Commentary courtesy of Spectrum Asset Management’s Lindsay Skardoon.

| Close | Prev Close |

Change | |

| Aust. 90 day bank bill% | 1.92 | 1.85 | 0.07 |

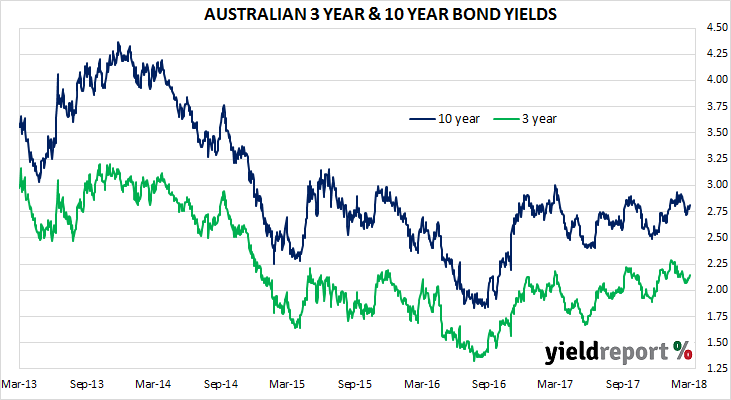

| Aust. 3 year bond%* | 2.15 | 2.12 | 0.03 |

| Aust. 10 year bond%* | 2.81 | 2.77 | 0.04 |

| Aust. 20 year bond%* | 3.22 | 3.18 | 0.04 |

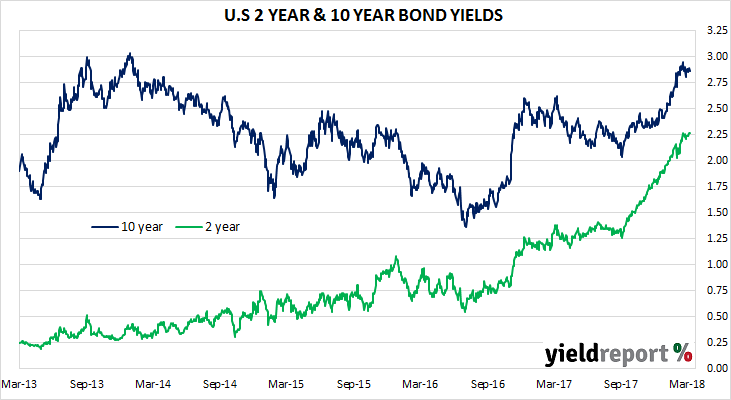

| U.S. 2 year bond% | 2.27 | 2.27 | 0.00 |

| U.S. 10 year bond% | 2.87 | 2.89 | -0.02 |

| U.S. 30 year bond% | 3.13 | 3.16 | -0.03 |

| * Implied yields from Mar 2018 futures | |||

LOCAL MARKETS

Bonds should hold steady today. Europe was stronger, and the U.S. bond market was a little better on the day. Today should be a day of consolidation.

U.S. BOND MARKETS

Bond markets were not quite so, by today’s events. What bond investors have to ponder is why bonds are not breaking through 3%. Today bonds rallied a little but whether they remain bid, only time will tell. There are 10-year and three-year auctions looming and should demand be weak, then bonds could sour and prices driven lower, and yields could press towards 3% again. The problem for many bond traders is that over the last ten years markets have exhibited few bearish traits and volatility has generally fallen to where it was, at one stage, totally benign. That may be about to change and the challenge for many new participants is that most have not traded or invested in a bear market and many are about to see what volatility does.

For many of the bond investors, the perfect storm is being created. Investors have been lulled into a false sense of security through low volatility caused by massive amounts of central bank money which is now being slowly withdrawn and a possible increase in a consumer led inflation as a result of tariffs. Company profits have increased however the tax cuts will be spent on dividends and share buybacks. Balance sheets are not being repaired in fact borrowing is still ongoing to pay for buybacks and dividends rather than capex to lift productivity and R&D to ensure the longevity of the company.

What should be of concern to most investors though are the “bond vigilantes”, because it appears as though they are making a comeback. Investors are querying the level of debt, increasingly significant increases in borrowings and also how the U.S. Government can pay its way. The vigilantes fret about ballooning deficits and if the target of a greater-than-3% growth rate will ever be met. The vigilantes have started to fret about deficits and it is now worth considering that interest expenditure for fiscal September rose to USD$459 billion or 2.4% of GDP, that’s increased from USD$433 billion for 2016. The worry is that with the tax cuts, increasing expenditures and significant increases in issuance (almost triples in 2018 from 2017) the interest cost will balloon and that’s before any rate hikes and increased bond yields have been factored into the equation.

As it stands the three-year auction went off worse than expected at 2.436% the highest auction result since May 2007. The bid to cover was at 2.94 the lowest since November. The ten-year traded 1 bp lower than expected however the bid ratio was lower than the average. The ten-year closed at 2.868%.