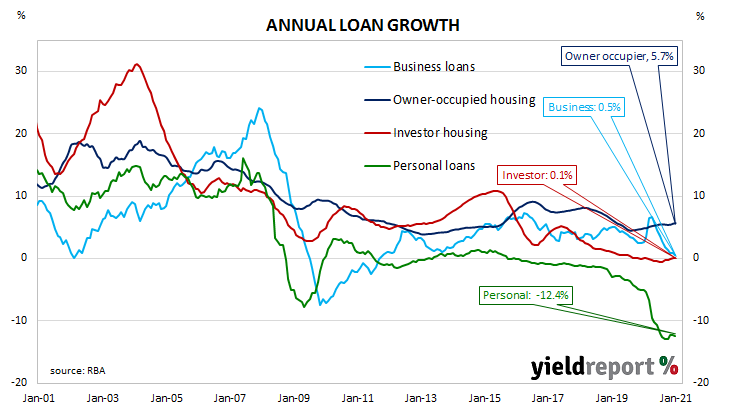

Summary: Private sector credit maintains modest growth rate in January; under expected figure; “slowest annual pace since 2010”; housing credit growth continues but business loans contract; some “encouraging signs”.

The pace of lending to the non-bank private sector by financial institutions in Australia has been trending down since late-2015. Private sector credit growth appeared to have stabilised in the September quarter of 2018 but the annual growth rate then continued to deteriorate through to the end of 2019. The early months of 2020 provided some positive signs but they disappeared in April and have not re-emerged as yet.

According to the latest RBA figures, private sector credit growth continued at a modest rate in January, rising by 0.2%. The result was under the generally expected figure of 0.3%, which also happened to be the size of December’s increase. The annual growth rate slipped from 1.8% in December to 1.7%.

“For 2021, it has been a soft start to the year. That result, matching the outcome for November, is the slowest annual pace since 2010, in the aftermath of the GFC,” said senior Westpac senior economist Andrew Hanlan.

Owner-occupier and investor loans accounted for all the net growth over the month. Business lending contracted and personal debt fell again.

Commonwealth bond yields jumped on the day, broadly following significantly higher US Treasury yields at the close of trading on Friday morning. At the close of business, the 3-year yield ACGB had gained 7bps to 0.37%, the 10-year yield had leaped by 18bps to 1.91% while the 20-year yield finished 12bps higher at 2.57%.

The traditional driver of loan growth rates, the owner-occupier segment, grew by 0.5% over the month, slightly slower than December’s 0.6%. The sector’s 12-month growth rate accelerated from 5.6% to 5.7%.

Growth rates in the business sector remained sluggish and business credit shrank by 0.1%, down from +0.3% in December. The segment’s annual growth rate slowed further, from December’s revised rate of 0.9% to 0.5%.