhibit 1: Corporate Bonds: Swap-to-Bond Spreads |

|

Exhibit 2 : Corporate Bonds: Swap-to-Bond Spreads |