Summary: 10-year bond yields moderately higher in Australia, slightly lower in US, Germany; ACGB 10-year spread to US Treasury yield widens from +9bps to +18bps; RBA buys $4 billion of various ACGBs & semis, purchases now total $269.5 billion; AOFM issues $3 billion worth of bonds, notes.

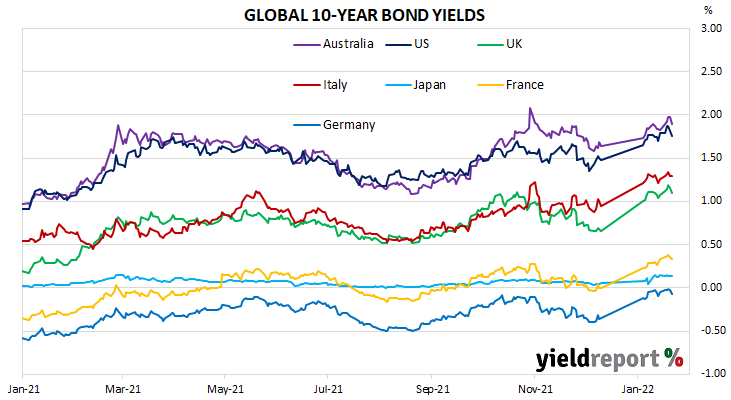

Sovereign 10-year bond yields finished the week moderately higher in Australia but slightly lower in the US and Germany. Yields in other major European markets increased a touch.

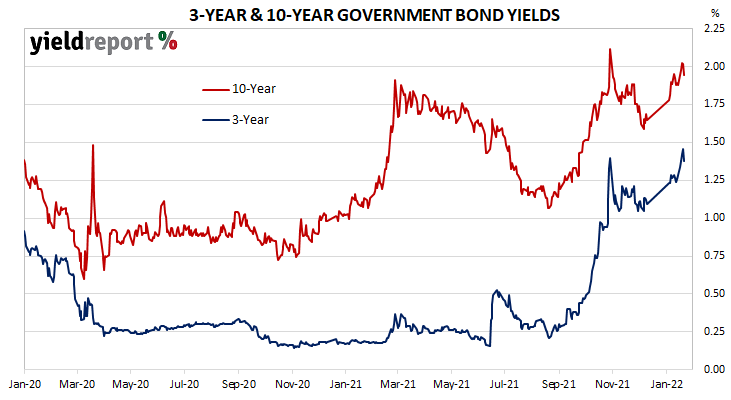

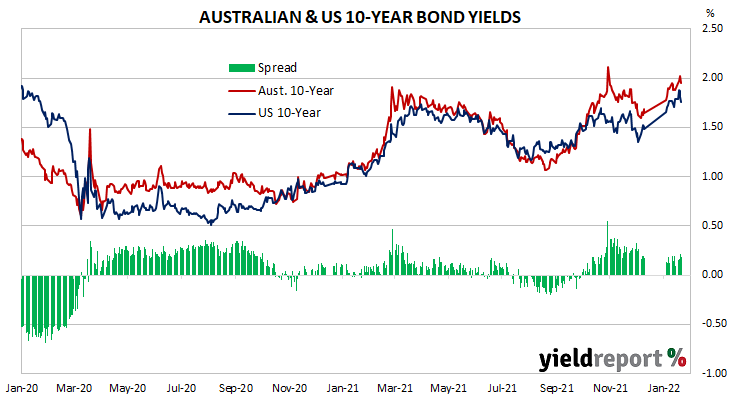

Locally, long-term ACGB yields increased noticeably over the first three days of the week before partially retracing those rises over much of the remainder. By this point, the 3-year ACGB yield had gained 9bps to 1.38%, the 10-year yield had added 6bps to 1.94% while the 20-year yield finished 4bps higher at 2.44%. The spread between US and Australia 10-year Treasury bond yields widened from +9bps to +18bps. The RBA purchased another $4.0 billion worth of various ACGBs and semis with maturities from November 2024 to April 2033 over the week. The RBA’s programme has now purchased $269.5 billion of bonds to date with a review set to take place next month.

Over in the US, long-term bond yields jumped at the start of the shortened week and then fell back over the remainder as equity-market jitters produced a move to lower-risk assets.

There were not many US economic reports during the week and the only really notable one, apart from the weekly jobless report, did not come out until Friday.

The weekly initial jobless claims report was released on Thursday. Total claims amounted to 0.286 million for the week to Saturday 15 January, 55,000 more claims than in the previous week after revisions. As at 8 January, continuing claims (seasonally adjusted) totalled 1.635 million, an 86,000 rise from the previous week’s total after revisions.

The next day, December’s increase in The Conference Board’s leading index met market expectations. The Conference Board expects US GDP to grow by 3.5% over calendar 2022, with about 0.5 percentage points of that in the March quarter.

By this point, the US 2-year Treasury bond yield had gained 5bps to 1.01% while the 10-year yield had lost 3bps to 1.76% and the 30-year yield had shed 4bps to 2.08%.

In major euro-zone markets, 10-year bond yields increased modestly over the first few days of the week before sliding back over the remainder.

On Tuesday night (AEST), Germany’s ZEW January survey indicated its Economic Sentiment index had increased “significantly” from December’s reading of 29.9 to 51.7, much higher than the 32.0 which had been generally expected. However, Its current conditions index declined from -7.4 to -10.2.

At the end of the week, January’s consumer sentiment survey indicated euro-zone consumers had become a little more cautious, again.

By the end of the week, the German 10-year bund yield had shed 2bps to -0.07% while the French 10-year OAT yield was unchanged at 0.33%. The Italian 10-year BTP yield increased by 3bps to 1.29% over the week while the British 10-year gilt yield finished 2bps higher at 1.10%.

The AOFM held two bond tenders during the week. $500 million of June 2035s and $1.5 billion of April 2025s were priced at yields of 2.15% and 1.33% respectively. Their respective coverage ratios were 2.2 and 2.9.

There was also one Treasury note tender which raised $1 billion on a short-term basis.

The gross value of all bonds issued by the AOFM in the 2021/2022 financial year-to-date (not taking into account buy-backs or short-term Treasury note tenders) is $52.3 billion. There are currently $782.813 billion of Treasury bonds and $41.107 billion of Treasury index-linked bonds on issue. The next bond series to mature does so on 15 July when $24.763 billion worth of bonds are due. There are also $33.00 billion of short-term Treasury notes currently outstanding after $4 billion matured on Friday.

| MATURITY | COUPON (%) | ISSUE SIZE ($M) | CLOSING YIELD | Δ WEEK | Δ MONTH | WEEK HIGH | WEEK LOW |

|---|---|---|---|---|---|---|---|

| 21-Nov-22 | 2.25 | 26,500 | 0.34 | 0.03 | 0.11 | 0.38 | 0.34 |

| 21-Apr-23 | 5.50 | 34,200 | 0.57 | 0.06 | 0.22 | 0.63 | 0.55 |

| 21-Apr-24 | 2.75 | 34,400 | 0.85 | 0.13 | 0.20 | 0.90 | 0.78 |

| 21-Nov-24 | 0.25 | 37,600 | 1.11 | 0.10 | 0.19 | 1.19 | 1.07 |

| 21-Apr-25 | 3.25 | 35,600 | 1.32 | 0.10 | 0.22 | 1.39 | 1.27 |

| 21-Nov-25 | 0.25 | 22,000 | 1.45 | 0.09 | 0.21 | 1.52 | 1.41 |

| 21-Apr-26 | 4.25 | 37,100 | 1.49 | 0.09 | 0.22 | 1.56 | 1.45 |

| 21-Sep-26 | 0.50 | 31,800 | 1.56 | 0.09 | 0.23 | 1.64 | 1.53 |

| 21-Apr-27 | 4.75 | 33,900 | 1.59 | 0.09 | 0.22 | 1.67 | 1.56 |

| 21-Nov-27 | 2.75 | 29,700 | 1.66 | 0.09 | 0.22 | 1.73 | 1.63 |

| 21-May-28 | 2.25 | 29,700 | 1.70 | 0.07 | 0.23 | 1.77 | 1.68 |

| 21-Nov-28 | 2.75 | 32,100 | 1.74 | 0.06 | 0.24 | 1.81 | 1.73 |

| 21-Apr-29 | 3.25 | 33,000 | 1.76 | 0.07 | 0.24 | 1.83 | 1.75 |

| 21-Nov-29 | 2.75 | 32,900 | 1.80 | 0.07 | 0.25 | 1.88 | 1.80 |

| 21-May-30 | 2.50 | 36,600 | 1.83 | 0.06 | 0.25 | 1.91 | 1.83 |

| 21-Dec-30 | 1.00 | 24,700 | 1.88 | 0.06 | 0.26 | 1.95 | 1.88 |

| 21-Jun-31 | 1.50 | 36,300 | 1.89 | 0.07 | 0.26 | 1.96 | 1.88 |

| 21-Nov-31 | 1.00 | 21,000 | 1.90 | 0.07 | 0.27 | 1.97 | 1.90 |

| 21-May-32 | 1.25 | 30,200 | 1.92 | 0.07 | 0.26 | 1.99 | 1.92 |

| 21-Apr-33 | 4.50 | 18,800 | 1.93 | 0.06 | 0.26 | 2.00 | 1.93 |

| 21-Jun-35 | 2.75 | 9,050 | 2.08 | 0.06 | 0.23 | 2.15 | 2.08 |

| 21-Apr-37 | 3.75 | 12,000 | 2.19 | 0.05 | 0.20 | 2.26 | 2.19 |

| 21-Jun-39 | 3.25 | 9,900 | 2.32 | 0.04 | 0.18 | 2.39 | 2.32 |

| 21-May-41 | 2.75 | 13,000 | 2.42 | 0.04 | 0.18 | 2.49 | 2.42 |

| 21-Mar-47 | 3.00 | 13,300 | 2.51 | 0.03 | 0.16 | 2.59 | 2.51 |

| 21-Jun-51 | 1.75 | 15,000 | 2.52 | 0.03 | 0.17 | 2.59 | 2.52 |