Summary:

US corporate-bond valuations have surged to their highest level in nearly 30 years as investors rush to secure elevated yields amid expectations of Federal Reserve rate cuts next month. The extra yield, or spread, over Treasuries for investment-grade bonds fell to 73 basis points on Friday—the lowest since 1998—indicating bonds have become unusually expensive. Investors are prioritizing locking in current interest rates despite economic slowdown risks and ongoing trade tensions.

High-grade bond yields have averaged over 5% in the past three years after the Fed raised rates to combat post-pandemic inflation, attracting strong demand from institutional investors, pension funds, and insurers. Some previously cautious investors, scarred by the 2022 market rout, are now rushing in, driven by “FOMO” as opportunities to secure attractive yields diminish

The surge in demand is fueling record inflows into investment-grade bond funds, according to JPMorgan strategists, particularly as rate cuts are increasingly priced in for upcoming Federal Open Market Committee meetings. Limited new issuance adds further support, as companies delay borrowing in anticipation of lower rates. With lower supply and compressed spreads, traders find it increasingly challenging to identify profitable trades, highlighting the intensity of the current market rally.

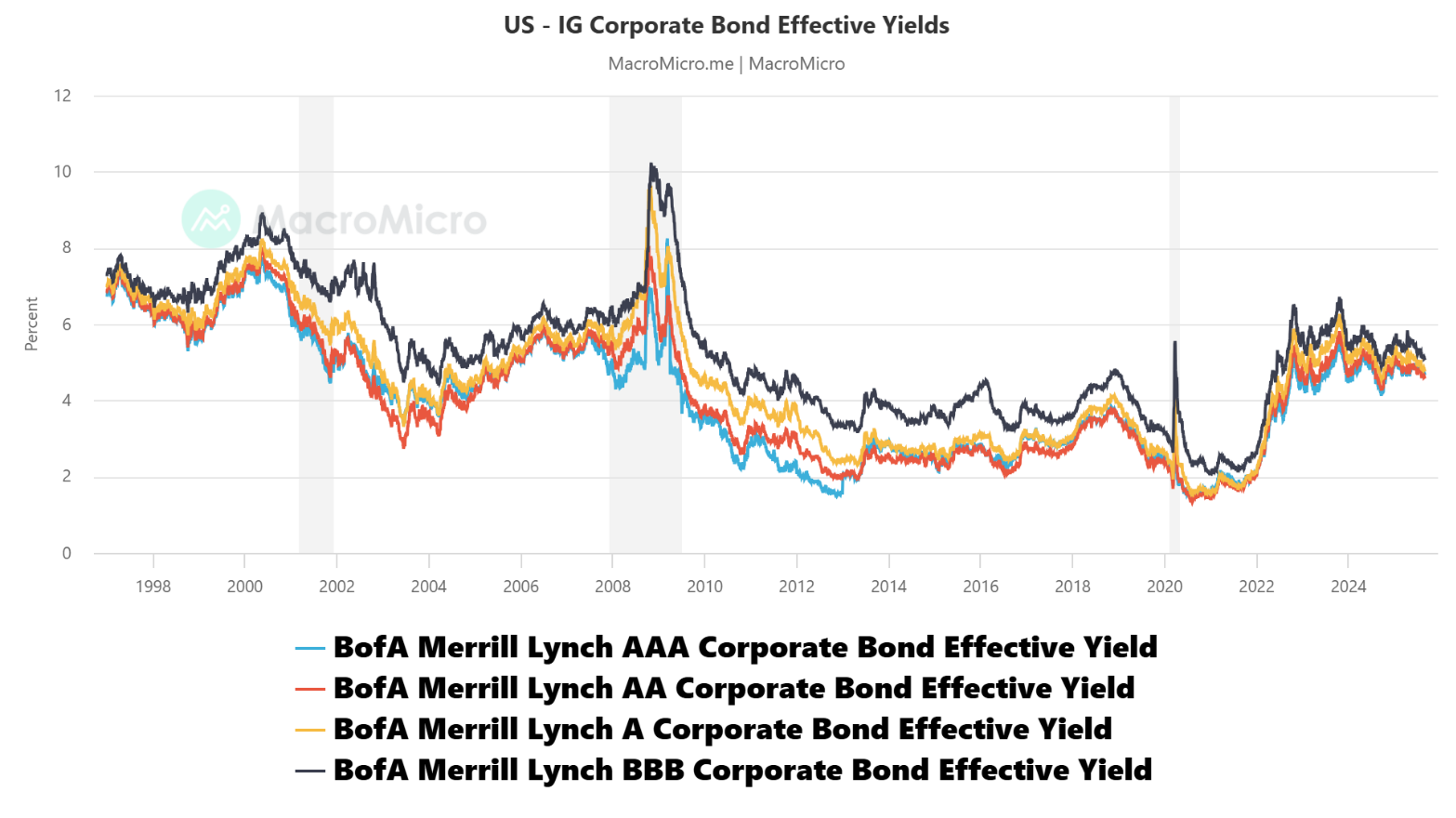

Figure 1 tracks effective yields on U.S. corporate bonds across rating categories—AAA, AA, A, and BBB—from 1997 to 2025. Overall, yields have shown cyclical patterns, rising during periods of economic stress and declining during stable or easing monetary policy phases. The early 2000s recession and the 2008 global financial crisis produced significant yield spikes, with BBB bonds consistently offering higher yields than higher-rated counterparts due to greater credit risk.

Yields declined steadily from 2009 through 2020, hitting historic lows during the pandemic as monetary stimulus compressed spreads. However, yields surged again in 2022 following aggressive Federal Reserve rate hikes to combat inflation, peaking near 6–7% before moderating slightly. Throughout the period, the spread between BBB and AAA bonds has persisted but remained relatively narrow during stable conditions. The chart underscores the sensitivity of corporate borrowing costs to macroeconomic cycles, monetary policy, and investor risk appetite.

Figure 1- US Corporate Bonds Yields

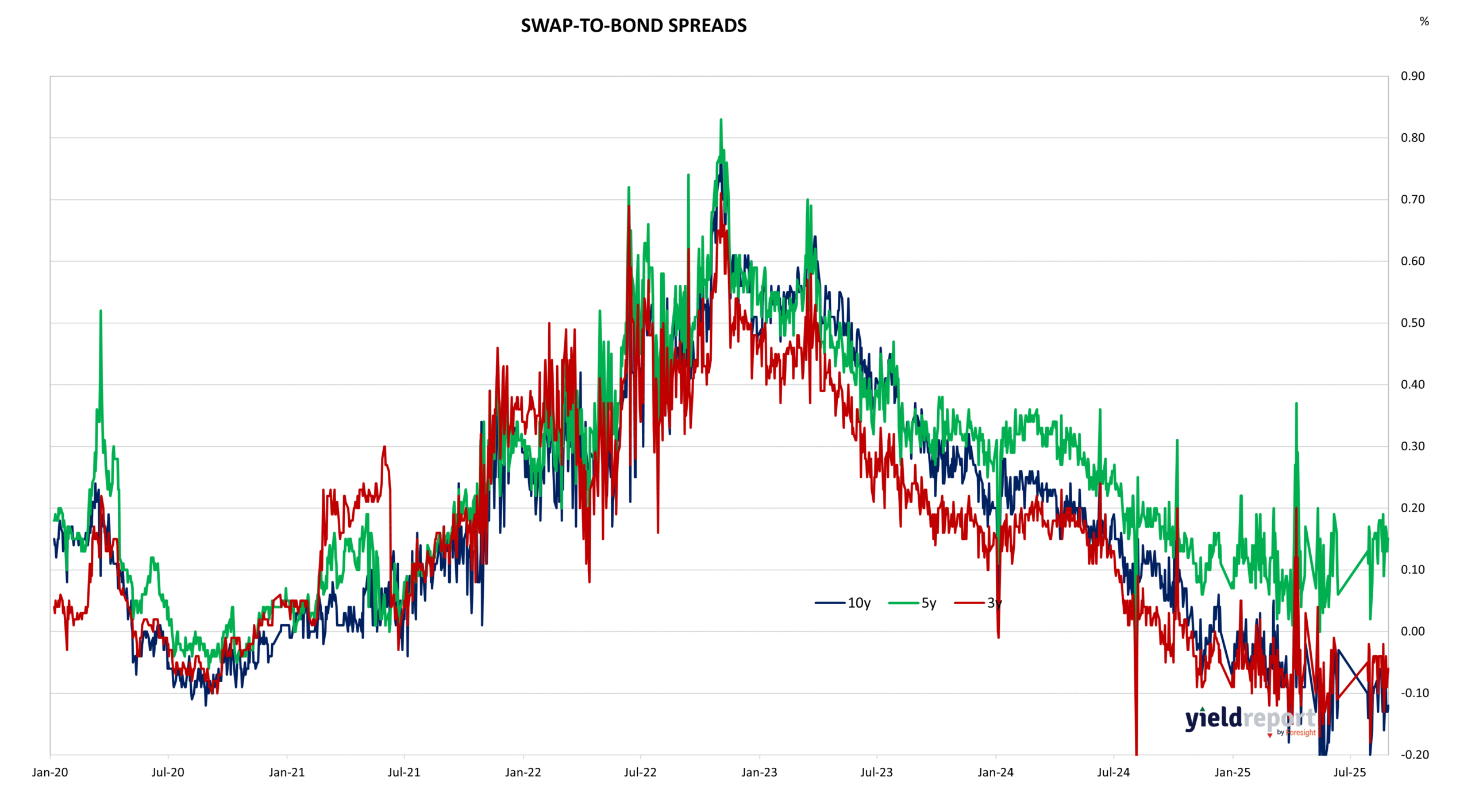

Figure 2: Australian Swap to Bond Spreads