Summary:

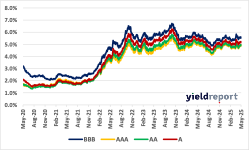

Figure 1:US Investment Grade Bonds Effective Yields Figure 2: US Investment Grade Bonds OAS Spreads.

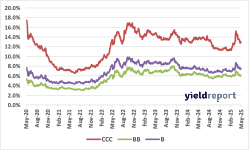

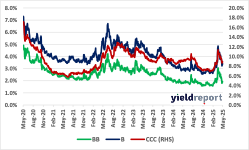

Figure 3: US High-Yield Bonds Effective Yields. Figure 4: US High-Yield Bonds OAS Spreads

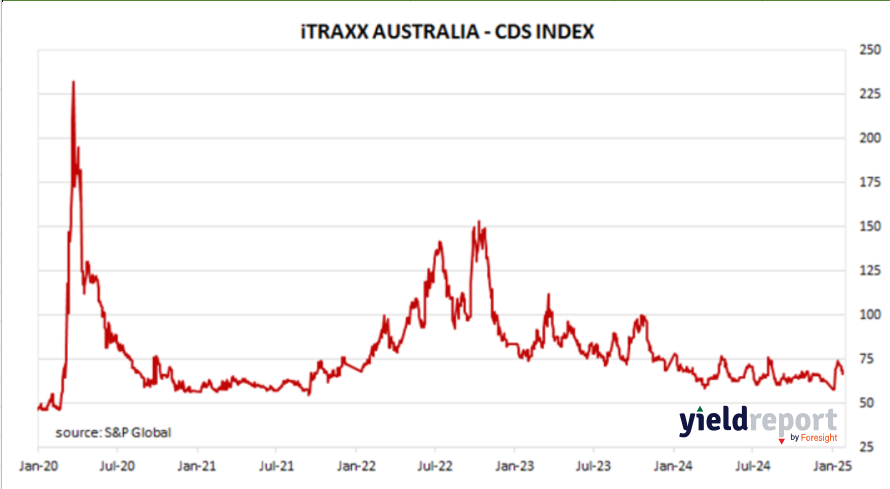

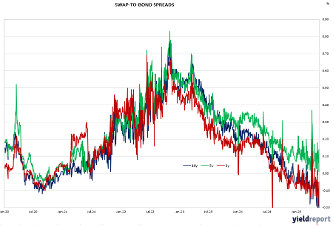

Figure 5: ITRAXX Australia – CDS Index Figure 6: Australian Swap to Bond Spreads