Summary: ACGB bond yields up in Australia; ACGB 10-year spread to US Treasury yield rises to 23bps; 10-year bond yields up in US, down in most major European markets; $3.5 billion of bonds, notes issued by AOFM.

Locally, long-term ACGB yields started with a noticeable increase which was followed by an even large reversal the next day. Yields then rose modestly for the remaining days of the week. At this stage, the 3-year ACGB yield had added 3bps to 3.45,%, the 10-year yield had gained 4bps to 3.98% while the 20-year yield finished 8bps higher at 4.41%. The spread between US and Australian 10-year Treasury bond yields increased from 20bps to 23bps.

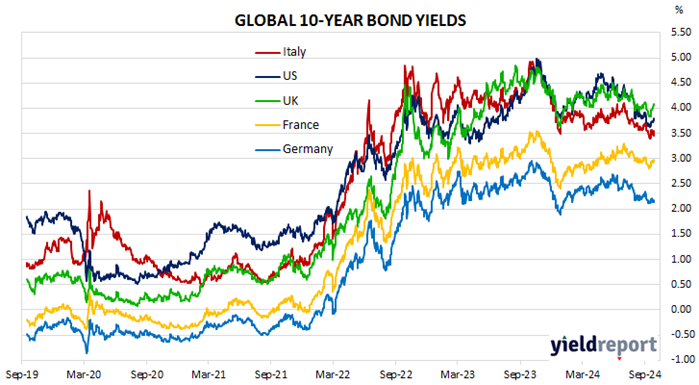

Over in the US, 10-year bond yields did not move much except for a moderate rise midweek and an equivalent fall at the end of the week.

S&P Global’s September flash reading of its US composite index were released at the start of the week. The composite index posted a decline from 54.6 in July to 54.4. The manufacturing index decreased from 47.9 to 47.0 while the services index declined from 55.7 to 55.4. “The early survey indicators for September point to an economy that continues to grow at a solid pace, albeit with a weakened manufacturing sector and intensifying political uncertainty acting as substantial headwinds.”

The Conference Board’s September reading of its Consumer Confidence Index was released on Tuesday. The index had its largest fall since 2021 but it still maintained a reading just above its long-term average.

The latest report on personal consumption expenditures came out at the end of the week. Core PCE price inflation increased by 0.1% in August and by 2.7% on an annual basis, up from 2.6% in July.

The New York Fed’s Nowcast model was also updated as usual at the end of the week. The September 2024 quarter forecast remained at 3.0% (annualised) while the December 2024 forecast was raised from 2.7% to 2.8%.

By this point, the US 2-year Treasury bond yield had lost 5bps to 3.56%, the 10-year yield had added 1bp to 3.75% while the 30-year yield finished 2bps higher at 4.10%.

In major euro-zone markets, 10-year bond yields moved in a vaguely similar manner to their US counterpart.

S&P Global released its September flash PMI figures for the euro-zone at the start of the week. The preliminary reading of the composite index was 48.9, down from August’s final reading of 51.0. “The eurozone is heading towards stagnation… Considering the rapid decline in new orders and the order backlog, it doesn’t take much imagination to foresee a further weakening of the economy.”

Germany’s ifo Institute released the September reading of its business climate index on Tuesday. The index declined again as German firms’ views of current conditions and the short-term outlook both deteriorated.

The latest reading of the euro-zone’s Economic Sentiment Indicator (ESI) came out at the end of the week. The index deteriorated slightly in September and is noticeably under its long-term average. This indicator has a solid correlation with euro-zone GDP.

By this point, the German 10-year bond yield had shed 8bps to 2.13% and the French 10-year OAT had lost 3bps to 2.93%. The Italian 10-year BTP yield decreased by 11bps to 3.46% over the week while the British 10-year gilt yield increased by 8bps to 4.06%.

The AOFM held two vanilla bond tenders this week. $1.0 billion of May 2034s and $500 million of May 2028s were priced at nominal yields of 3.91% and 3.50% respectively. There were also two Treasury note tenders which raised $2.0 billion on a short-term basis.

The gross value of all bonds issued by the AOFM in the 2024/2025 financial year (not taking into account short-term Treasury note tenders) is $29.20 billion. There are currently $866.55 billion of Treasury bonds and $41.485 billion of Treasury index-linked bonds on issue. The next series to mature does so on 21 November 2024 when $41.30 billion worth of bonds are due. There are also $25.00 billion of short-term Treasury notes outstanding.