Summary: Treasury yields trended lower following the release of February personal consumption expenditures data. Core inflation accelerated to 0.4% m/m monthly, coming in above expectations and marking a second consecutive month of inflation running at a monthly pace faster than what would be in line with the Fed’s 2% annual target. The stronger inflation data was offset by weaker-than-expected real spending data rising 0.1% m/m after falling 0.5% in January.

Treasuries are on track to post the first month of negative returns in 2025, falling nearly 1% month to date as of yesterday’s close. Tariff headlines weighed on financial markets throughout March, adding to investors’ inflation expectations and putting upward pressure on yields. More tariff announcements are on tap next week on April 2, and many market commentators expect those to follow a similar pattern as other recent announcements, where the president declares sweeping measures, then the impacted countries move to negotiate the terms.

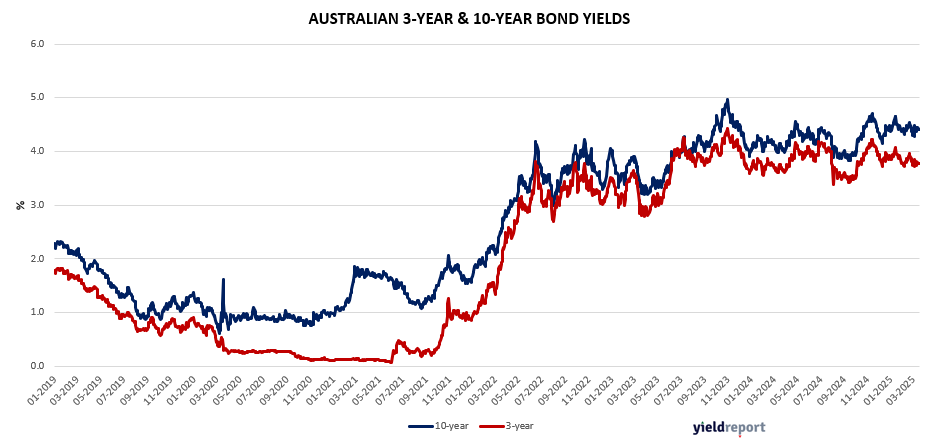

Exhibit 1. Australian 3Y/10Y Bond Yield

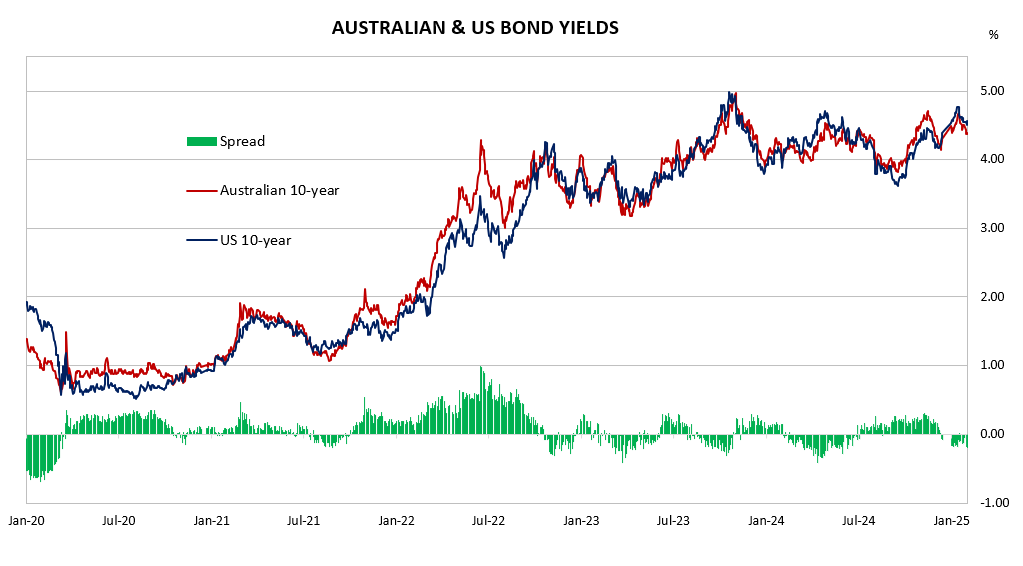

Exhibit 2. AU and US Bond Yields Spread

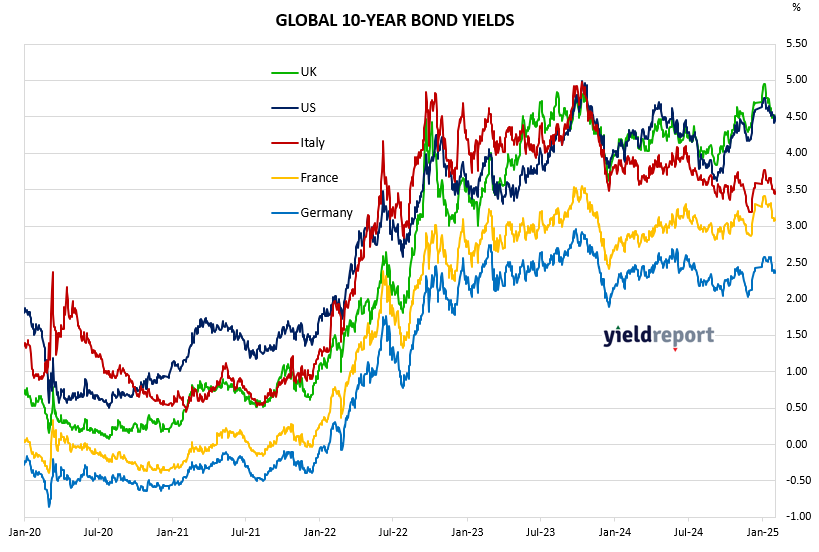

Exhibit 3. Global Bond Yields

The Treasury yield curve reached its steepest level since mid January on Thursday, with the difference between the 2- and 10-year Treasury yields widening to 37 bps yesterday before easing to 34 bps today. The prospect of Fed cuts later this year have curbed a rise in the policy-sensitive 2-year yield, with fed funds futures pricing in two rate cuts and a 50% chance of a third.

On the long end of the curve, the latest tariff headlines have led investors to demand more compensation for inflation risks, pushing the 10- and 30-year Treasury yields to their highest levels since late February, suggesting markets are doubting Fed Chair Powell’s recent comments that he expects tariff-induced price pressures to be “transitory.” Atlanta Fed President Raphael Bostic pushed back on that idea earlier this week, saying that he does not expect inflation to reach the Fed’s 2% annual target until 2027, in line with the median FOMC member as of March’s forecasts. Back in September, the median FOMC participant expected inflation to reach the target level in mid to late 2026.

Australia’s 10-year government bond yield remained elevated at a five-week high of 4.51%, despite recent soft inflation data. Australia’s headline inflation eased to 2.4% in February from 2.5% in the previous month, while core inflation also fell to 2.7% from 2.9%. The data comes less than a week before the Reserve Bank of Australia’s next policy decision on April 1, where the central bank is expected to keep rates unchanged.

Meanwhile, markets currently see a 64% chance of a rate cut in May. However, the central bank has warned earlier that further monetary easing is not guaranteed, after its first rate cut in over four years last month. In other news, the Australian government on Tuesday announced two additional personal income tax cuts set for 2026 and 2027, totalling A$17.1 billion over the forward estimates.