Summary:

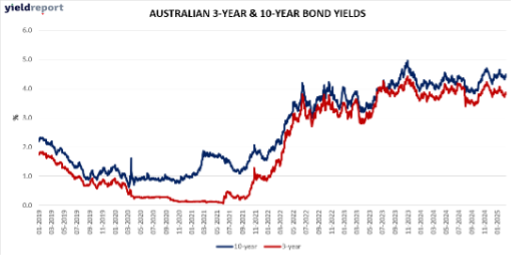

As noted previously, directionally, Australian government bond yields have since the beginning of the year being set by the direction of the US bond market. And that means the 10-year government bond has had its best month since July 2024 as yields fell all week. The 10-year declined 17 basis points over the week. It is off almost 30 basis points since its January 13 recent high. The 2-year, 12 basis points, pricing in 3.77% versus the current cash rate of 4.1%.

So, notwithstanding the government bond yield volatility – which has been marked – bonds have been exhibiting negative correlation to equities, and has generally been doing so for six months. This is significant – the inverse correlation not only broke down from early 2003 but went wildly positive.

Focus on Australia, a report released on Thursday showed that business investment unexpectedly declined in the fourth quarter, indicating a slight drag on economic growth and adding to case for more policy easing. Meanwhile, data on Wednesday showed headline inflation held at an annual 2.5% in January, while core inflation ticked up to 2.8%.

While this report does not provide definitive signal for further rate cuts, it offers reassurance that inflation is trending in the right direction and supports the Reserve Bank of Australia’s recent rate cut. However, RBA Deputy Governor Andrew Hauser said on Thursday that the central bank would need to see further progress in inflation before considering additional rate cuts.

But as noted, the direction is really being set by the US markets. Forget actual data, it’s the slew of negative consumer sentiment / expectations surveys over the last three weeks that is really setting the tone – declining yields (rising bond prices), a very nervous equities market.

Take Friday as an example. The yield on the 10-year US Treasury note was at the 4.25% mark on Friday, plunging over 15bps in the week to its lowest in over two months as markets assessed the latest economic data against concerns that tariffs and aggressive government spending cuts will hurt growth. Personal spending in the US unexpectedly slipped in January while income soared. Additionally, headline and core PCE price indices edged higher as expected, maintaining market bets that the Federal Reserve is due to cut rates twice this year.

Interestingly, corporate bonds have become the new safe haven, and over and above government bonds. We discuss this in some detail in this week’s thematic spotlight. 2025 is looking like the year of bonds.

Exhibit 1. Australian 3Y/10Y Bond Yield

Exhibit 2. AU and US Bond Yields Spread

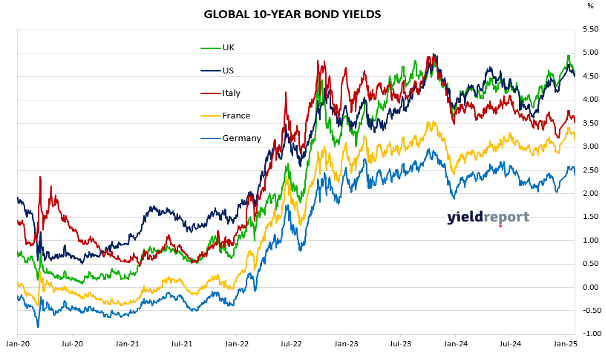

Exhibit 3. Global Bond Yields