JCB find the YieldReport to be an invaluable summary of all debt market activity. Whilst we are focussed on the highest grade bonds it is important to see what is..Angus Coote, Executive Director, JCB Active Bond Fund

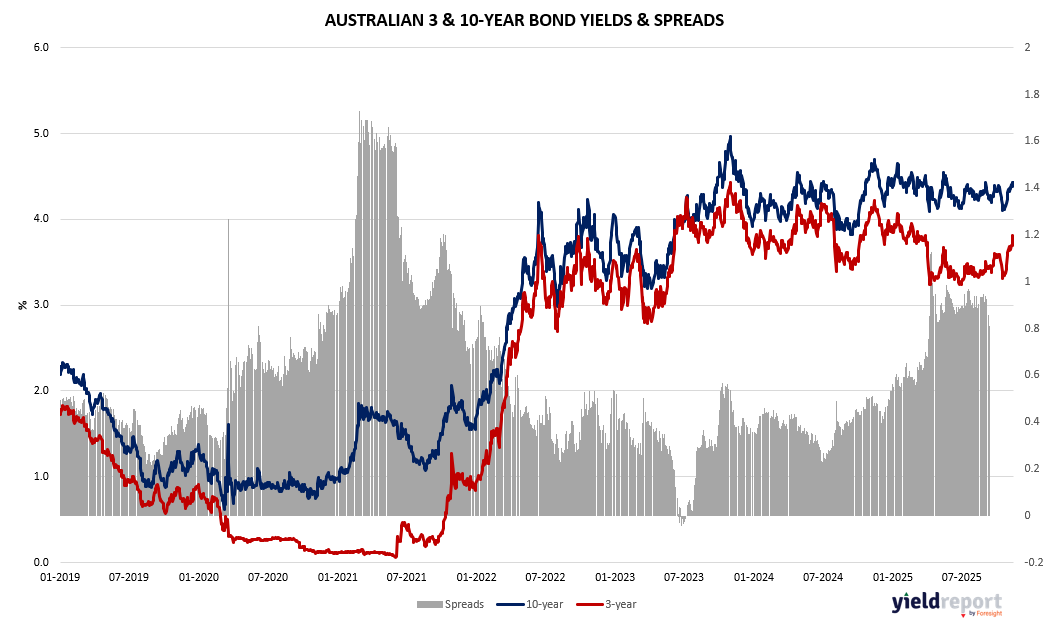

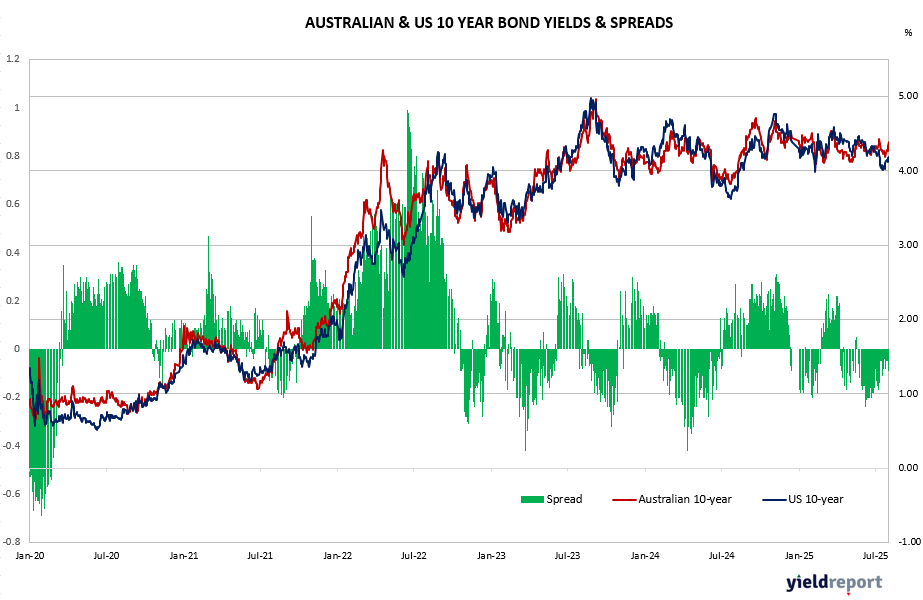

Australian and US bond yields moved slightly higher over the week as markets continued to reassess interest-rate expectations. In Australia, the 3-month BBSW held steady at 3.64%, while government bond yields rose across the curve, reflecting a firmer outlook for inflation and a reduced likelihood of near-term rate cuts. The 3-year yield increased 11 bps to 3.76%, the 10-year rose 7 bps to 4.44%, and the 30-year gained 4 bps to 5.03%, signalling upward pressure on long-dated borrowing costs. The cash rate remained unchanged at 3.60%.

US Treasury yields also edged higher, but the moves were more modest. The 2-year yield rose 2 bps to 3.59%, indicating slightly firmer expectations for the Federal Reserve’s policy path, while the 10-year and 30-year yields increased 3 bps each, reaching 4.13% and 4.73% respectively. These increases reflect continued resilience in US economic data and persistent inflation uncertainty.

The RBA kept the cash rate at 3.6% in its November 2025 meeting and signalled a more hawkish stance, with Governor Michele Bullock indicating that interest rates could move “in either direction” as inflation is now expected to remain above the 2–3% target range until the second half of 2026. Markets, which just a week earlier fully priced in a February 2026 cut, have sharply repriced expectations: the likelihood of a May cut has dropped to 69%, and bond futures no longer assume any cut this cycle. The RBA was surprised by stronger September-quarter inflation, with underlying inflation at 3%, and now places greater weight on restoring price stability over protecting employment.

Inflation is forecast to peak at 3.7% in mid-2026 before easing to 2.6% by mid-2027, while real wages are expected to fall through 2026. Bullock noted temporary drivers such as travel and fuel but warned of persistent pressures in housing and hospitality. Economists from NAB, EY and Fortlake viewed the tone as hawkish, suggesting cuts are unlikely without a clear economic deterioration. Analysts including Jonathan Kearns consider a February cut unrealistic without exceptionally low CPI. Some strategists even see potential for rate hikes in late 2026. Markets now view the next move as equally likely to be up as down, reflecting a shift from easing bias to cautious neutrality.