Summary:

Australia’s economy expanded 0.6% in Q2 2025 and 1.8% year-on-year, marking the first annual rise in GDP per capita since early 2023. Growth was led by household consumption, which rose 0.9%—the strongest quarterly gain since late 2022—driven by rising real disposable incomes (+4.1% YoY), tax relief, rate cuts, and easing inflation. Goods spending (+1.0%) outpaced services (+0.8%), supported by EOFY discounts, early import deliveries, and holiday-related demand.

Residential construction remained soft (+0.4%), while private business investment declined, except for intellectual property products. Public investment fell 7% over three quarters, dampening activity in construction and real estate. Government spending added 0.2 percentage points to growth, mainly through health and infrastructure. Net exports contributed modestly, with services exports offsetting weaker resource flows. Inventory drawdowns subtracted 0.2 points.

Overall, growth is supported by resilient consumption, targeted public demand, and exports, while private investment and inventory trends remain uneven. Forecasts for GDP have been lifted to 2.2% in 2025 and 2.6% in 2026, though business investment is expected to stay subdued.

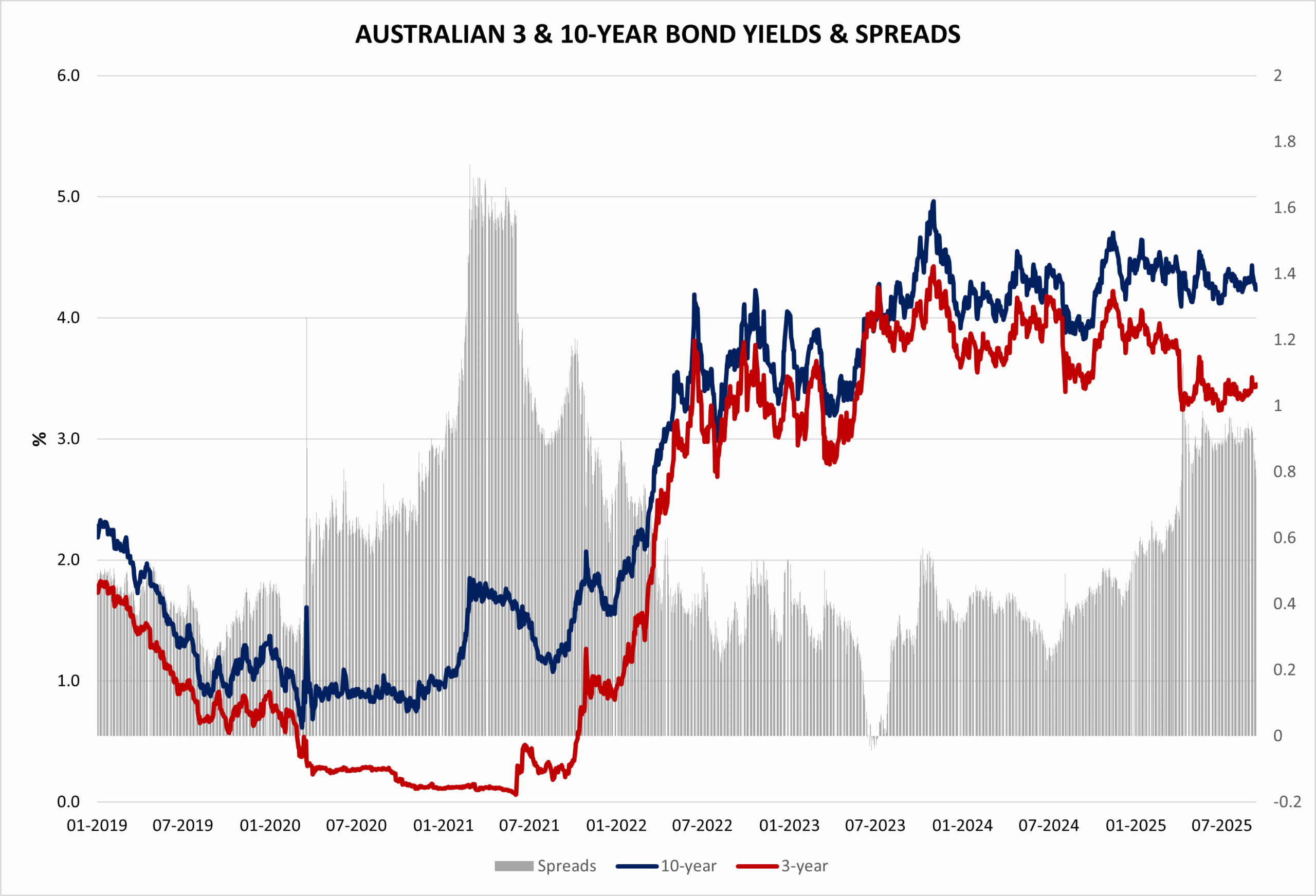

This week, the cash rate held at 3.60%, with short-term yields stable. Long-term bond yields eased slightly, narrowing the 3–10 year spread, reflecting cautious sentiment and limited upward pressure on rates.

Figure 1: Aust. 3 yr minus 10 yr Bond Spread

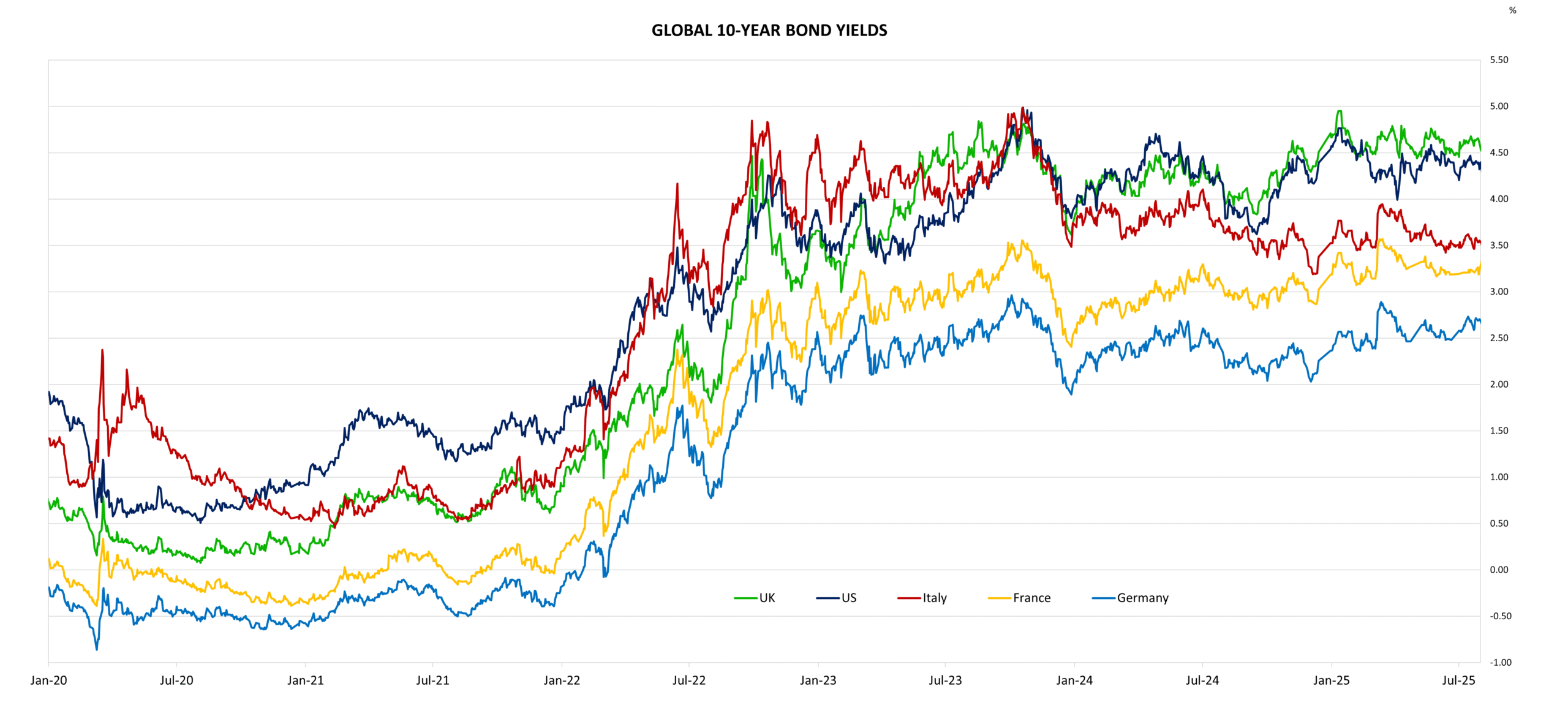

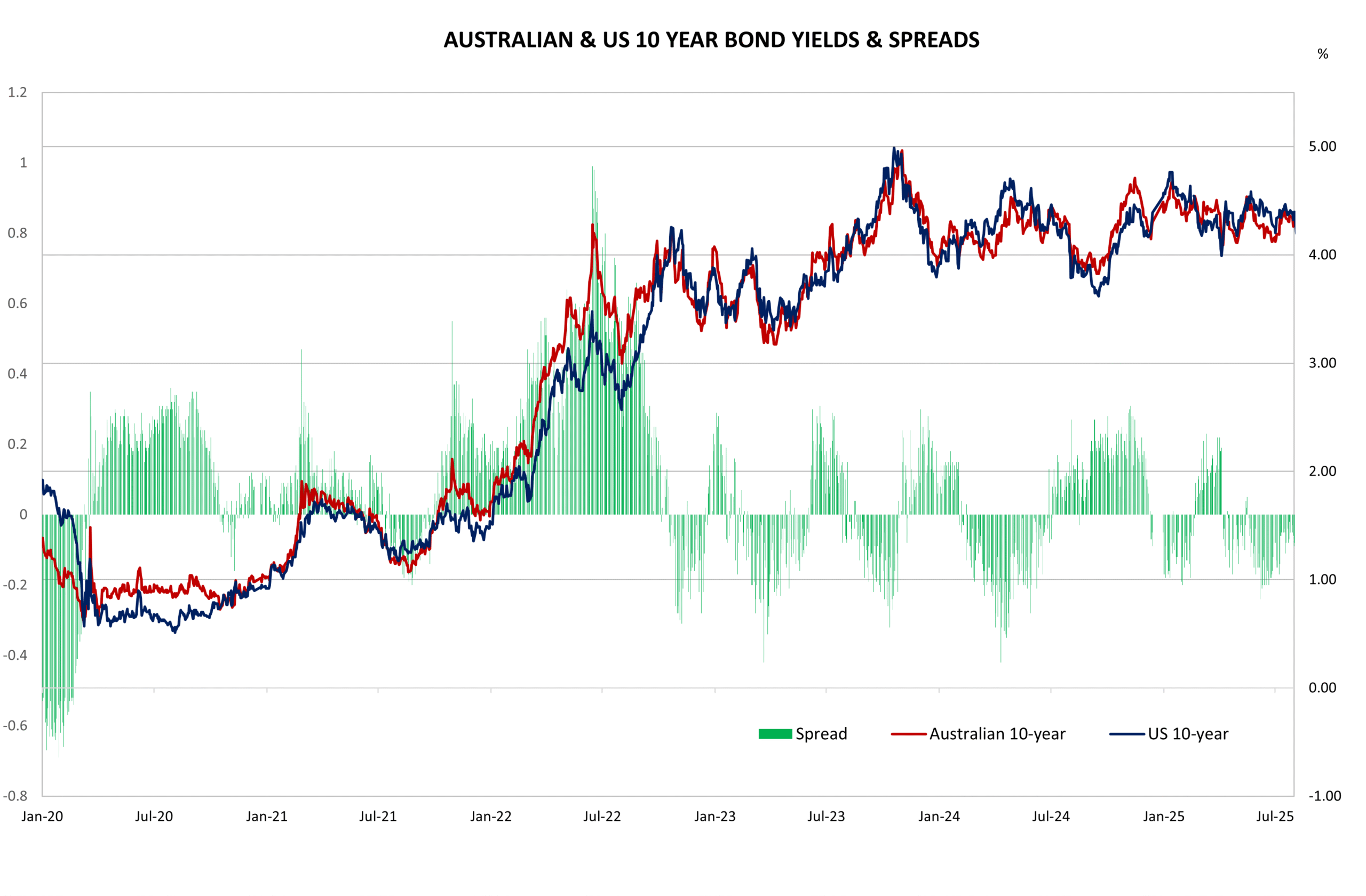

Figure 2: Australian & US Bond Yields

Figure 3: US 10-year minus 2-year Bond Spread