Summary:

Corporate bond markets demonstrated remarkable resilience following the Federal Reserve’s September rate cut, with investment-grade spreads compressing to multi-decade lows while issuance activity remained robust despite seasonal headwinds. The Fed’s 25 basis point “risk management cut” to 4.00%-4.25% steepened the Treasury curve and provided fresh momentum for corporate credit, with investment-grade spreads tightening to 72 basis points—levels not seen in nearly two decades.

Investment-grade corporates posted modest declines of -0.13% for the week but significantly outperformed similar-duration Treasuries by 18 basis points, underscoring the market’s appetite for credit risk over government paper. New issuance totaled $33.6 billion, slightly below forecasts but maintaining healthy momentum as corporations continue to capitalize on favorable borrowing conditions ahead of potential future rate cuts.

High-yield bonds rallied strongly throughout the week, benefiting from the Fed’s dovish pivot and continued investor search for yield in a lower-rate environment. The sector’s outperformance reflects growing confidence that the central bank’s easing cycle will support credit markets without signaling underlying economic distress.

Credit fundamentals remain supportive despite some cooling in corporate earnings growth. While corporate profits declined 2.9% in the first quarter—the largest drop since Q4 2020—overall profit levels remain elevated at $3.9 trillion compared to $2.9 trillion in late 2019. This backdrop has enabled continued rating agency upgrades, with investment-grade improvements outpacing downgrades by approximately 2:1.

The technical environment appears increasingly favorable as fund flows decelerated but remained positive at $3.7 billion, well below the four-week average of $6.9 billion. This moderation in inflows, paradoxically, may reduce pressure on spreads while maintaining sufficient demand to absorb new supply.

Looking ahead, market participants are positioned for continued spread compression given the Fed’s signaled intention for additional cuts. With officials projecting two more 25 basis point reductions by year-end and one additional cut in 2026, the interest rate backdrop remains supportive for credit assets. However, the market’s current pricing of deeper cuts than Fed projections suggest creates potential volatility if economic data fails to justify more aggressive easing.

September’s strong finish caps what has been a historically favorable period for corporate issuance, with companies successfully front-loading financing needs before potential fourth-quarter volatility. The combination of tight spreads, solid demand fundamentals, and a proactive Federal Reserve continues to create an optimal environment for both issuers seeking capital and investors pursuing income in an uncertain economic landscape

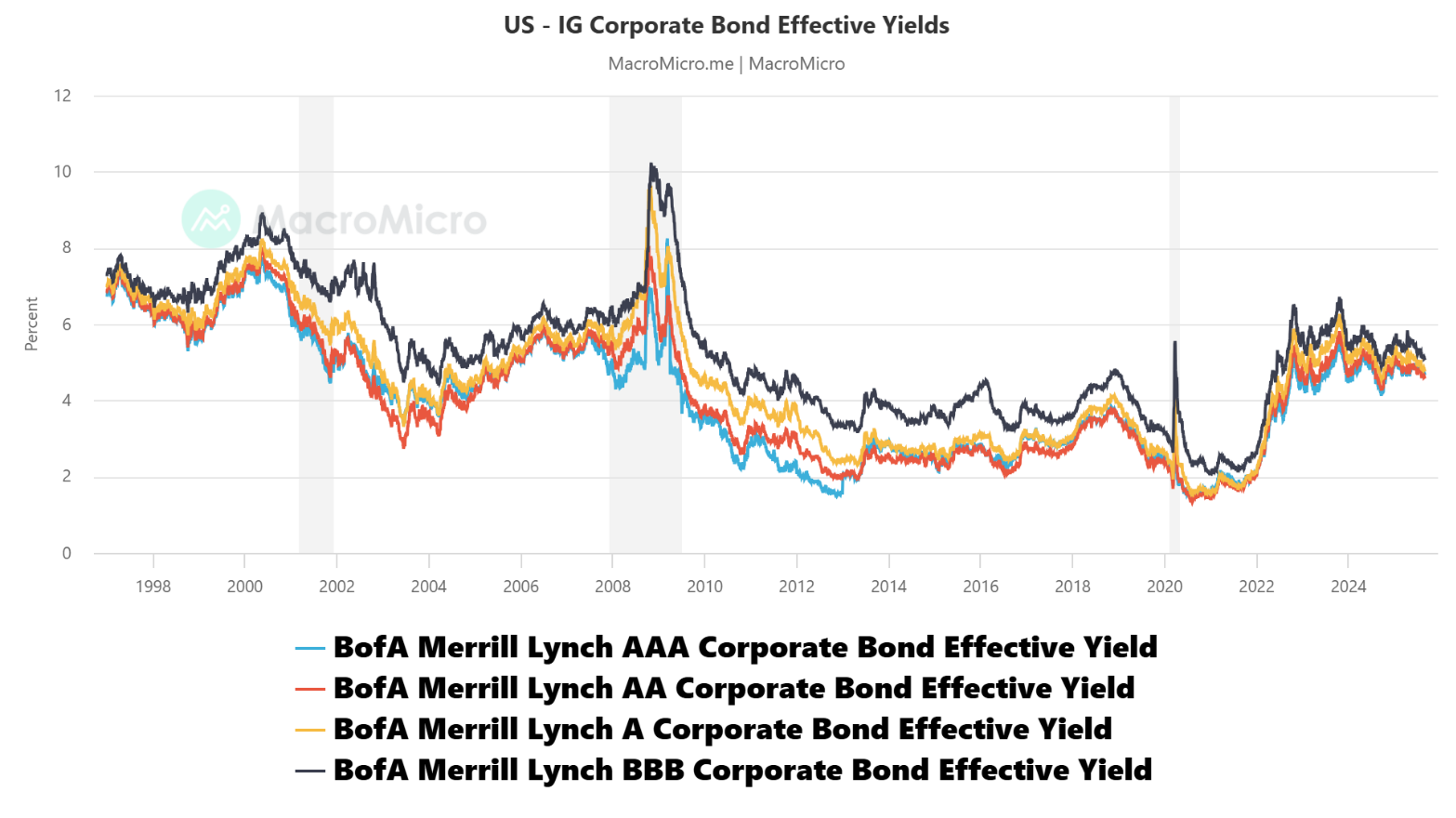

Figure 1- US Corporate Bonds Yields

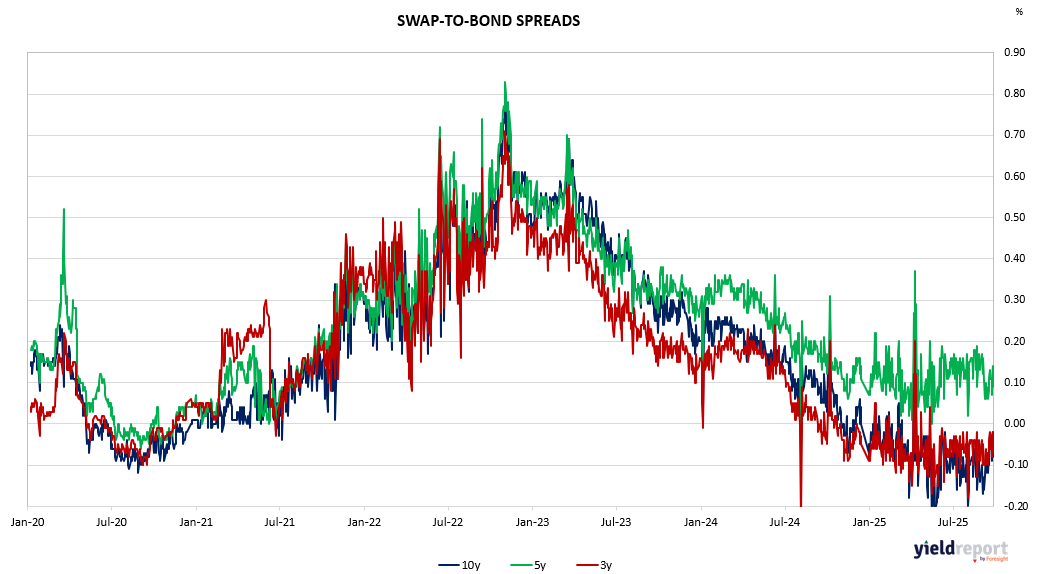

Figure 2: Australian Swap to Bond Spreads