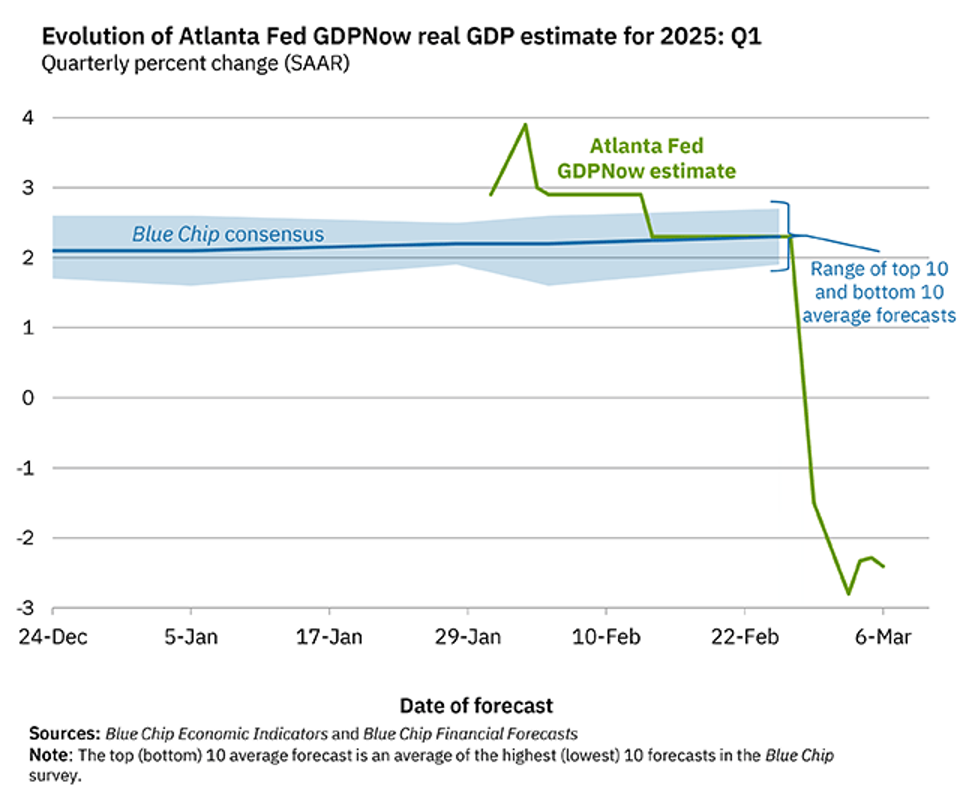

The Atlanta Fed’s GDPNow model (nowcasting) lowered its Q1 US GDP forecast significantly on Friday. The volatile model swung in response to January’s surge in imported goods ahead of Trump’s tariffs.

In addition, consumer spending was depressed by a colder-than-usual January, so it is likely consumer spending, and the model will rebound in February.

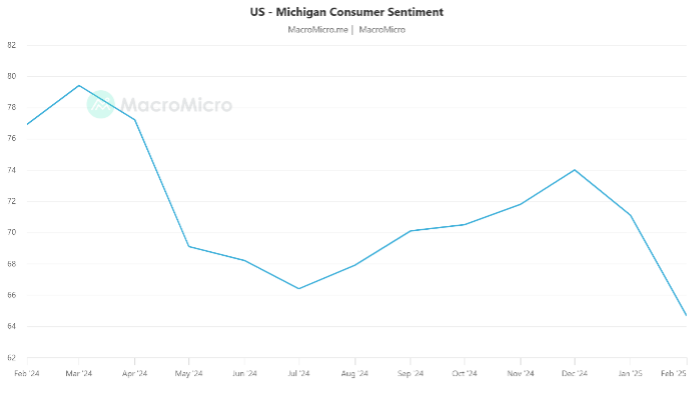

However, US Consumer and Business Sentiment over the last 4 weeks has dropped off a cliff. Like, completely off a cliff. It started with the University of Michigan survey and just kept rolling. While we aren’t seeing this yet in the economic data, “yet” is the operative word in making sense of all this

In the US, the consumer is 60% of the economy, but 50% of that 60% (30%) is accounted for by the richest 10% in the country. And when the stock market is getting rolled, or highly uncertain, may affect the spending patterns of this cohort. This cohort, a decent slab of which are retirees and therefore all income is asset returns based, have done exceptionally well over the last few years, be it equities, bonds, private debt

As for the other 90% – tariffs are regressive – they impact the poor more significantly through the inflation impact. And they are nervous which is being reflected in broad consumer sentiment data

Businesses are too. And in times of uncertainty the sensible thing to do is say “well, you know what, lets just take a pause for the time being”. Currently, with a day having almost 6 months’ worth of macro announcements, of course they are taking a pause. Granted, corporate America came through the recent earnings season in a strong position and CY25 EPS growth for the S&P 500 was upgraded meaningfully from 8% to 15%. But that was almost a month ago.

If you’re searching for a bearish narrative, take your pick. Among the many economic challenges ahead cited by the growing cohort of bears are:

- Fiscal stimulus will diminish, weighing directly on GDP. In other words, a fiscal cliff is coming soon.

- Consumers will retrench because they are too leveraged or have run out of excess savings.

- The positives of Trump 2.0’s pro-business stance are outweighed by the negatives of policy uncertainty, drummed up by daily executive orders and tariff announcements. This uncertainty will restrain capital spending and is already spurring a slowdown in the services economy.

- The Department of Government Efficiency (DOGE) is slashing the federal workforce and contracted workers. That will jack up unemployment and knock down consumer spending.

- Should DOGE fail in its aims of narrowing the budget and slowing the growth in federal spending, then higher interest rates and a fiscal crisis are inevitable. Corporate defaults, slimmer profit margins, and lower stock prices surely would follow. The reduced net wealth effect would weigh doubly on consumer spending. Construction employment would suffer from the housing market malaise under higher rates.

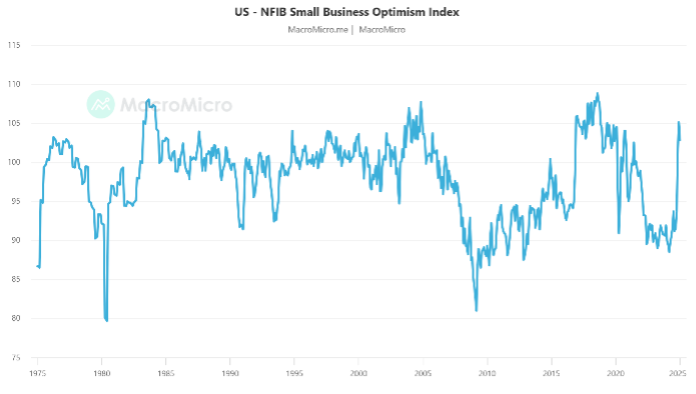

| Exhibit 1: US Business Uncertainty Index |

Exhibit 2: US Consumer Sentiment