Summary:

The Reserve Bank of Australia (RBA) held the cash rate steady at 3.6% during its October 2025 meeting. Governor Michele Bullock emphasized a cautious but optimistic outlook, citing signs of recovery in consumption and labour markets. Inflation remains within the target band, though pressures from services and housing persist. The RBA refrained from forward guidance, opting for a data-dependent approach. Markets and government commentary have shifted expectations, with fewer anticipating further rate cuts. The next policy decision will be informed by updated CPI data and labour market indicators in November

Market participants have recalibrated expectations, with fewer anticipating further rate cuts. The RBA acknowledged stronger-than-expected inflation data as a key driver of this shift. While the RBA did not directly reference government commentary, economists and markets have adjusted expectations. Earlier forecasts of further rate cuts have been tempered by stronger-than-expected inflation data.

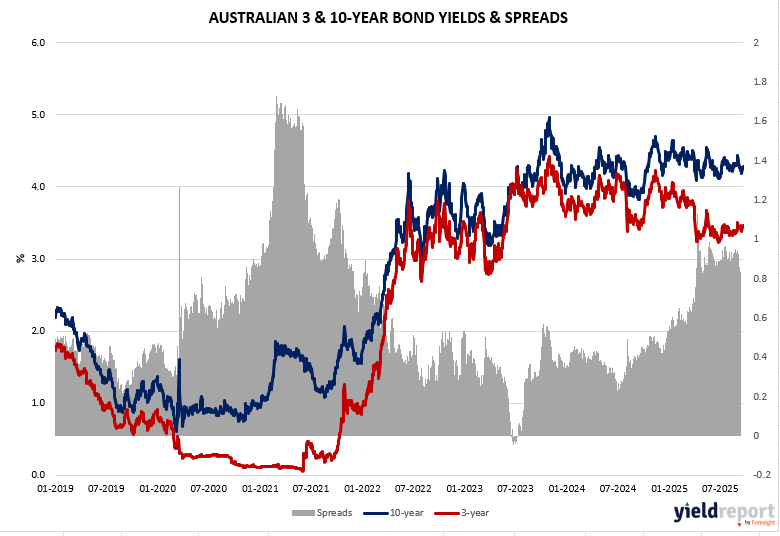

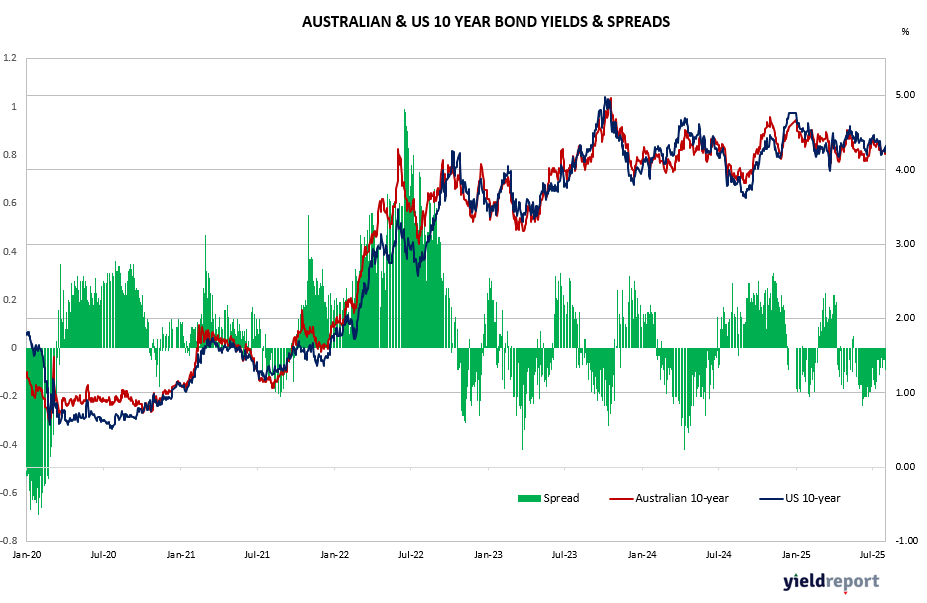

The Australian Bond spreads (3 & 10 years) continue to indicate positive sloping yield curve with significant steepening in the curve occurring from July 2023 (phase 1) and then accelerating from July 2024. The current spread continues to be at cyclical highs although lower than record highs observed in2021. From an investment perspective, steepening yield curves and a rebounding lending environment are likely to boost domestic economic environment and bank profitability. In a similar vein, the spread between the US 2 year bonds and US 10 Year bond has also been steepening since July 2023.

Figure 1: Aust. 3 yr minus 10 yr Bond Spread

Figure 2: Australian & US Bond Yields

Figure 3: US 10-year minus 2-year Bond Spread