Summary: .

Over the course of the week, the yield on the US 10-year Treasury note fell by 17 basis points to 4.24%. And it was all largely driven by dovish comments from Fed officials. In an interview, Fed Governor Christopher Waller said he’d support rate cuts in the event aggressive tariff levels hurt the jobs market. Fed Bank of Cleveland President Beth Hammack told CNBC on Thursday the central bank could move on rates as early as June if it has clear evidence of the economy’s direction.

On the basis of these latter comments, the rally on Thursday was led by short to intermediate-maturity tenors, which are more sensitive than longer-maturity yields to Fed interest-rate changes. Yields on two-year notes declined as much as 8 basis points to just below 3.79%, remaining inside Wednesday’s range. The five-year yield declined nearly 10 basis points below 3.93%.

Swap contracts that aim to predict Fed actions priced in 15 basis points of easing — about 60% of a quarter-point rate cut — for the following meeting on June 17-18, up from around 13 basis points late Wednesday. The contracts priced in a combined 54 basis points of easing by September, four basis points more than previously, around 84 basis points by year-end, or at least three quarter-point cuts.

In US economic data Thursday, weekly jobless claims tallies suggested the labour market remains on solid ground. Speaking later Thursday, Fed Governor Christopher Waller said layoffs linked to tariffs wouldn’t be surprising and could warrant rate cuts, but are unlikely to be visible before mid-year.

US Treasuries – Safe haven? The traditional role of US Treasuries as the primary safe haven has been challenged during recent stress periods, marked by sharp yield spikes (10-year yield previously pushed above 4.5%) occurring even amidst equity downturns. Analysis points to forced deleveraging of highly leveraged basis trades (involving over $800B in net short futures) as the main technical driver behind these dislocations, rather than a fundamental abandonment by major foreign creditors.

The sense that the $29 trillion Treasuries market is the port of choice in a market storm has been a unique advantage for the world’s biggest economy, helping to keep a lid on US borrowing costs over the decades. But lately they’ve been trading a little more like a risky asset. Former Treasury Secretary Lawrence Summers went so far as to say they were behaving like the debt of an emerging-market country.

Dash for cash? Some investors may have ditched Treasuries along with other US assets to hide out in the ultimate haven: cash. Assets in US money-market funds — which are often viewed as like cash, with the extra upside that they earn money over time — have soared for some time as the Federal Reserve delayed rate cuts, and reached a record in the week through April 2.

We said several weeks ago – watch money market inflows.

Beyond technical pressures, the long-term sustainability of US fiscal policy is increasingly scrutinized, potentially eroding Treasury appeal. With significant projected deficits adding to the existing debt burden, the critical relationship between Treasury yields (‘r’) and economic growth (‘g’) comes into focus. A scenario where interest costs persistently outpace growth (r > g) signals a heavier debt servicing load, raising fundamental questions about the ultra-safe status of Treasuries for long-term holders compared to assets like gold.

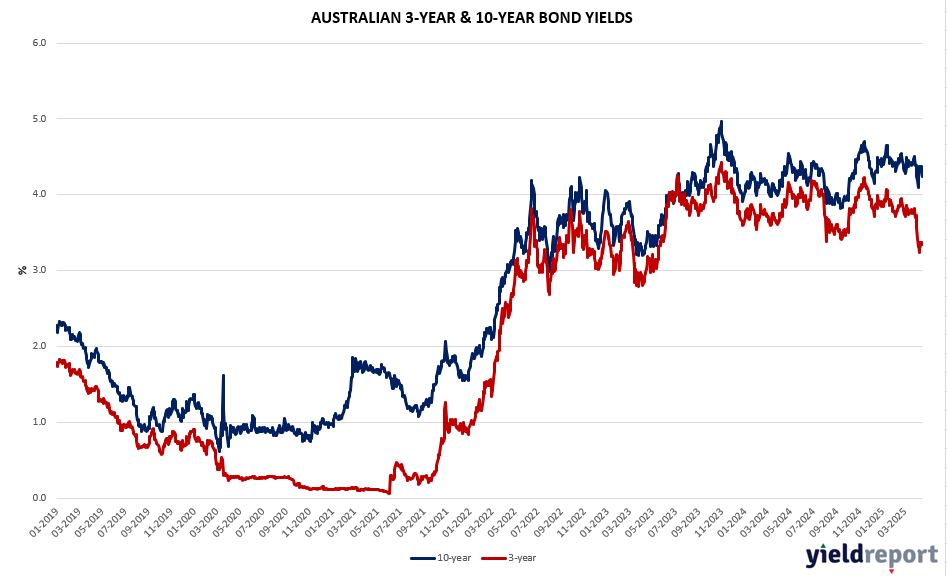

Exhibit 1. Australian 3Y/10Y Bond Yield

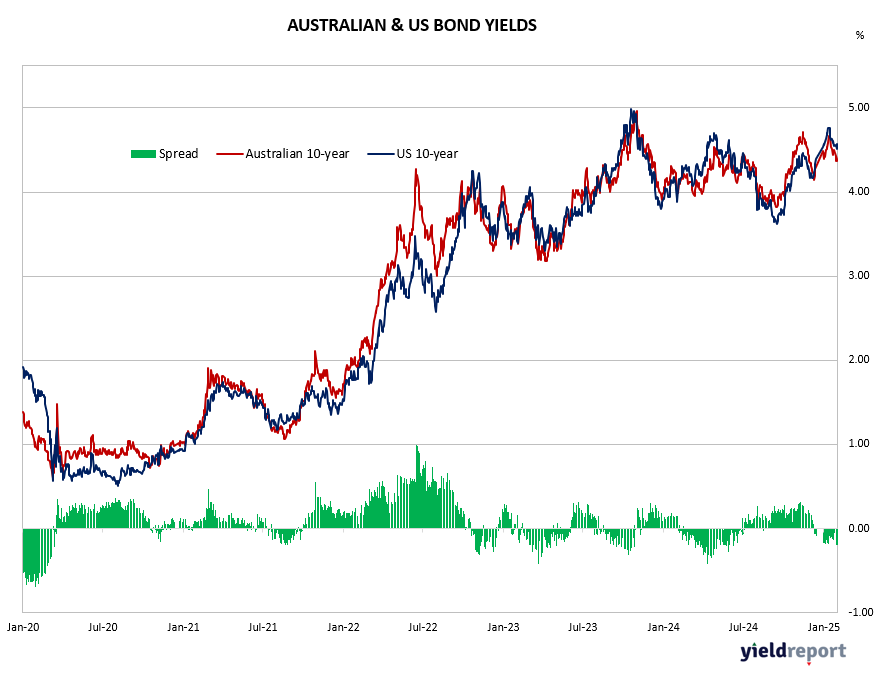

Exhibit 2. AU and US Bond Yields Spread

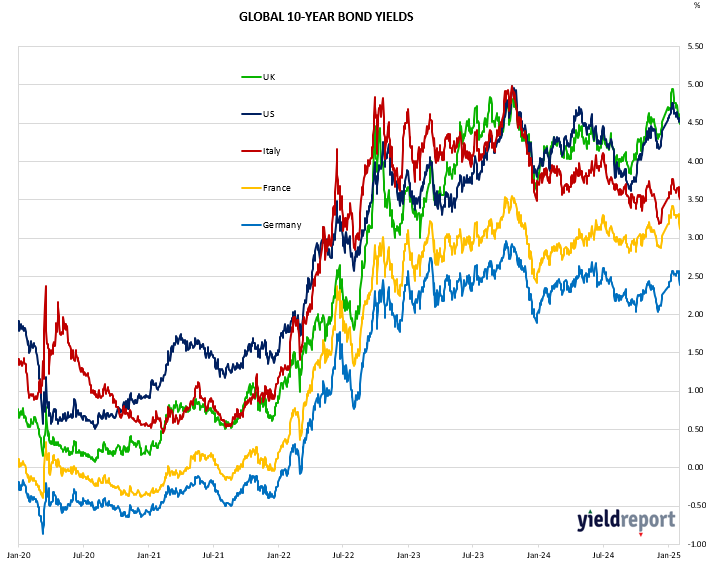

Exhibit 3. Global Bond Yields