Summary:

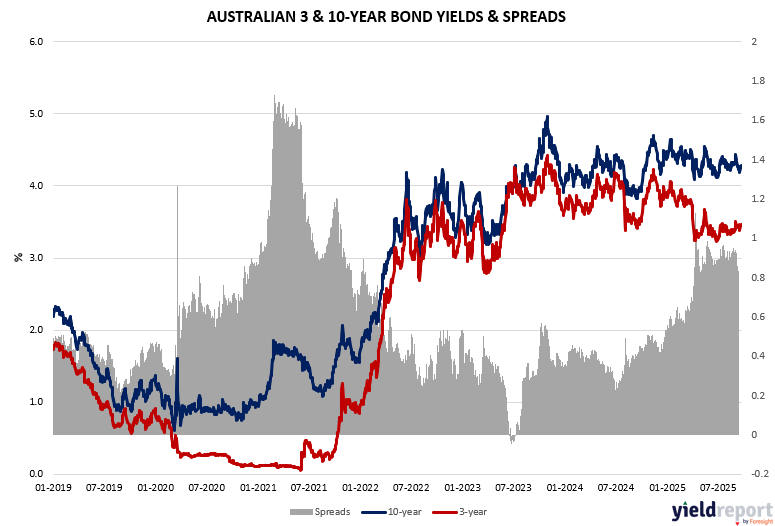

Australia’s cash rate held steady at 3.60%, while the 3-month BBSW rose 4bps to match, driven by stronger-than-expected CPI data and shifting expectations around RBA rate cuts. The yield curve steepened, with the 3-year bond yield up 16bps to 3.6%, 10-year up 14bps to 4.4%, and 30-year rising 7bps to 5.06%. Short-term rates showed volatility, but long-dated yields moved more sharply, reflecting investor concern over inflation and future RBA policy.

Bond spreads between 3- and 10-year maturities widened slightly, as the shorter end rose more aggressively than the longer end, signaling heightened sensitivity to inflation risks.

Figure 1: Aust. 3 yr minus 10 yr Bond Spread

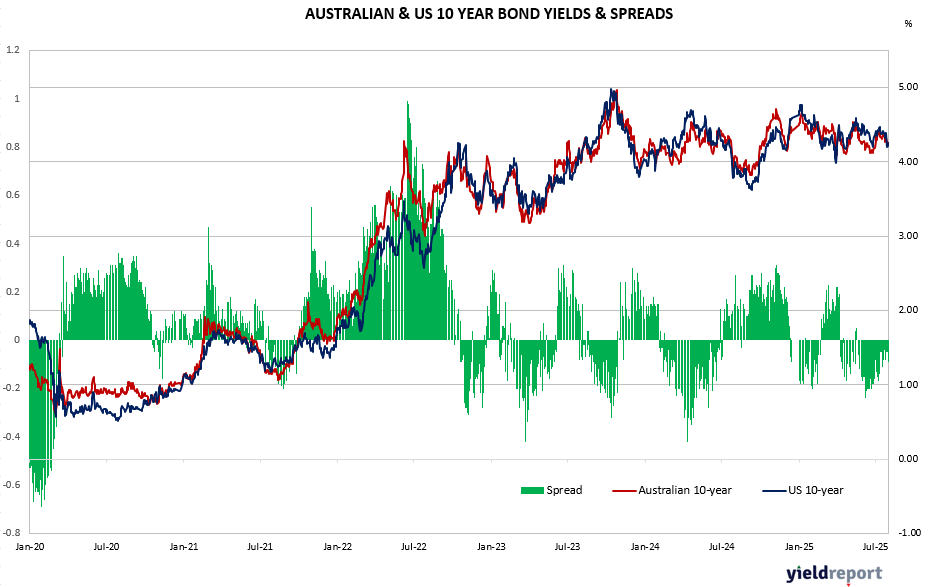

Figure 2: Australian & US Bond Yields

Figure 3: US 10-year minus 2-year Bond Spread