Summary: .

US government debt rallied over the week and across the curve, erasing past week declines. Tuesday was instrumental, after a Treasury Department official said a rule change was under consideration that could lower trading costs for banks. The US 10-year was down 4 bps to 4.34%, the US 3-year down 2 bps to 3.86%.

While the rule change mentioned by Deputy Treasury Secretary Michael Faulkender has been on the radar for years, his comments on the Supplementary Leverage Ratio, or SLR, helped drive yields lower to levels last seen during last week’s market turmoil.

On Wednesday, it was a Jerome Powell speech at the Economic Club of Chicago that triggered the main moves of the day. The key comment from Jerome Powell, and it was exactly when the market started to sell off, was when the Fed said it may have a problem with it’s dual mandate this year. Specifically, he stated that the economy will likely be “moving away” from both of its goals “probably for the balance of this year.” That is, higher inflation and higher unemployment (a stagflation scenario, and was written all over the conversation) and which would put the Fed between a rock and a hard place. He also stated that there is uncertainty about tariffs would lead to a one-off price impact or that the price impact would be more persistent. And finally, he reiterated that, with the current employment and inflation levels, the Fed is in no rush to move on rates. So, forget any Fed put, at least in the short term.

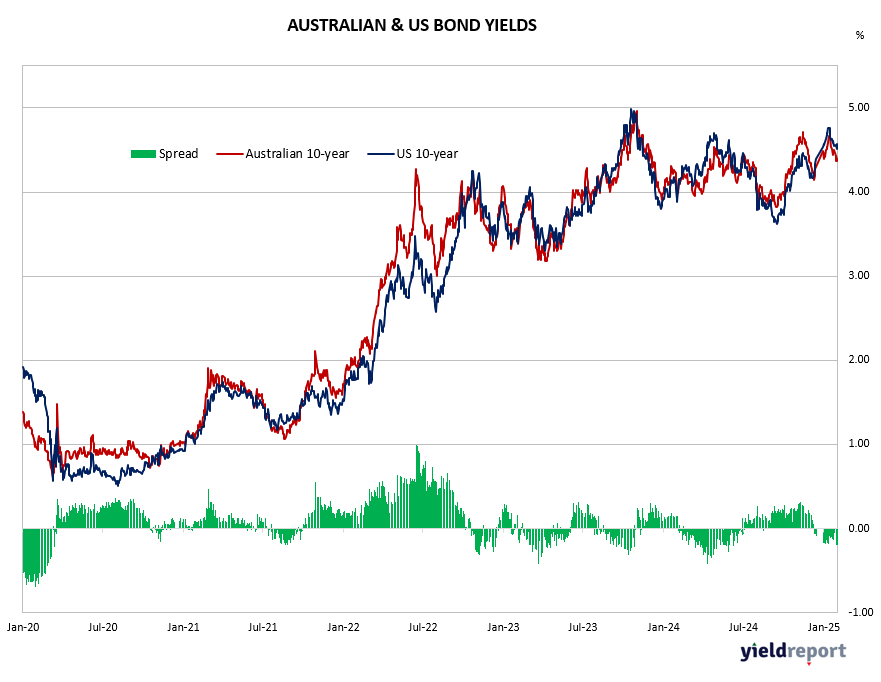

Investors also were motivated to buy longer-maturity Treasury debt at yield levels that offer the most compensation, relative to shorter-maturities, in more than a decade. The term premium increased to 71 basis points, last seen in September 2014. Term premiums have been on the rise as US economic policy becomes harder to predict. A gauge of policy uncertainty neared a record this month after President Donald Trump announced sweeping tariffs and then backtracked on some. Proposals for tax cuts and a potential need to increase the US government debt limit also contributed to the move. And this is notable in Australia, as per char chart below.

Many market watchers last week suggested that foreign powers including China were offloading their US Treasury holdings in retaliation for Trump’s tariffs, exacerbating the plunge in prices. But Ed Yardeni, the noted US economist, released a detailed note yesterday indicating the vast majority of selling had come from forced selling by hedge funds.

Meanwhile, higher Treasury yields are failing to support the value of the US dollar as they have historically. The relationship between the dollar and Treasury yields is the weakest in three years as investors question the dollar’s haven status. Options positioning shows show that traders expect more losses for the dollar. The moves last weak were highly unusual and in an interview yesterday, Jenet Yellen stated that she believed the move in the USD last week was a sign of foreign asset selling. But there is a ton of narratives out in the markets about last weeks move.

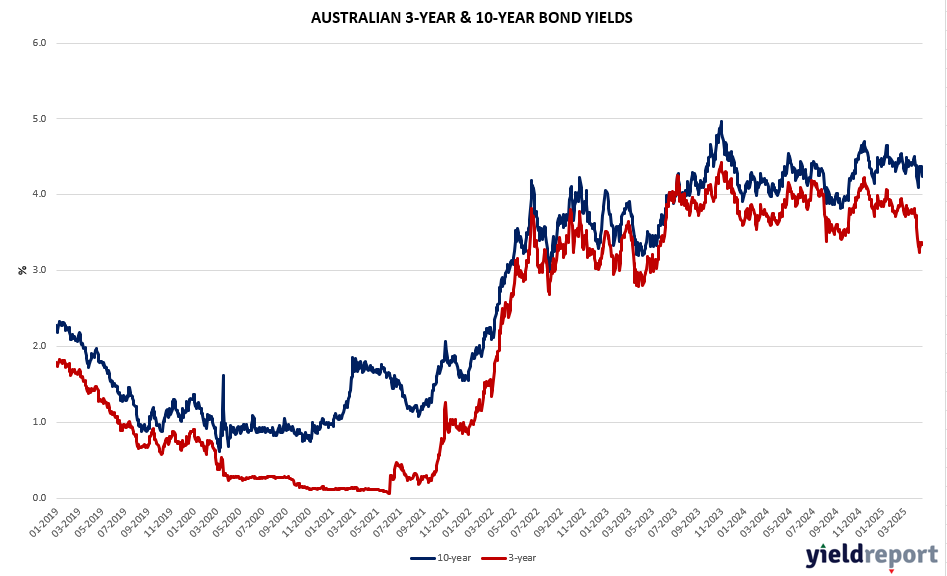

Exhibit 1. Australian 3Y/10Y Bond Yield

Exhibit 2. AU and US Bond Yields Spread

AU and US Bond Yields Spread

What the chart below highlights is just how much the Australian bond market is tracking and mirroring the US market. Chois your poison – I’d be Au Bonds any day. Sell off globally, as nerves settled.

Exhibit 3. Global Bond Yields