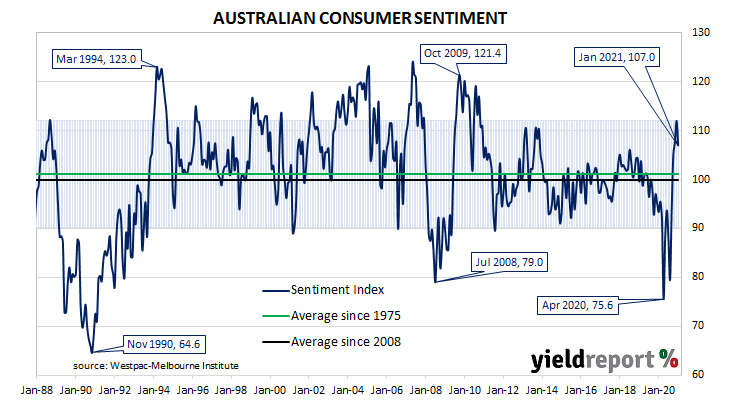

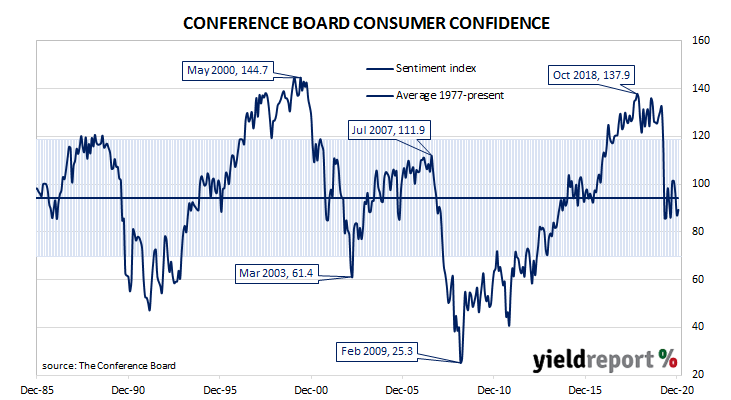

Summary: US consumer confidence rises in January; Conference Board index increases, more than expected; view of present conditions deteriorate, views of future conditions improve; COVID-19 “still the major suppressor”.

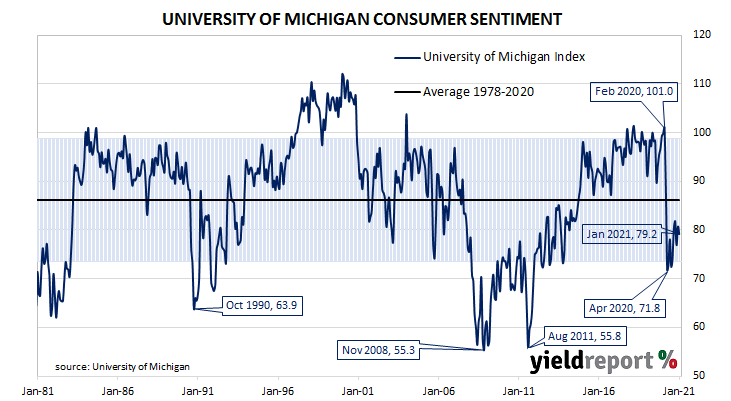

After the GFC in 2008/09, US consumer confidence clawed its way back to neutral over a number of years and then went from strength to strength until late 2018. Measures of consumer confidence then oscillated within a fairly narrow band at historically high levels until they plunged in early 2020. Subsequent readings have oscillated around the long-term average.

The latest Conference Board survey held during the first half of January indicated US consumer confidence has improved compared with the previous month. January’s Consumer Confidence Index registered 89.3, above the median consensus figure of 88.8 and more than December’s final figure of 87.1. Consumers’ views of present conditions declined but their views regarding future conditions improved compared to those held at the time of the December survey.

Lynn Franco, a senior director at The Conference Board, said COVID-19 was “still the major suppressor” of consumers’ views of present conditions but they “foresee conditions improving in the not-too-distant future.”

US Treasury bond yields moved a little each way. By the end of the day, the 2-year yield Treasury bond yield had slipped 1bp to 0.12%, the 10-year yield had inched up 1bp to 1.04% while the 30-year yield finished 1bp lower at 1.79%.

In terms of US Fed policy, expectations of any change in the federal funds rate over the next 12 months maintained a neutral bias. Federal funds futures contracts for January 2022 implied an effective federal funds rate of 0.075%, just under the current spot rate.