Summary: ACGB bond yields down in Australia; ACGB 10-year spread to US Treasury yield falls to -8bps; 10-year bond yields down in US, up in major European markets; $2.95 billion of bonds, notes issued by AOFM.

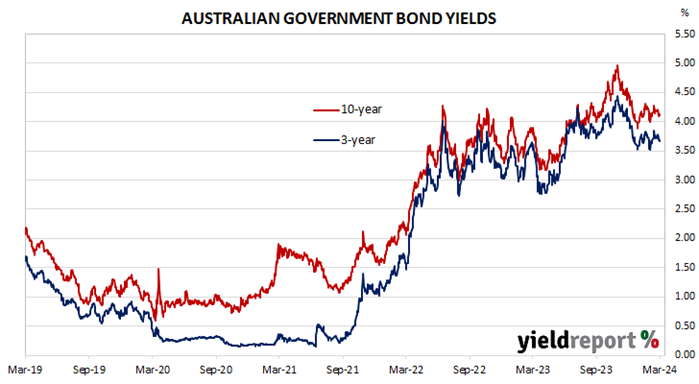

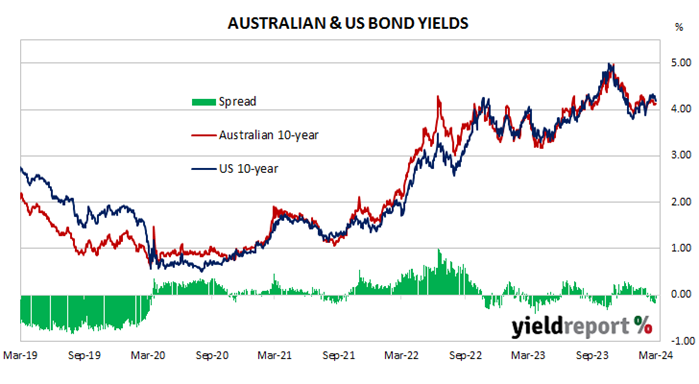

Locally, long-term ACGB yields started the week with a large fall which was followed by a couple days of moderate rises. Yields then declined on Thursday and steadied at the end of the week. By this point, 3-year ACGB and 10-year yields had both lost 10bps to 3.68% and 4.11% respectively while the 20-year yield finished 7bps lower at 4.44%. The spread between US and Australian 10-year Treasury bond yields fell from -4bps to -8bps.

Over in the US, 10-year bond yields started with a couple of days of modest rises. Yield then fell back midweek and again at the end of the week.

The latest reading of The Conference Board’s Consumer Confidence Index came out on Tuesday. Confidence deteriorated in February after three months of improvement again, a third consecutive month of gains for the index.

The latest report on personal consumption expenditures was released a couple of days later. Core PCE price inflation increased by 0.4% in January and by 2.8% on an annual basis, slightly slower than December’s 2.9%.

The ISM’s February reading of its PMI came out at the end of the week. At 47.8 it was below expectations and in contractionary territory.

The US Fed’s Nowcast model was also updated. The March 2024 quarter forecast was lowered from 2.8% to 2.3%.

By this stage, the US 2-year Treasury bond yield had shed 14bps to 4.53%, the 10-year yield had lost 6bps to 4.19% while the 30-year yield finished 4bps lower at 4.33%.

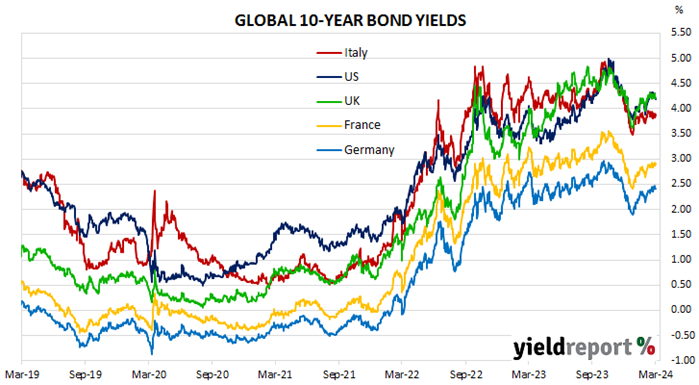

In major euro-zone markets, 10-year bond yields moved in a broadly similar manner to their US counterpart except they increased slightly at the end of the week instead of falling noticeably.

The latest euro-zone’s Economic Sentiment Indicator (ESI) came out midweek. The index declined slightly in February and remains under its long-term average. This indicator has a solid correlation with euro-zone GDP and it implied a year-to-February growth rate of 0.3%, down from 0.4% in January.

The “flash” February consumer price index (CPI) report was released at the end of the week. It produced an annual inflation rate of 2.6% for the euro-zone, slightly above expectations. Annual core CPI slowed from 3.3% to 3.1%.

By this point, the German 10-year bund yield had added5bps to 2.42% while the French 10-year OAT yield had gained 7bps to 2.90%. The Italian 10-year BTP yield also increased by 7bps to 3.88% over the week while the British 10-year gilt yield finished 1bp higher at 4.21%.

The AOFM held an index-linked bond tend in addition to the usual vanilla bond tender this week; $150 million of February 2050 ILBs were priced at a real yield of 1.91% while $800 million of May 2034s were priced at a nominal yield of 4.13%. There were also two Treasury note tenders which raised $2.0 billion on a short-term basis.

The gross value of all bonds issued by the AOFM in the 2023/2024 financial year (not taking into account buy-backs or short-term Treasury note tenders) is $30.6 billion. There are currently $853.05 billion of Treasury bonds and $40.986 billion of Treasury index-linked bonds on issue. The next series to mature does so on 21 April 2024 when $35.90 billion worth of bonds are due. There are also $28.00 billion of short-term Treasury notes outstanding.