Summary:

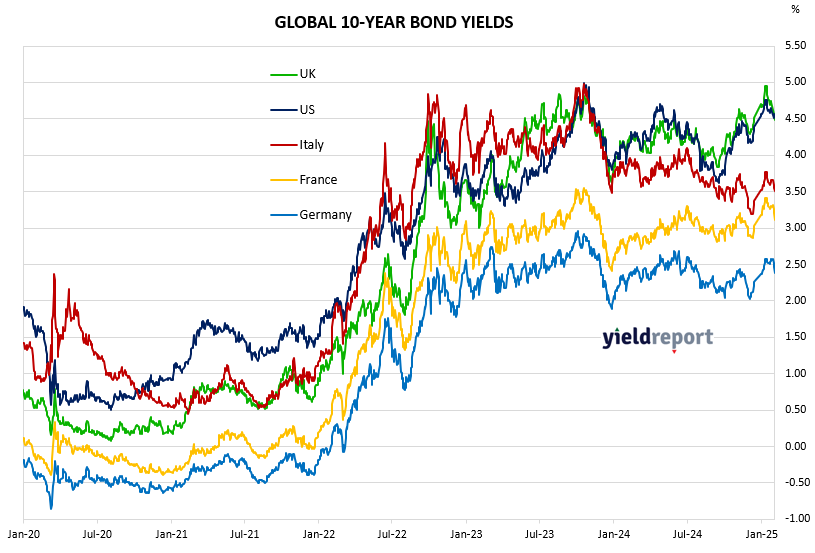

Another relatively choppy week for US bond markets. The yield on the 10-year rallied on Tuesday than sold off from Wednesday onwards, with the Wednesday decline coming after the Fed hinted it may slow the runoff of its balance sheet, while markets continued to assess the impact of more aggressive tariff threats from US President Trump. Minutes from the FOMC’s last meeting indicated that various members thought it will be appropriate to pause asset selling until the resolution of debt ceiling dynamics.

On Friday, the US Treasury bond yield note fell past 4.45%, the lowest in two weeks, as fresh data showed that the US services sector unexpectedly contracted unexpectedly in February as concerns about lower government spending drove clients to halt new orders, marking a sharp swing for the sector that had been resilient for two years.

The data favoured bets that the Fed may lis due to lower interest rates this year, with only 15% of the market positioned for no further no cuts by December. Meanwhile, the US Treasury department signalled it will not increase the share of longer-term securities within its financing plan in the near future, limiting the supply of debt securities in the longer end of the curve. This compounded support for 10-year notes after FOMC minutes.

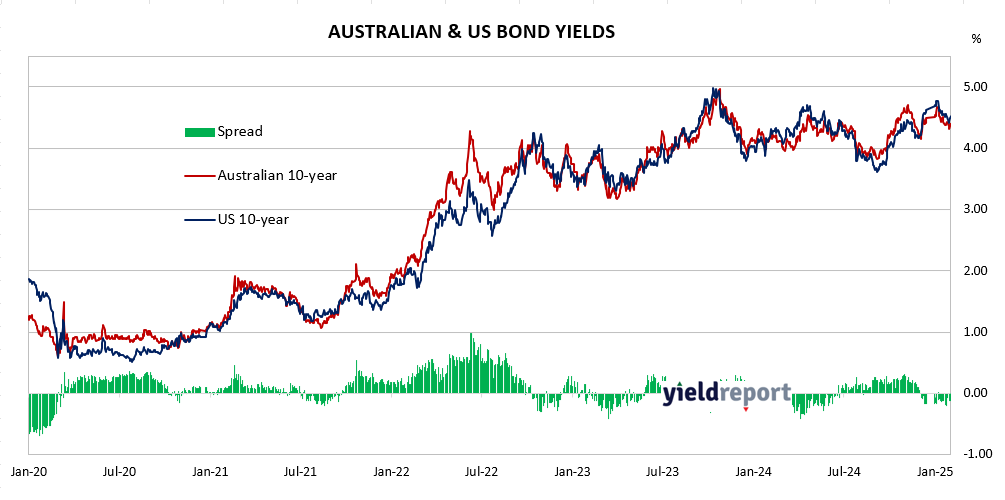

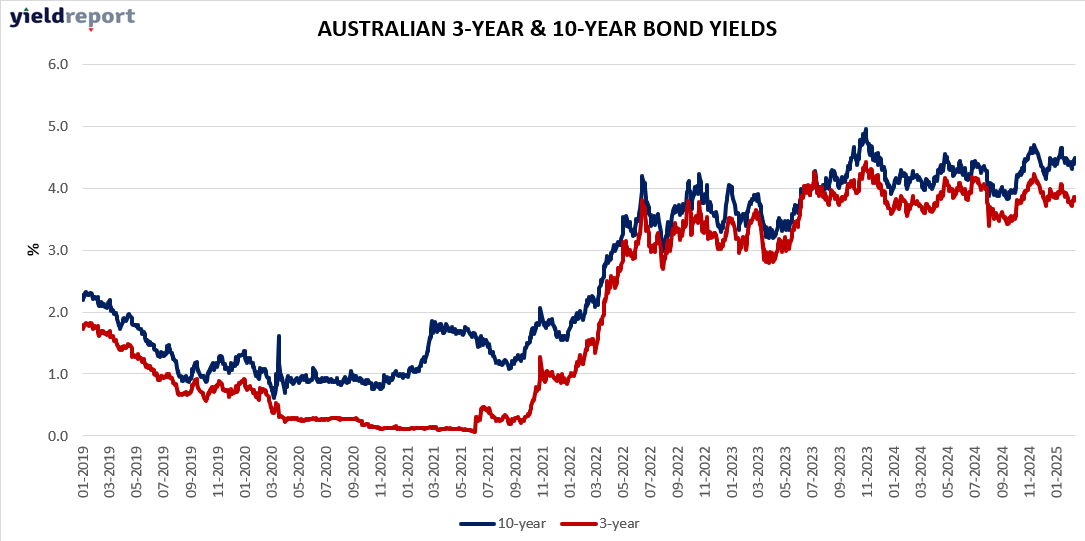

In Australia, as expected, the RBA cut its cash rate by 25 bps, the first reduction since November 2020, citing a significant decline in inflation, alongside weak economic growth and slower-than-expected recovery in private domestic demand. Despite the rate cut, policymakers cautioned about upside risks to inflation. Notwithstanding the cut, the 10-year Australian government bond yield rose 10 basis points to around 4.58% on Tuesday, reaching its highest level in over a month. Similarly, the more interest rate policy sensitive 2-year yield also rose.

While the cut was highly expected, the narrative from the RBA left many commentators in the market scratching their heads, with Michelle Bullock cautioning that further easing was not guaranteed given upside risks to inflation. If you are going to market a change in interest rate policy direction, should it not be done with conviction.?? And we go back to the opening sentence above – the 10-year is at its highest level in a month.

On Thursday, the release of labour market data showed employment climbed by 44,000 over the month in January, more than double market expectations of a 20,000 rise. Michelle Bullock stated that the jobs market is tighter than the RBA may like.

The interest rate market materially repriced interest rate expectations. The market is now implying only a 10% probability of another rate cut in April and suggests just 40bps of easing for 2025, equivalent to fewer than two rate cuts. A week is a long time in markets!