Summary:

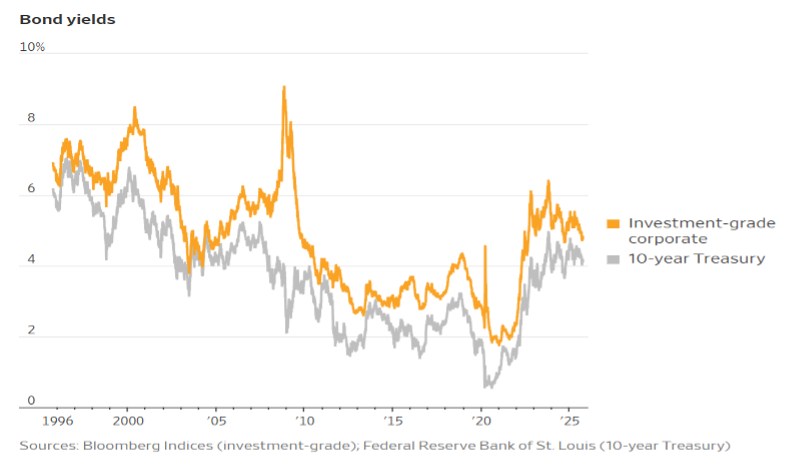

While U.S. stocks continue setting records, corporate bonds have become the real stars of financial markets in 2025. Despite the Federal Reserve beginning to cut interest rates, investor demand for company debt is soaring, driving investment-grade credit spreads—the premium over U.S. Treasurys—down to just 0.72 percentage points, the lowest since 1998. This reflects an extraordinary level of market confidence that major corporations won’t face credit downgrades or defaults anytime soon.

One key reason is that yields on corporate bonds remain historically attractive. Even though spreads are narrow, absolute yields are still higher than during the 2010s and early 2020s. As rates decline, investors—many of whom have been parked in money-market funds—are eager to lock in these elevated yields before they fall further. Memories of the near-zero interest rate era after 2008 are fresh, reinforcing the rush to secure long-term income while it lasts.

The economic backdrop also supports this optimism. Although job growth has slowed, unemployment remains low, and inflation pressures are easing, allowing the Fed to cut rates preemptively rather than reactively. Corporate balance sheets are strong, with high earnings-to-interest ratios indicating that firms can comfortably service their debts. This has reassured investors that corporate credit remains fundamentally sound.

Another major factor fuelling the rally is limited supply. Companies have been reluctant to issue new debt while borrowing costs remain elevated, resulting in a scarcity of both investment-grade and sub-investment-grade bonds. The modest increase in nonfinancial corporate debt and the slowdown in leveraged buyouts highlight this supply shortage.

This imbalance—strong demand meeting tight supply—has created a powerful tailwind for corporate bond prices. As Neha Khoda of Bank of America noted, the contraction in debt growth is normal during high-rate periods, and combined with persistent investor appetite, it has driven credit spreads to multi-decade lows. Together, these dynamics suggest that, at least for now, corporate bonds are outshining even the record-setting stock market as Wall Street’s preferred asset class.

Figure 1- US Corporate and 10-year Treasury Yields

Figure 2: Australian Swap to Bond Spreads