Summary:

The Australian credit market saw steady demand and tight spreads over the final week of July. In the primary market, issuance was led by Dyno Nobel (formerly Incitec Pivot), which launched a dual-tranche AUD 500 million senior deal (BBB/Baa2) on 29 July. The offer was more than eight times oversubscribed, allowing Dyno to price the 7-year and 10-year tranches at swaps+155bp and +170bp, well inside initial guidancekanganews.com. This robust interest – driven by Dyno’s solid balance sheet and limited competing supply – highlights the strong appetite for high-grade corporate credit. (Transpower NZ also returned with both wholesale and retail Kangaroo bonds, reportedly drawing record retail demand.)

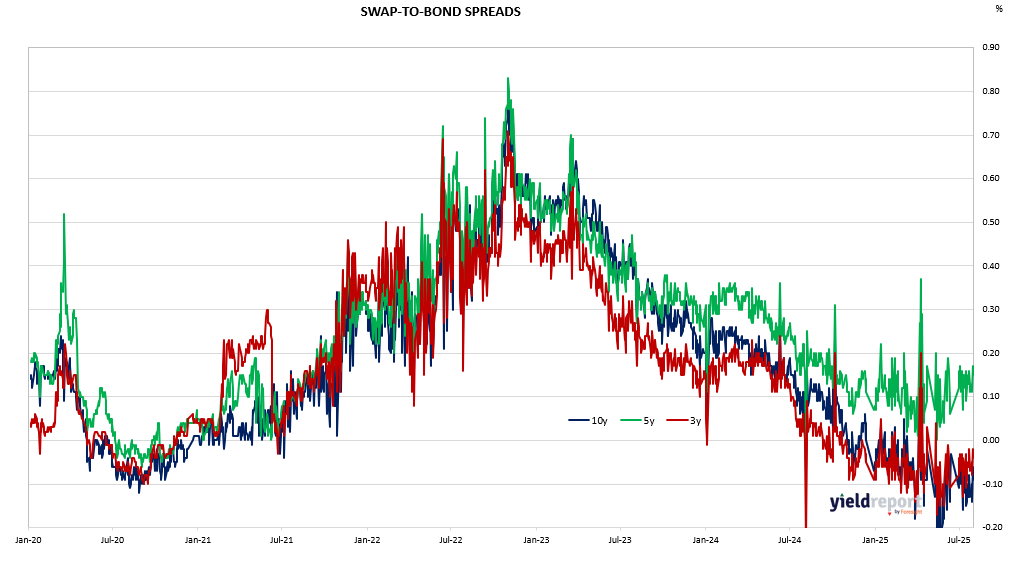

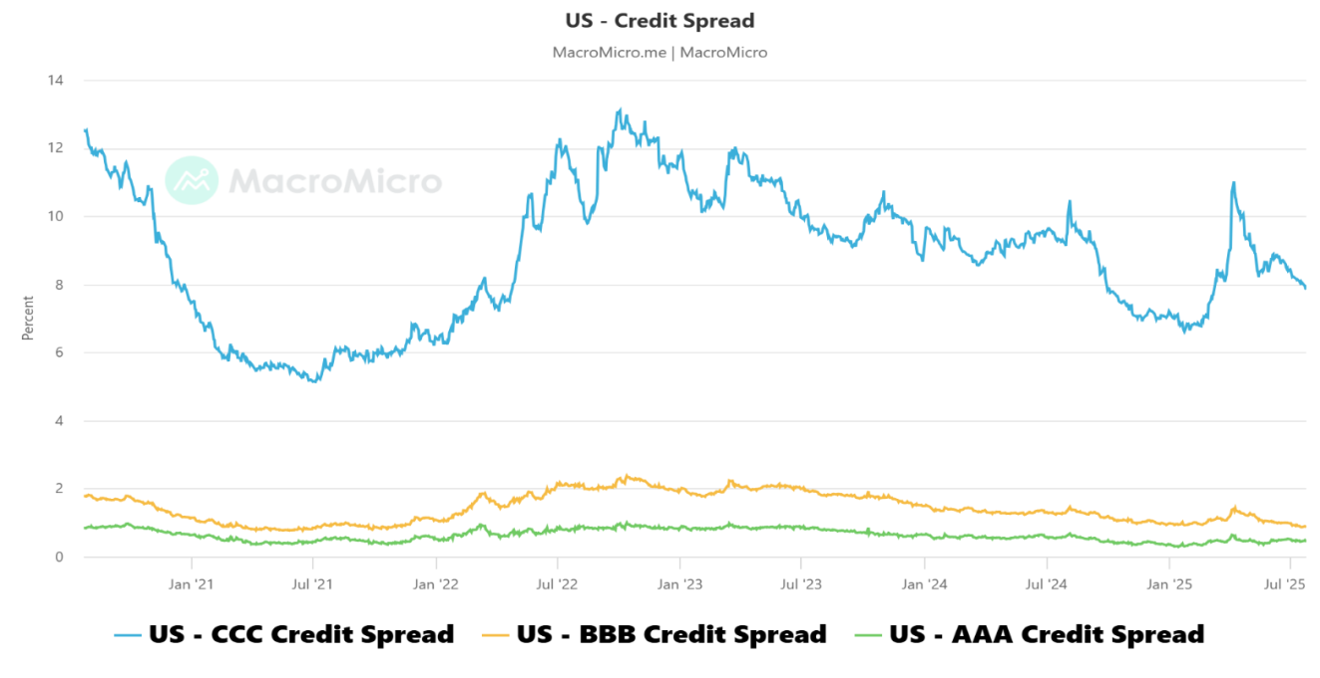

In the secondary market, major Australian investment-grade credits saw only modest yield moves. Global risk‑on sentiment (especially progress on US trade deals) pushed government bond yields slightly higher, but corporate yields rose less; for example, New South Wales Treasuries (“TCorp bonds”) 10‑year yields increased by less than sovereigns, narrowing the corporate spread to about 60 basis points – an 18‑month lowtcorp.nsw.gov.au. Overall, credit spreads were flat to tighter. Total return indices for Australian IG corporates were mildly positive over the week, as stable or slightly lower spreads offset the small rise in benchmark yields. Lower‑grade Australian spreads also remained contained; globally, even CCC‑rated corporate spreads have eased (US CCC spreads fell from ~10.5% in April to below 8% by late July).

Figure 1: US Corporate Bond Spreads

Figure 2: Australian Swap to Bond Spreads