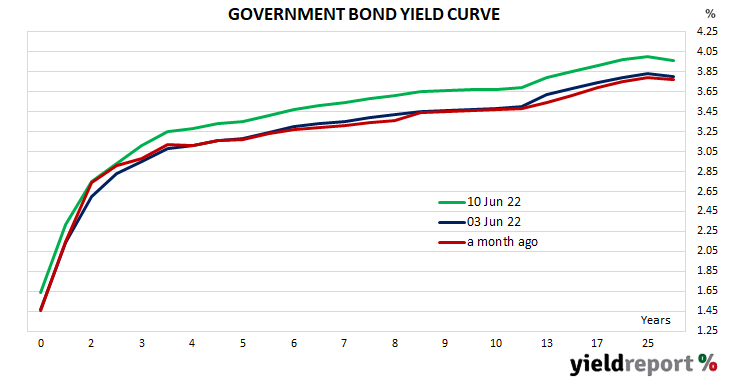

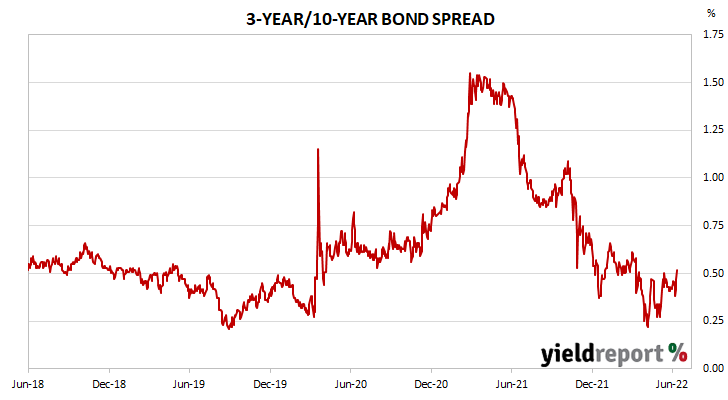

Summary: ACGB curve steeper; US Treasury curve generally flatter.

The gradient of the ACGB yield curve became steeper as long-term yields outpaced rises at the short end. By the end of the week, the 3-year/10-year spread had gained 6bps to 52bps while the 3-year/20-year spread had gained 5bps to 81bps.

In contrast, the traditional measures of the gradient of the US Treasury curve finished the week noticeably flatter. The 2-year/10-year spread narrowed by 16bps to 10bps while the 2 year/30 year spread shed 28bps to 13bps over the week. However, the San Francisco Fed’s favoured recession-predicting measure, the 3-month/10-year Treasury spread, finished 7bps wider at 183bps.