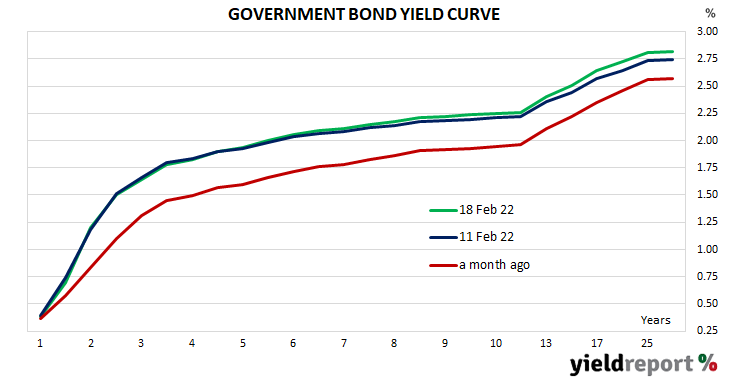

Summary: ACGB gradient steeper; US Treasury curve gradient also steeper.

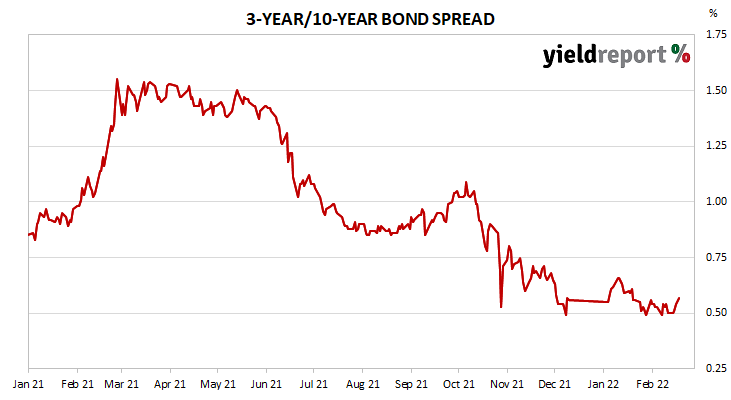

The gradient of the ACGB yield curve became steeper as yields fell at the short end and rose elsewhere. By the end of the week, the 3-year/10-year spread had widened by 7bps to 57bps and the 3-year/20-year spread had gained 10bps to 105bps.

The gradient of the US Treasury curve also became steeper. The 2-year/10-year spread widened by 3bps to 46bps over the week while the 2 year/30 year spread gained 4bps to 78bps. However, the San Francisco Fed’s favoured recession-predicting measure, the 3-month/10-year Treasury spread, finished unchanged at 158bps.