Summary: .

For the week ending July 13, 2025, the Australian government bond market recorded modest gains, reflecting a cautious market response to the RBA’s decision to hold the cash rate at 3.85% and the global fiscal stimulus from the “One Big Beautiful Bill” (OBBBA). The benchmark 10-year yield increased 14 basis points to 4.33%, while the 2-year yield rose 5 basis points to 3.40%. The 15-year yield edged up 8 basis points to 4.66%, and the 5-year yield climbed 8 basis points to 3.71%.

Swap rates also rose, with the 3-year rate up 11.83 basis points to 3.3708%, the 5-year up 11.67 basis points to 3.773%, and the 10-year up 9.98 basis points to 4.2313%, signalling adjusted expectations of future RBA policy amid the OBBBA’s impact. The May CPI data, showing a trimmed mean of 2.1% year-on-year per the Australian Bureau of Statistics, continues to support rate cut speculation, with markets now pricing a 100-basis point reduction over the next year, targeting a 2.85% cash rate by mid-2026, though bank forecasts like ANZ’s 3.35% by December 2025 suggest a more tempered outlook.

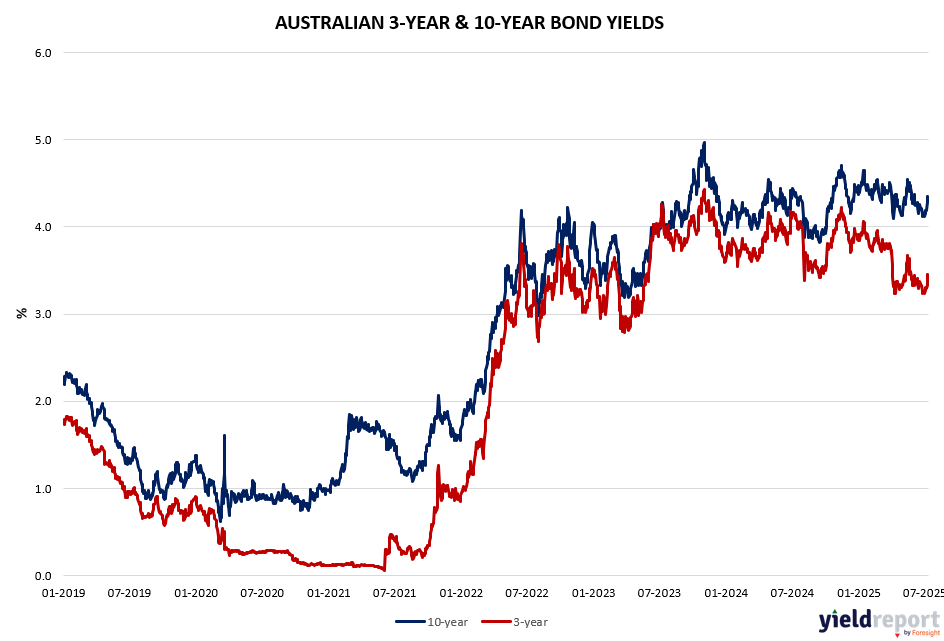

Figure 1: Aust. 10 yr minus 3 yr Bond Spread

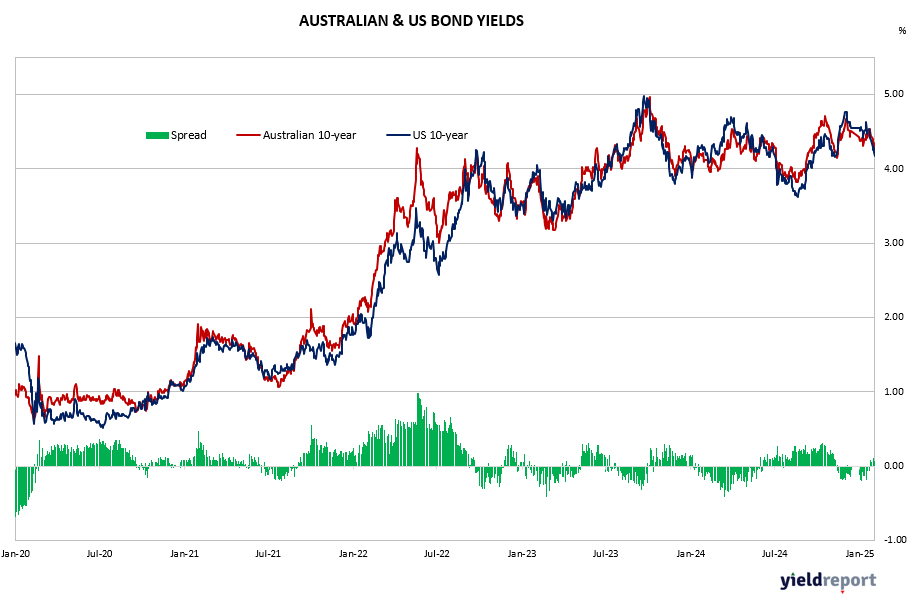

Figure 2: Australian & US Bond Yields

Figure 3: US 10 yr minus 2 yr Bond Spread