JCB find the YieldReport to be an invaluable summary of all debt market activity. Whilst we are focussed on the highest grade bonds it is important to see what is..Angus Coote, Executive Director, JCB Active Bond Fund

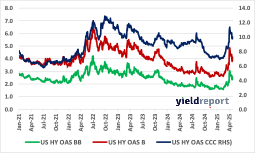

There were reasonably material increases in yield during the week in the US high yield market, reflecting the markets repricing of Fed rate cuts. By Thursday close, the high yield aggregate yield had increased 13 bps to 7.69%, the BB 12bps to 6.32%, the B 24bps to 7.84% and the CCC 15bps to 13.68%.

During the week, JP Morgan highlighted its bullish position on US high yield corporate bonds, noting the significant increase in spreads recently (lower valuations) as well as the fact that the high yield market has increased in quality over the past 10-15 years. It notes that High yield has matured over the past 10 – 15 years into a market with a larger proportion of BB-rated bonds (50% of the high yield market), increased secured debt issuance, now has lower duration (roughly 1.4 years lower since 2007) and far more conservative use of proceeds.

Despite recent market stress, credit fundamentals and technicals remain solid. Credit metrics for high yield for the fourth quarter have showed modest improvements off an already strong base. High yield issuers saw its first decline in leverage in four quarters with 15 of 18 sectors experiencing improvement.

Leverage metrics remain well below the long-term average. Interest coverage has also improved for the first time in more than two years. High yield spreads (as of 4/8/25) hit their highest level since October 2023 at 453 basis points (bps). The historical median 12-month forward total return for high yield with an index OAS range between 400-500 bps is 6.2% with a median excess return of 3.7%. While volatility could continue to be elevated in the short term, historically this has been an attractive entry point for a longer investment horizon.

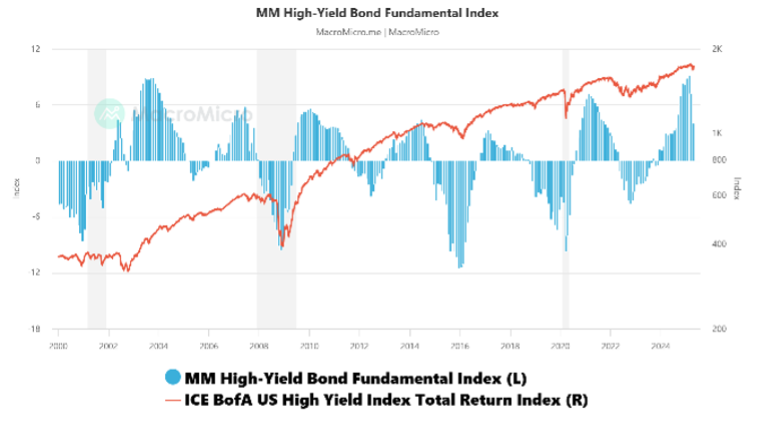

Figure 1: US High Yield Bond Fundamental Index

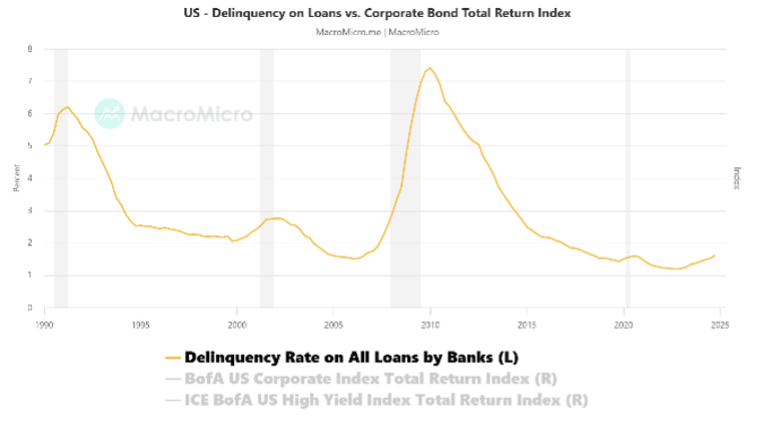

Figure 2: Delinquency on US Loans

In relation to Figure 1, the MM Fundamental Index for high-yield bonds is an integral index for assessing the fundamentals of junk bonds. When it goes up, the fundamentals of junk bonds are looking good. The Fundamental Index is updated with the monthly value on the last Friday of each month, and there may be subsequent changes due to data revisions for its constituent variables.

In relation to Figure 2, the US Fed surveys large commercial banks on the delinquency rates on loans and leases each quarter. As delinquency rates on loans and leases reflect the overall debt repayment capacity of businesses, delinquency rates serve as an important indicator of corporate bond defaults. The latest statistics are very solid: Delinquency Rate on All Loans by Banks (2024-Q4): 1.62%. Previous month: 1.52%.