Summary: 10-year bond yields considerably higher in Australia, less so in US, other major northern-hemisphere markets; ACGB 10-year spread to US Treasury yield widens from +6bps to +28bps; RBA buys $4 billion of various ACGBs, final purchases under current programme; AOFM issues $5.15 billion worth of bonds, notes.

Sovereign 10-year bond yields finished the week considerable higher in Australia, while upward movements in the US and other major northern-hemisphere markets were more restrained.

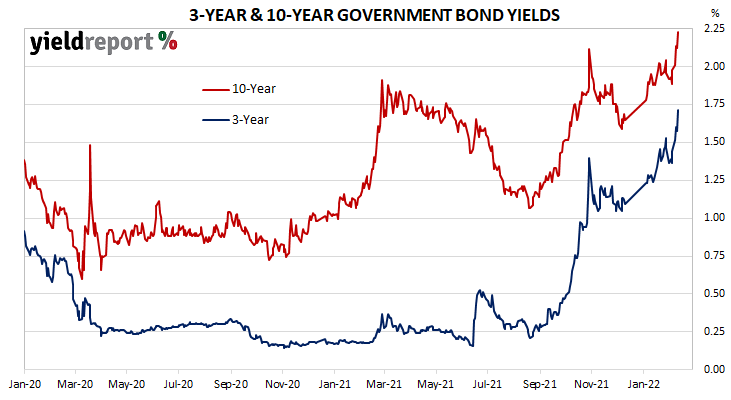

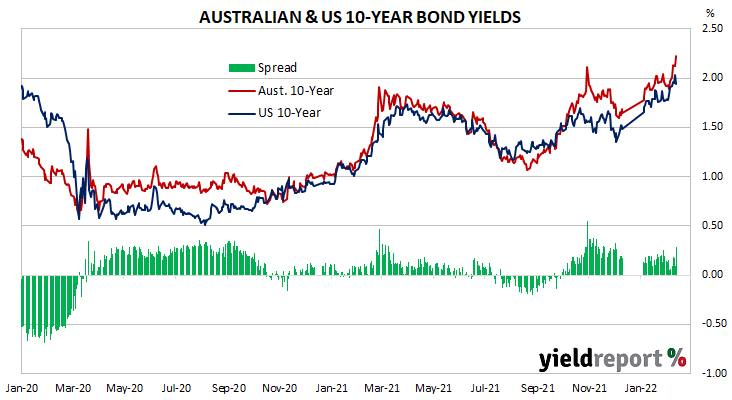

Locally, long-term ACGB yields generally increased materially over the week, with large jumps on Tuesday and Friday. By the end of the week, the 3-year ACGB yield had gained 28bps to 1.72%, the 10-year yield had added 25bps to 2.22% while the 20-year yield finished 22bps higher at 2.67%. The spread between US and Australia 10-year Treasury bond yields widened from +6bps to +28bps.

The RBA purchased another $4.0 billion worth of various ACGBs and semis with maturities from April 2024 to May 2032 over the week. The purchases will be the last under the Bank’s current bond purchase programme as per the RBA’s announcement in the previous week. A total of $280.7 billion of bonds were purchased under the programme and a review is slated for May as to whether maturing bonds will be reinvested or not.

Over in the US, long-term bond yields moved higher over much of the week before falling noticeably at the end of it.

There were only couple of notable US economic reports and both came out in the latter part of the week.

The first notable report of the US week was released on Thursday. January’s CPI report exceeded market expectations, sending the annual rate to 7.5%. One local economist described US inflation as “rampant”.

The weekly initial jobless claims report was also released as usual. Total claims amounted to 0.223 million for the week to Saturday 5 February, 16,000 fewer claims than in the previous week after revisions. As at 29 January, continuing claims (seasonally adjusted) totalled 1.621 million, unchanged from the previous week’s total after revisions.

The next day, US consumer sentiment further softened in February. The University of Michigan’s Consumer sentiment index fell from 67.2 to 61.7, “reaching its worst level in a decade.”

By this point, the US 2-year Treasury bond yield had gained 20bps to 1.51%, the 10-year yield had added 3bps to 1.94% while the 30-year yield finished 4bps higher at 2.25%.

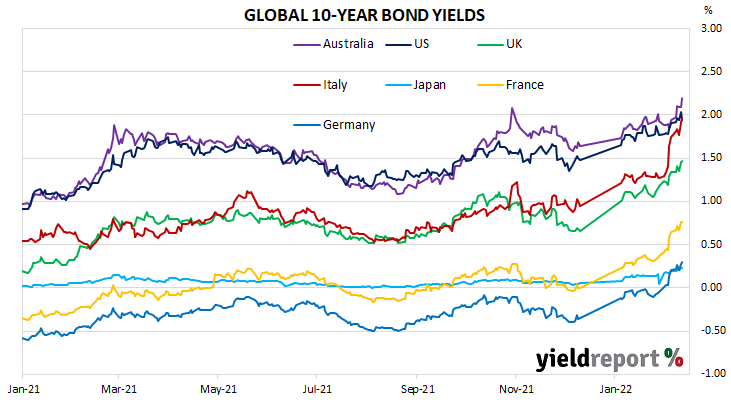

In major euro-zone markets, 10-year bond yields increased through much of the week, with just one down day midweek. There were no particularly notable euro-zone reports released.

By the end of the week, the German 10-year bund yield had gained 9bps to 0.30% and the French 10-year OAT yield had gained 12bps to 0.76%. The Italian 10-year BTP yield added 21bps to 1.95% over the week while the British 10-year gilt yield finished 13bps higher at 1.47%.

The AOFM held three vanilla bond tenders and one index-linked bond (ILB) tender during the week. $1 billion of May 2041s, $1 billion of November 2032s and $1 billion of November 2024s were priced at yields of 2.49%, 2.14% and 1.49% respectively while the August 2040 ILBs were priced at a real yield of 0.25%.

There were also two Treasury note tenders which raised $2 billion on a short-term basis.

The gross value of all bonds issued by the AOFM in the 2021/2022 financial year-to-date (not taking into account buy-backs or short-term Treasury note tenders) is $59.45 billion. There are currently $789.813 billion of Treasury bonds and $41.257 billion of Treasury index-linked bonds on issue. The next series to mature does so on 21 February when $5.121 billion worth of index-linked bonds are due. There are also $39.00 billion of short-term Treasury notes currently outstanding.

| MATURITY | COUPON (%) | ISSUE SIZE ($M) | CLOSING YIELD | Δ WEEK | Δ MONTH | WEEK HIGH | WEEK LOW |

|---|---|---|---|---|---|---|---|

| 21-Nov-22 | 2.25 | 26,500 | 0.40 | 0.11 | 0.03 | 0.40 | 0.33 |

| 21-Apr-23 | 5.50 | 34,200 | 0.75 | 0.17 | 0.17 | 0.75 | 0.63 |

| 21-Apr-24 | 2.75 | 34,400 | 1.19 | 0.25 | 0.35 | 1.19 | 1.00 |

| 21-Nov-24 | 0.25 | 37,600 | 1.51 | 0.28 | 0.41 | 1.51 | 1.31 |

| 21-Apr-25 | 3.25 | 37,100 | 1.66 | 0.27 | 0.35 | 1.66 | 1.46 |

| 21-Nov-25 | 0.25 | 22,000 | 1.80 | 0.28 | 0.35 | 1.80 | 1.60 |

| 21-Apr-26 | 4.25 | 37,100 | 1.83 | 0.28 | 0.34 | 1.83 | 1.63 |

| 21-Sep-26 | 0.50 | 32,800 | 1.90 | 0.28 | 0.33 | 1.90 | 1.69 |

| 21-Apr-27 | 4.75 | 33,900 | 1.92 | 0.28 | 0.33 | 1.92 | 1.72 |

| 21-Nov-27 | 2.75 | 29,700 | 1.98 | 0.27 | 0.32 | 1.98 | 1.78 |

| 21-May-28 | 2.25 | 29,700 | 2.04 | 0.28 | 0.32 | 2.04 | 1.82 |

| 21-Nov-28 | 2.75 | 32,100 | 2.07 | 0.27 | 0.30 | 2.07 | 1.84 |

| 21-Apr-29 | 3.25 | 33,000 | 2.09 | 0.27 | 0.30 | 2.09 | 1.87 |

| 21-Nov-29 | 2.75 | 32,900 | 2.12 | 0.27 | 0.29 | 2.12 | 1.90 |

| 21-May-30 | 2.50 | 36,600 | 2.14 | 0.26 | 0.28 | 2.14 | 1.92 |

| 21-Dec-30 | 1.00 | 24,700 | 2.17 | 0.26 | 0.27 | 2.17 | 1.95 |

| 21-Jun-31 | 1.50 | 36,300 | 2.18 | 0.25 | 0.27 | 2.18 | 1.96 |

| 21-Nov-31 | 1.00 | 21,000 | 2.20 | 0.25 | 0.27 | 2.20 | 1.98 |

| 21-May-32 | 1.25 | 31,200 | 2.21 | 0.25 | 0.26 | 2.21 | 1.99 |

| 21-Apr-33 | 4.50 | 18,800 | 2.22 | 0.25 | 0.26 | 2.22 | 2.00 |

| 21-Jun-35 | 2.75 | 9,050 | 2.36 | 0.25 | 0.25 | 2.36 | 2.14 |

| 21-Apr-37 | 3.75 | 12,000 | 2.44 | 0.23 | 0.22 | 2.44 | 2.24 |

| 21-Jun-39 | 3.25 | 9,900 | 2.57 | 0.23 | 0.22 | 2.57 | 2.38 |

| 21-May-41 | 2.75 | 13,500 | 2.65 | 0.22 | 0.19 | 2.65 | 2.46 |

| 21-Mar-47 | 3.00 | 13,300 | 2.74 | 0.22 | 0.18 | 2.74 | 2.66 |

| 21-Jun-51 | 1.75 | 15,000 | 2.74 | 0.22 | 0.17 | 2.74 | 2.56 |