Summary:

Australian Fixed Income

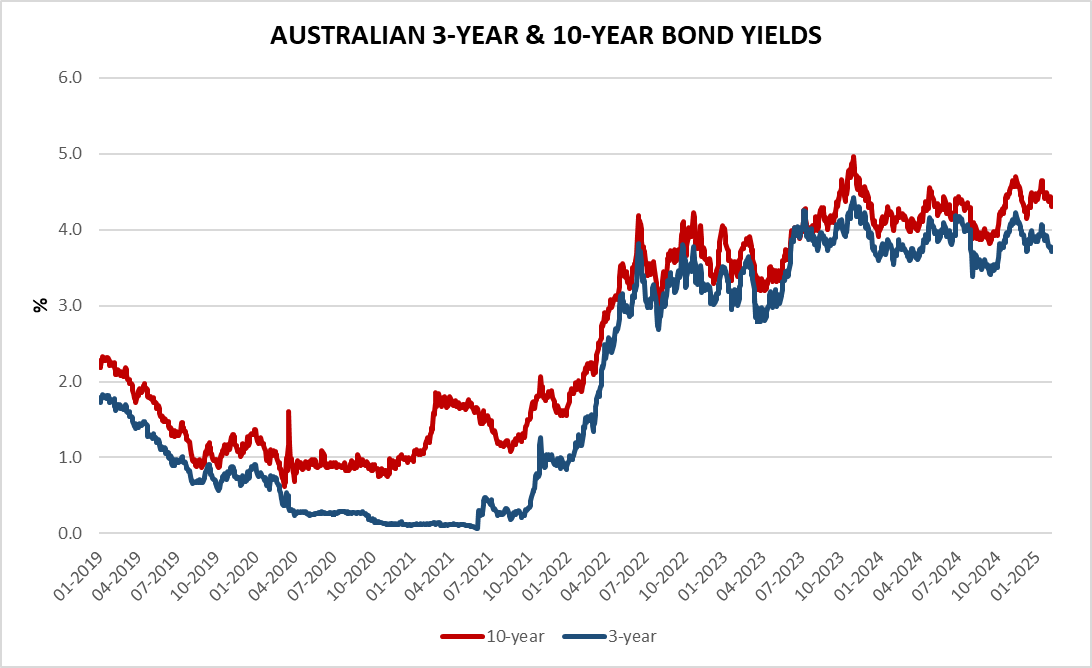

Australia’s 10-year government bond yield remained effectively unchanged over the course of the week, declining 1 basis point to 4.35% by Friday. During the week the bond instrument touched a seven-week low on Wednesday amid dovish expectations for the Reserve Bank of Australia’s upcoming policy decision. Domestic investors remained confident the RBA will lower its 4.35% cash rate at its meeting later this month, with market pricing in a 95% chance of a 25 basis point rate cut from the RBA in February to 4.1%. If this does not happen the market is pricing in a rate cut in April as a certainty.

This follows recent data showing underlying inflation has moderated faster than the RBA forecasted, which also led to some major Australian banks to shift their call for the first cut to February from May. However, a first cut is maybe viewed as more of a policy step towards a less restrictive stance given the softer economic activity. The RBA is unlikely to rush to neutral stance, preferring to verify the path of inflation in the quarterly reports and align further cuts with their quarterly forecast schedule.

Australian Government Bonds.csv

| Bond | Yield | Day | Month | Year |

|---|---|---|---|---|

| 10-year | 4.35% | +0.034% | -0.159% | +0.244% |

| 3-year | 3.76% | +0.047% | -0.167% | +0.095% |

| 2-year | 3.79% | +0.031% | -0.115% | +0.022% |

| 1-year | 3.93% | +0.023% | -0.127% | -0.141% |

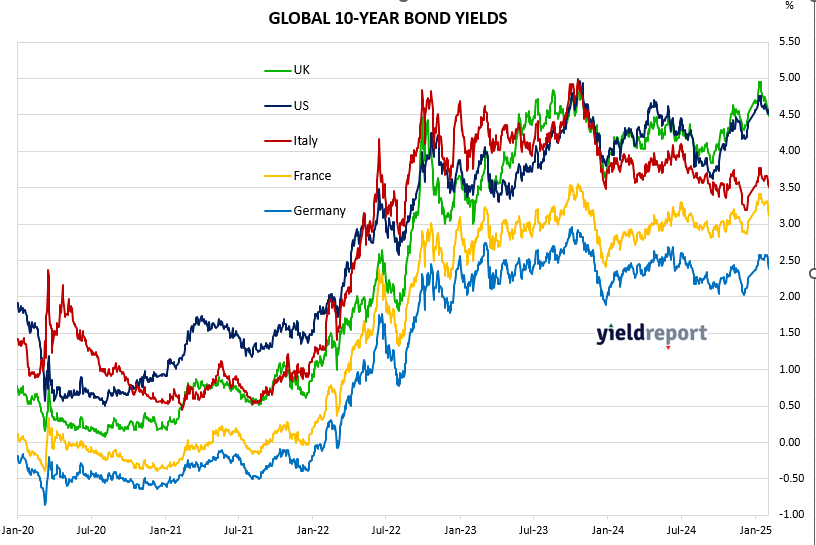

The US employment report for January released on Friday was hotter than expected: payrolls up by 143,000; unemployment rate ticked down to 4%; average hourly earnings up 0.5%; participation rate also up. Yields consequently increased.

Later on Friday the University of Michigan Sentiment Index data showed that consumers expect inflation to be a full percentage point higher in 12-months from 3.3% to 4.3% on account of tariffs. The heightened near-term inflation expectations drove down consumer sentiment to a 7-month low in early February.

While not the largest move in yields, the data releases are very significant Fed policy wise. Unemployment rate coming down and inflation expectations going up is effectively Fed kryptonite. The data reinforces the prevailing view of ‘higher for longer’ and the that Fed can be quite patient, not needing to move anytime soon and more so given the uncertainties regarding tariffs. On the topic of the latter and which will likely impact Fed timing, it may take some time on what the full details are and, consequently, have true clarity between the economic data and ultimately what the interest rate term policies will be.

In short, yields may well be range-bound for the foreseeable future and at levels the majority of fund managers view as very attractive rates notwithstanding the very tight spreads (see chart below). It is the latter that may represent the key risk (i.e. a widening) for sectors/companies with material sales and supply chain exposures. It highlights the need for a selective approach rather than a broader market beta play, and the more so the lower in the ratings scale the exposure is.

Meanwhile, traders maintained bets for a quarter-point rate reduction in September. All told, the swaps market suggests around 35 basis points of rate cuts for this year, less than 50 percent odds of a second quarter-point reduction. So, the market’s view is that the developments definitively removes market expectations for the window to cut in March.

The chart below displays the latest 10-2 year spread. The spread remains in the positive, with the last time the spread was negative was on September 5, 2024. In other words, the market is no longer signalling a possible economic downturn.

Figure 1: US 2 year and 10 year bond spread

Figure 2: US AAA and High Yield Option-Adjusted Spread