Summary: ACGB bond yields down in Australia; ACGB 10-year spread to US Treasury yield slips to -9bps; 10-year bond yields down in US, major European markets; $2.80 billion of bonds, notes issued by AOFM.

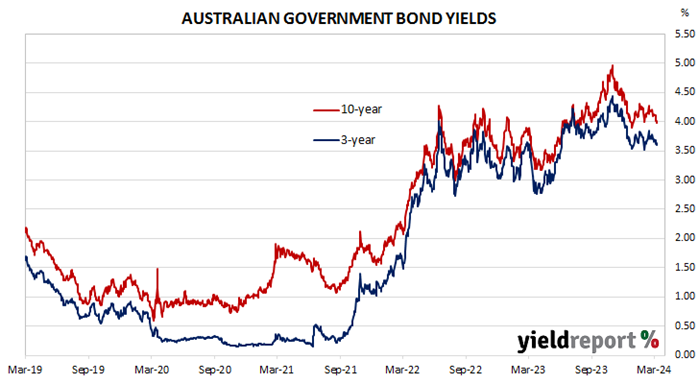

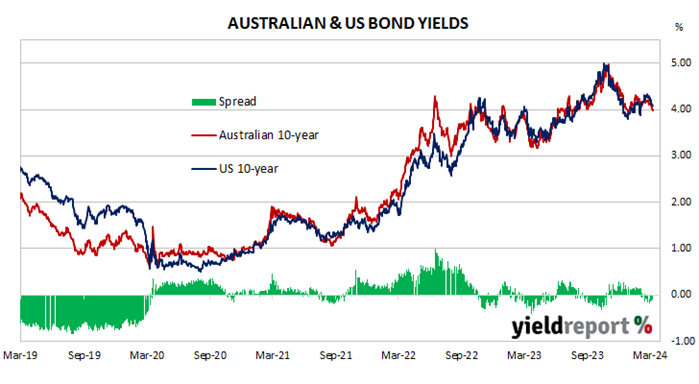

Locally, long-term ACGB yields fell through the entire week with the exception of Thursday when they finished steady. By the end of the week, the 3-year ACGB yield had lost 8bps to 3.60%, the 10-year yield had shed 12bps to 3.99% while the 20-year yield finished 14bps lower at 4.30%. The spread between US and Australian 10-year Treasury bond yields slipped from -8bps to -9bps.

Over in the US, 10-year bond yields started with a modest rise but then they fell through the remainder of the week.

The ISM’s February Services PMI was released on Tuesday. The index fell from 53.4 to 52.6, largely in line with expectations.

January’s JOLTS report was released the next day. Total quits, separations and openings all decreased and the quit rate ticked down from 2.2% to 2.1%.

At the end of the week, February’s non-farm payrolls report produced a rise in employment in excess of expectations for second consecutive month. However, the jobless rate increased from 3.7% to 3.9%, even as participation rate remained steady at 62.5%.

The US Fed’s Nowcast model was also updated as usual. The March 2024 quarter forecast was unchanged at 2.1%.

By this stage, the US 2-year Treasury bond yield had lost 6bps to 4.47%, the 10-year yield had shed 11bps to 4.08% while the 30-year yield finished 8bps lower at 4.25%.

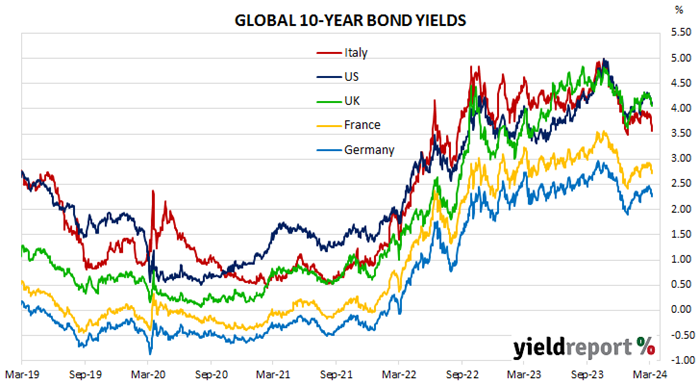

In major euro-zone markets, 10-year bond yields fell through the entire week.

It was a quiet week from a data point of view. However, the ECB Governing Council met on Thursday and left its various policy rates unchanged. It did, however, trim its inflation and GDP forecasts with inflation forecast to hit the ECB’s 2% target in 2025.

By the end of the week, the German 10-year bund yield had lost 16bps to 2.26% while the French 10-year OAT yield had shed 19bps to 2.71%. The Italian 10-year BTP yield fell by 31bps to 3.57% over the week while the British 10-year gilt yield finished 15bps lower at 4.06%.

The AOFM held the usual vanilla bond tender this week; $800 million of November 2029s were priced at a nominal yield of 3.74%. There were also two Treasury note tenders which raised $2.0 billion on a short-term basis.

The gross value of all bonds issued by the AOFM in the 2023/2024 financial year (not taking into account buy-backs or short-term Treasury note tenders) is $31.40 billion. There are currently $853.85 billion of Treasury bonds and $40.986 billion of Treasury index-linked bonds on issue. The next series to mature does so on 21 April 2024 when $35.90 billion worth of bonds are due. There are also $26.00 billion of short-term Treasury notes outstanding.