Commentary courtesy of Spectrum Asset Management’s Lindsay Skardoon.

| Close | Prev Close |

Change | |

| Aust. 90 day bank bill% | 1.85 | 1.85 | 0.00 |

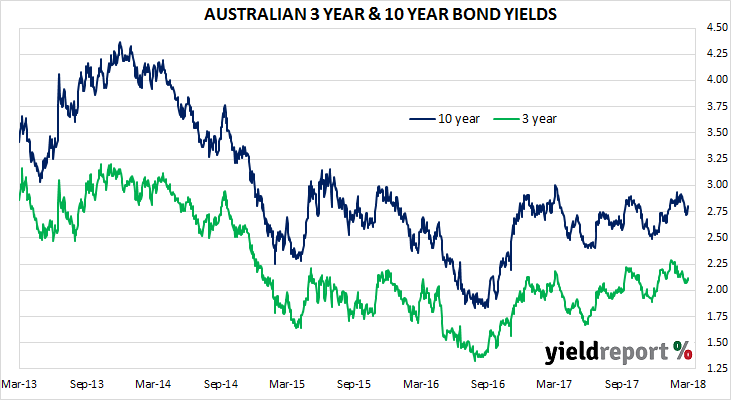

| Aust. 3 year bond%* | 2.11 | 2.10 | 0.01 |

| Aust. 10 year bond%* | 2.79 | 2.78 | 0.01 |

| Aust. 20 year bond%* | 3.20 | 3.19 | 0.01 |

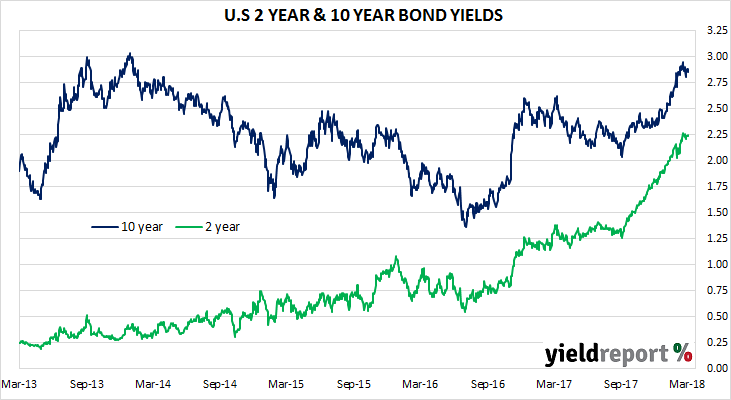

| U.S. 2 year bond% | 2.24 | 2.25 | -0.01 |

| U.S. 10 year bond% | 2.86 | 2.88 | -0.02 |

| U.S. 30 year bond% | 3.12 | 3.15 | -0.03 |

| * Implied yields from Mar 2018 futures | |||

LOCAL MARKETS

With little detail at present, it is hard to know how hard the markets will be hit. This sell-off could take a few days to reach maturity. However, the initial response on the U.S. market, post the release of tariffs, was to rally.

Bonds are likely to follow the U.S. trend and drift. One should expect some selling on the day.

U.S. BOND MARKETS

Yield curve may not invert, but that does not mean the U.S. cannot slip into recession. By way of history, recessions that occurred in the fifties and before the fifties only about 50% were preceded by an inverted yield curve.

The important news of the day though had to do with Draghi. The ECB appears to be relatively confident about European growth. That probably explains why the ECB has been buying fewer bonds and why the pledge to accelerate its bond-buying programme should the economy deteriorate been removed from its release. As the bond-buying programme by the ECB slows this too will impact on U.S. treasuries forcing rates higher again. It will be interesting to see how the carry trade works as for the moment the carry trade is being wound back because every time the U.S. hikes rates, the interest cost rises. Bonds rose on the day and U.S. Treasuries saw yield rise as well due to fears about increased supply.

The implication for markets, however, is that the stimulus provided by the ECB may well end before the end of 2018. That implication will take time to digest and that also spells a tightening of sorts for the U.S. Treasury Market as European investors may choose to buy their own bonds in preference to treasuries.