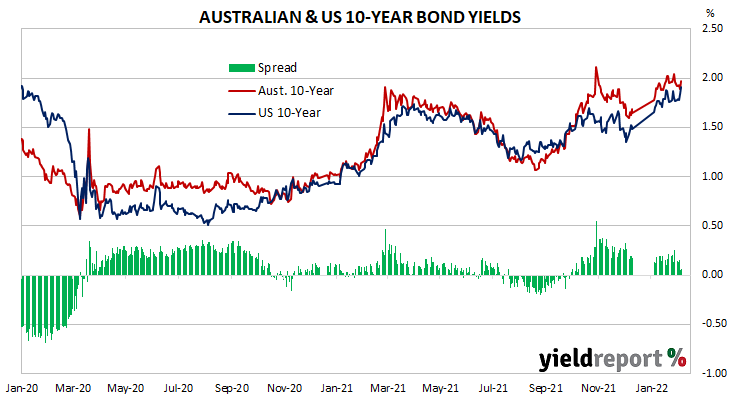

Summary: 10-year bond yields a touch higher in Australia but noticeably higher in US, other major northern-hemisphere markets; ACGB 10-year spread to US Treasury yield tightens from +19bps to +6bps; RBA buys $4 billion of various ACGBs, final purchases under current programme next week; AOFM issues $4 billion worth of bonds, notes.

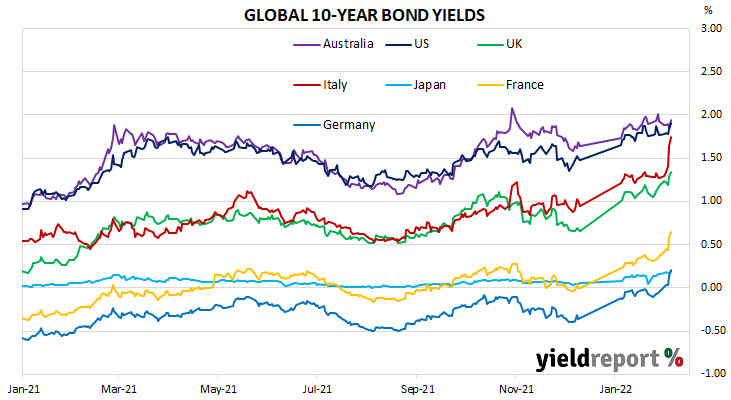

Sovereign 10-year bond yields finished the week a touch higher in Australia but considerably higher in the US and other major northern-hemisphere markets.

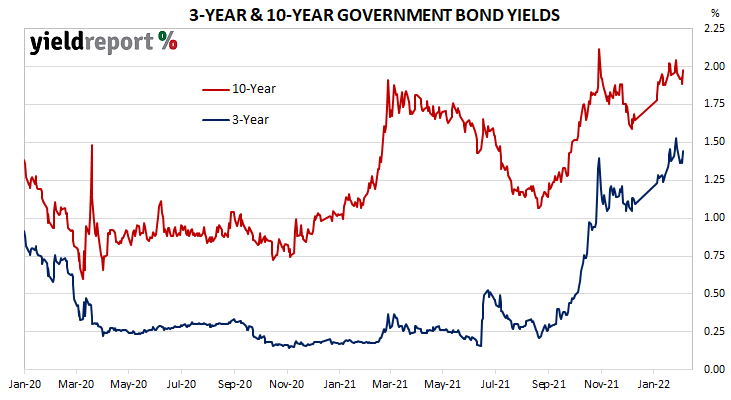

Locally, long-term ACGB yields generally declined over the first four days of the week before jumping on Friday. By this point, the 3-year ACGB yield had lost 3bps to 1.44%, the 10-year yield had inched up 1bp to 1.95% while the 20-year yield finished unchanged at 2.45%. The spread between US and Australia 10-year Treasury bond yields tightened from +19bps to +6bps.

The RBA purchased another $4.0 billion worth of various ACGBs and semis with maturities from April 2024 to April 2033 over the week. Purchases under the Bank’s current bond purchase programme will end next week as per the RBA’s announcement on Tuesday. A total of $276.7 billion of bonds have been purchased under the programme and a review is slated for May as to whether maturing bonds will be reinvested or not.

Over in the US, long-term bond yields crept up over the few days of the week before increasing materially on Thursday and Friday.

There were a bunch of US economic reports released for a second week running.

The first notable report of the US week was released on Tuesday. December’s JOLTS report indicated the US quit rate had declined a little while remaining close to its all-time high.

The ISM’s January Manufacturing PMI report was released on the same day. The index slipped a little but the change appears to be related to fewer supply-chain disruptions.

Midweek, the ADP January report missed market expectations but it was generally viewed as a temporary setback given bounces from previous coronavirus waves.

On Thursday, the ISM’s services activity index declined from 62.0 to 59.9 in January, largely in line with the 59.5 which had been generally expected.

The weekly initial jobless claims report was also released as usual. Total claims amounted to 0.238 million for the week to Saturday 29 January, 23,000 fewer claims than in the previous week after revisions. As at 22 January, continuing claims (seasonally adjusted) totalled 1.628 million, a 44,000 fall from the previous week’s total after revisions.

At the end of the week, January’s non-farm payrolls report produced a much higher rise in employment than expected, with employment rising by 467,000. However, the jobless rate ticked up from 3.9% to 4.0% as the participation rate rose.

By this point, the US 2-year Treasury bond yield had gained 15bps to 1.31% while 10-year and 30-year yields both finished 14bps higher at 1.91% and 2.21% respectively.

In major euro-zone markets, 10-year bond yields increased through the week, especially so on Thursday.

December quarter GDP figures were released at the start of the week. The euro-zone economy expanded by 0.3%, slightly below the 0.4% expected, taking the annual growth rate from 3.9% to 4.6%.

Eurozone unemployment figures were released the next day. The jobless rate declined from December’s revised rate of 7.1% to 7.0%, the lowest rate since the series began in 1998.

Midweek, the “flash” January consumer price index (CPI) report produced an annual inflation rate of 5.1% in the euro-zone, above expectations and slightly higher than December’s final reading of 5.0%. However, core annual CPI fell back from 2.6% to 2.3%.

The ECB Governing Council left policy rates unchanged at its latest policy meeting on Thursday but outlined a reduction schedule for the amount of bonds purchased each month under its Pandemic Emergency Purchases Programme. Additionally, ECB President Christine Lagarde stated all members of the Governing Council have inflation concerns.

At about the same time, the Bank of England raised Bank Rate from 0.25% to 0.50%, its second increase in as many months. It also said it will start to unwind its £895 billion quantitative easing programme by allowing the government bonds it holds to mature without re-investing the proceeds.

By the end of the week, the German 10-year bund yield had jumped 26bps to 0.21% and the French 10-year OAT yield had gained 27bps to 0.64%. The Italian 10-year BTP yield added 47bps to 1.74% over the week while the British 10-year gilt yield finished 17bps higher at 1.34%.

The AOFM held two bond tenders during the week. $1 billion of November 2031s and $1 billion of November 2025s were priced at yields of 1.93% and 1.51% respectively. Their respective coverage ratios were 3.2 and 4.3.

There were also two Treasury note tenders which raised $2 billion on a short-term basis.

The gross value of all bonds issued by the AOFM in the 2021/2022 financial year-to-date (not taking into account buy-backs or short-term Treasury note tenders) is $56.3 billion. There are currently $786.813 billion of Treasury bonds and $41.107 billion of Treasury index-linked bonds on issue. The next series to mature does so on 21 February when $5.121 billion worth of index-linked bonds are due. There are also $37.00 billion of short-term Treasury notes currently outstanding.

| MATURITY | COUPON (%) | ISSUE SIZE ($M) | CLOSING YIELD | Δ WEEK | Δ MONTH | WEEK HIGH | WEEK LOW |

|---|---|---|---|---|---|---|---|

| 21-Nov-22 | 2.25 | 26,500 | 0.29 | -0.08 | 0.06 | 0.32 | 0.26 |

| 21-Apr-23 | 5.50 | 34,200 | 0.58 | -0.04 | 0.23 | 0.58 | 0.54 |

| 21-Apr-24 | 2.75 | 34,400 | 0.94 | -0.01 | 0.29 | 0.94 | 0.86 |

| 21-Nov-24 | 0.25 | 37,600 | 1.23 | 0.00 | 0.31 | 1.23 | 1.13 |

| 21-Apr-25 | 3.25 | 37,100 | 1.39 | -0.02 | 0.29 | 1.39 | 1.31 |

| 21-Nov-25 | 0.25 | 22,000 | 1.52 | -0.01 | 0.29 | 1.52 | 1.43 |

| 21-Apr-26 | 4.25 | 37,100 | 1.55 | -0.01 | 0.28 | 1.55 | 1.46 |

| 21-Sep-26 | 0.50 | 32,800 | 1.62 | -0.02 | 0.28 | 1.62 | 1.54 |

| 21-Apr-27 | 4.75 | 33,900 | 1.65 | -0.01 | 0.28 | 1.65 | 1.56 |

| 21-Nov-27 | 2.75 | 29,700 | 1.71 | 0.00 | 0.28 | 1.71 | 1.63 |

| 21-May-28 | 2.25 | 29,700 | 1.76 | 0.01 | 0.30 | 1.76 | 1.69 |

| 21-Nov-28 | 2.75 | 32,100 | 1.79 | 0.01 | 0.30 | 1.79 | 1.73 |

| 21-Apr-29 | 3.25 | 33,000 | 1.82 | 0.02 | 0.30 | 1.82 | 1.75 |

| 21-Nov-29 | 2.75 | 32,900 | 1.85 | 0.02 | 0.30 | 1.85 | 1.79 |

| 21-May-30 | 2.50 | 36,600 | 1.88 | 0.02 | 0.30 | 1.88 | 1.81 |

| 21-Dec-30 | 1.00 | 24,700 | 1.91 | 0.02 | 0.30 | 1.91 | 1.85 |

| 21-Jun-31 | 1.50 | 36,300 | 1.93 | 0.02 | 0.30 | 1.93 | 1.86 |

| 21-Nov-31 | 1.00 | 21,000 | 1.94 | 0.02 | 0.31 | 1.94 | 1.88 |

| 21-May-32 | 1.25 | 31,200 | 1.96 | 0.02 | 0.30 | 1.96 | 1.89 |

| 21-Apr-33 | 4.50 | 18,800 | 1.97 | 0.02 | 0.30 | 1.97 | 1.90 |

| 21-Jun-35 | 2.75 | 9,050 | 2.11 | 0.01 | 0.26 | 2.11 | 2.05 |

| 21-Apr-37 | 3.75 | 12,000 | 2.21 | 0.01 | 0.22 | 2.21 | 2.14 |

| 21-Jun-39 | 3.25 | 9,900 | 2.34 | 0.01 | 0.20 | 2.34 | 2.26 |

| 21-May-41 | 2.75 | 13,000 | 2.42 | 0.00 | 0.18 | 2.42 | 2.35 |

| 21-Mar-47 | 3.00 | 13,300 | 2.52 | 0.00 | 0.17 | 2.52 | 2.44 |

| 21-Jun-51 | 1.75 | 15,000 | 2.52 | 0.00 | 0.17 | 2.52 | 2.44 |