Summary: ACGB yields down in Australia; ACGB 10-year spread to US Treasury yield rises to 18bps; 10-year bond yields down in US, major European markets; $2.3 billion of bonds issued by AOFM.

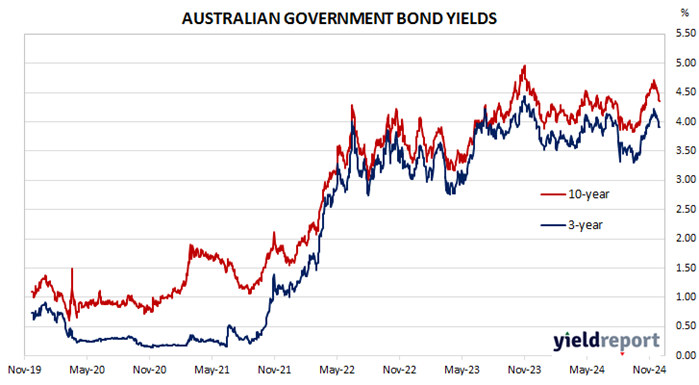

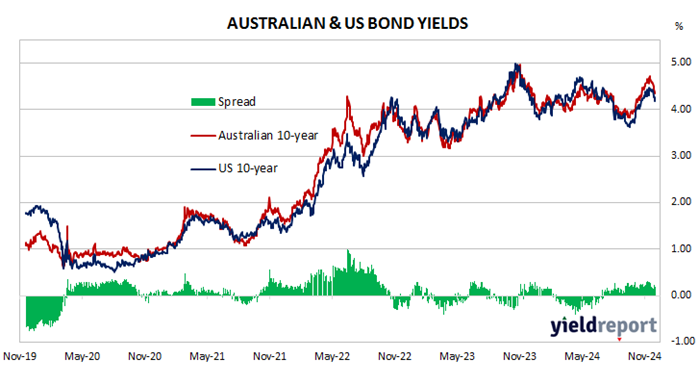

Locally, long-term ACGB yields declined though the entire week. By the end of it, the 3-year ACGB yield had lost 17bps to 3.91%, the 10-year yield had shed 21bps to 4.35% while the 20-year yield finished 17bps lower at 4.68%. The spread between US and Australian 10-year Treasury bond yields rose from 15bps to 18bps.

Over in the US, 10-year bond yield movements alternated between “up” days and “down” days, with the “down” noticeably larger in magnitude.

Minutes of the FOMC November meeting were released on Tuesday. They did nothing to suggest the FOMC had materially changed its view with respect to lowering its federal funds target range over the next twelve months.

The Conference Board’s November reading of its Consumer Confidence Index was also released. The index increased again, maintaining a level which is well above average.

The latest report on personal consumption expenditures came out next week. Core PCE price inflation increased by 0.3% in October and by 2.8% on an annual basis.

The New York Fed’s Nowcast model was updated as usual at the end of the week. The December 2024 quarter forecast was trimmed from 1.9% (annualised) to 1.8%.

By this stage, the US 2-year Treasury bond yield had lost 22bps to 4.15%, the 10-year yield had shed 24bps to 4.17% while the 30-year yield finished 22bps lower at 4.36%.

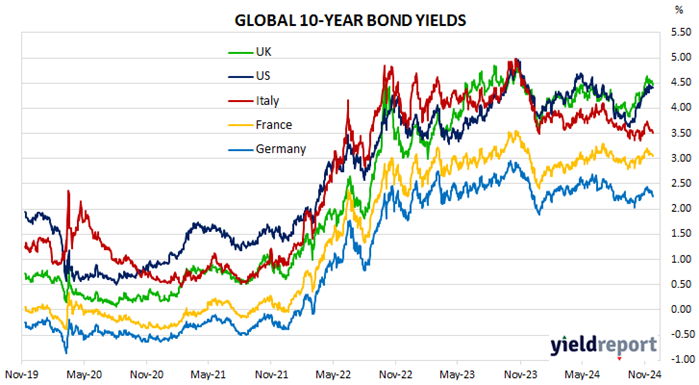

In major euro-zone markets, 10-year bond yields mostly fell through the entirety of the week.The latest reading of the euro-zone’s Economic Sentiment Indicator (ESI) was posted on Thursday. The index increased a little in November but remains noticeably under its long-term average. This indicator has a solid correlation with euro-zone GDP and it implied a year-to-November growth rate of 0.6%.

The “flash” November consumer price index (CPI) report was released at the end of the week. The euro-zone CPI decreased by 0.3% over the month but increased by 2.3% over the year, up from 2.0% in October. Annual core CPI remained steady at 2.7%.

By this point, the German and French 10-year bond yields had both shed 15bps to 2.09% and 2.90% respectively. The Italian 10-year BTP yield fell 22bps to 3.28% over the week while the British 10-year gilt yield finished 13bps lower at 4.33%.

The AOFM made a syndicated issue of index-linked bonds (ILBs) in addition to two vanilla bond tenders this week. $800 million of August 2040 ILBs were issued at a real yield of 2.19% while $800 million of December 2034s and $700 million of June 2031s were priced at nominal yields of 4.43% and 4.16% respectively. There were also two Treasury note tenders which raised $2.0 billion on a short-term basis.

The gross value of all bonds issued by the AOFM in the 2024/2025 financial year (not taking into account short-term Treasury note tenders) is $43.60 billion. There are currently $839.45 billion of Treasury bonds and $42.685 billion of Treasury index-linked bonds on issue. The next series to mature does so on 21 April 2025 when $41.50 billion worth of bonds are due. There are also $30.00 billion of short-term Treasury notes outstanding.