| Name | Daily Close | Daily Change | Daily Change (%) |

|---|---|---|---|

| Dow | 38,314.86 | -2,231.07 | -5.50% |

| S&P 500 | 5,074.08 | -322.44 | -5.97% |

| Nasdaq | 15,587.79 | -962.82 | -5.82% |

| VIX | 45.31 | 15.29 | 50.93% |

| Gold | 3,035.40 | -86.3 | -2.76% |

| Oil | 61.99 | -4.96 | -7.41% |

US MARKET

Wow, the US markets roiled on Friday. And if you thought the US equities market on Thursday was interesting, it was nevertheless trumped by Friday’s intra-day developments. The tone of calls with clients on Friday were reportedly very different to Thursday. Intra-day moves were fascinating, and a summary is illustrative in terms of what is driving markets regarding tariffs.

China had announced reciprocal tariffs (wait for the EU likely this week). By 10:45am NY time, both the S&P 500 and Nasdaq 100 were down 5%. Volume was off the charts, the VIX peaked at 44, and business media commentators were reminding viewers that the circuit breaker kicks in at -7% and the last time such an event occurred was March 18 2020. It was the largest sell-off since March 2020 and the sell-off was broad based. The market was completely ignoring the strong jobs report.

Then at around 11am, Trump posted on Truth Social that he had a call with the Vietnamese Prime Minister who expressed his desire to reduce US tariffs to zero. Evidence of an Exit Ramp. Stocks began to pare losses to a degree, 10-year treasury yield backed up 10 bps, and the Yen pulled back.

Then the J Powell headlines began to hit the wires. “Transitory” has been dropped from his narrative, now saying that it’s possible tariffs could have a persistent inflationary, and the economic impact of new tariffs is likely to be significantly larger than expected, and the central bank must make sure that doesn’t lead to a growing inflation problem. The emphasis from J Powell was on managing inflation rather than a growth downturn, and it was a stagflation risk message. That is, rates are on hold until things become clear.

While Friday was wild, you can make an argument that, to date, the selling has been orderly. Global investors have been all in on equities, all in on US exceptionalism, and all in on the Mag 7 / AI. And now comes the repatriation of capital to what are comparative safe havens like Australia, the EU, and maybe even the UK. And after a decade, at least of trillions of dollars of foreign investment capital flowing into the US, this great unwind will likely impact the US dollar (it did on Thursday when traditionally the dollar should have rallied). And a weakening USD will only add to the inflationary impacts of the tariffs in the US.

At the close, the S&P 500 fell 6.2%. The Nasdaq 100 fell 6.1%. The Dow Jones Industrial Average fell 5.5%. The S&P 5000 racked up its worst two-day plunge since March 2020 in a selloff that slashed over $5 trillion in value. Investment banks, like JP Morgan got hammered due to a combined effect on its customer base and M&A activity. Alternative managers, like Apollo and KKR, similarly due to the PE markets being on hold (a whole separate conversation regarding private equity fund issues).

The latest jobs report showed resilience, but that was before aggressive levies start making their way through the economy. The market effectively ignored the report, despite being stronger than expected.

The fastest US stock market selloff since the depths of the Covid pandemic has left valuations looking cheap. But if a recession is inevitable due to the global trade war, the definition of inexpensive becomes relative, and analysts are notoriously slow adjusting earnings downwards. Historically, the S&P 500’s trailing price-to-earnings ratio slides to an average of 15.6 during routs that precede economic downturns, according to data compiled by Sam Stovall at research firm CFRA. It’s currently around 22 despite the recent selloff.

LOCAL MARKET

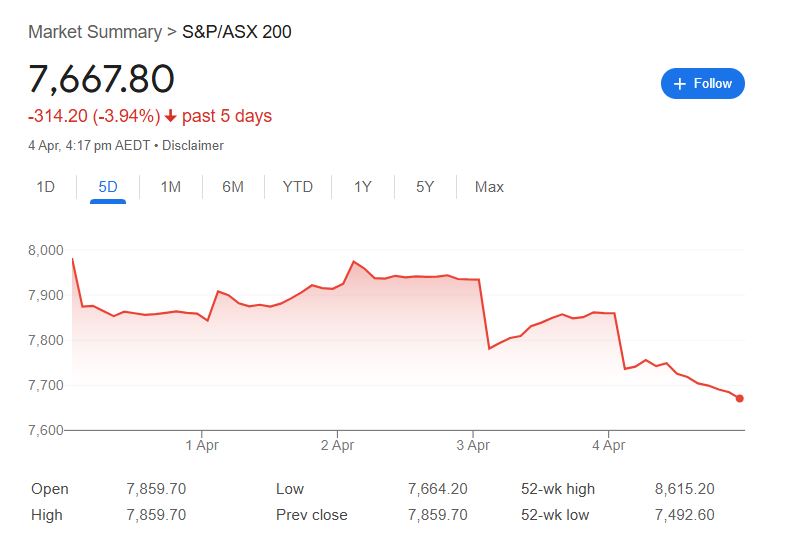

Meanwhile in Australia, the S&P/ASX 200 Index fared comparatively very well on the critical 2 days post the tariff announcements, down circa only 1-2% on both Thursday and Friday.

There are a range of clear reasons for this comparatively strong performance and why indeed the Australian equities market may be viewed as a safe haven (in a global equities market context) and the US market the contrary. Wow, how things change.

Clearly, the Australian consumers and businesses are not being subject to a tax called tariffs. Any economic hit will be indirect – that is, via a slowdown in our major trading partners. Domestically facing and defensive businesses performed the best over Thursday and Friday. Commodities the worst. Australian stocks exposed to China have been a significant laggard despite evidence that demand for commodities is starting to recover.

Additionally, the Australian economy is showing signs of improving as tax cuts and falling inflation boost disposable income. Further, the RBA was also late to start its easing cycle compared to other central banks, meaning the boost from looser policy has more to run.

We also wonder whether there may be a degree of country rotation out of the US back into Australia, given the comparatively lower risks. Certainly, this repatriation of capital out of the US is certainly gather steam global, it may well have marked implications on the USD.