Summary:

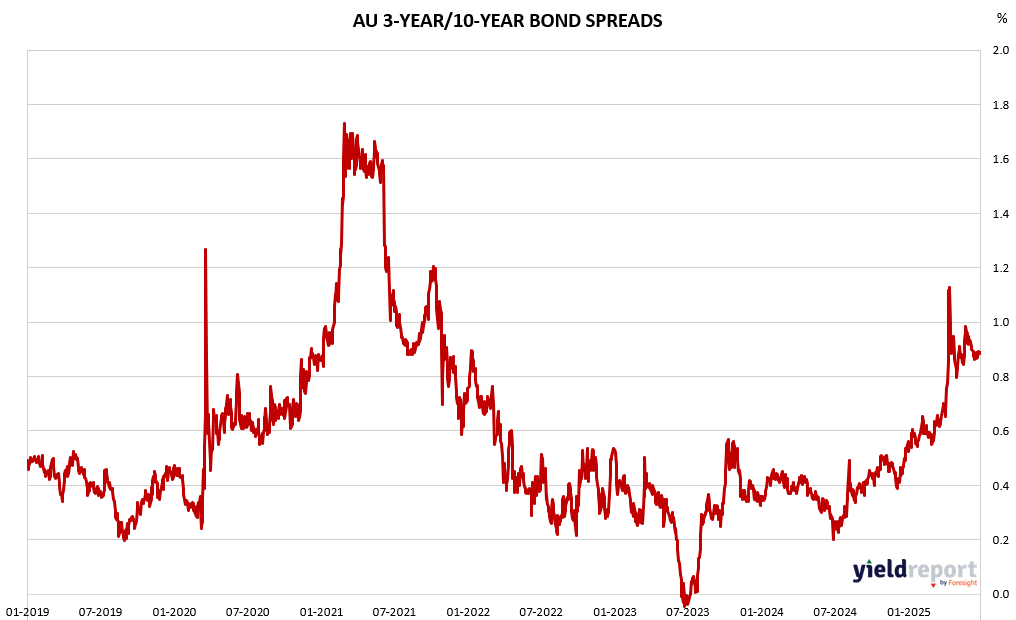

The Australian bond market continued its recent trend of softening yields on 20 June, reflecting a cautious but steady investor sentiment ahead of key economic data releases. The 10-year bond yield eased to 4.22%, down 3.3 bps. The 3-year yield slipped to 3.36% (−1.4 bps), while 20- and 30-year bond yields declined to 4.82% and 4.92% respectively.

This across-the-curve decline suggests a market in a holding pattern, with investors positioning defensively amid expectations of a potential RBA pivot. The Bloomberg AusBond Composite Index rose by 0.09%, signaling cautious optimism as investors favor fixed income while awaiting clearer signals from central banks.

Markets are pricing in a 90 bps rate cut over the next year, targeting a 2.85% cash rate. However, investors remain watchful for developments on tariffs and geopolitics.

Exhibit 1: Australian 10-yr minus 3-yr Spread

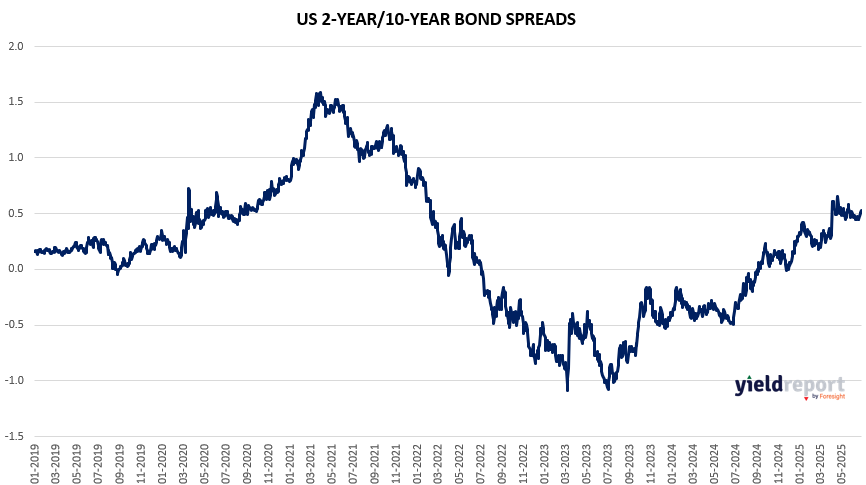

Exhibit 2: US 10-yr minus 2-yr Spread

To learn more about yield curves and their predictive power, visit this article or this one.