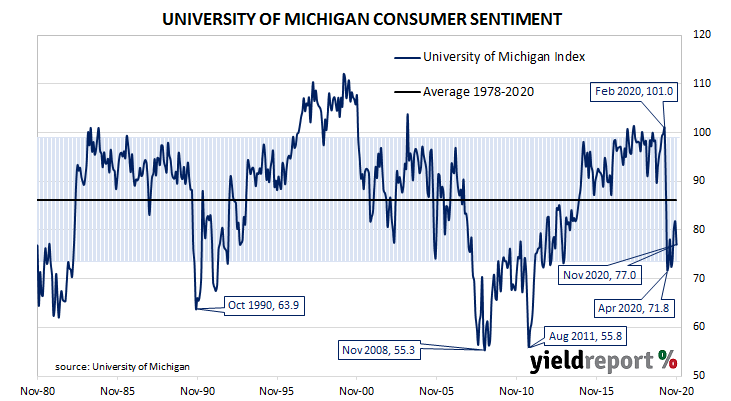

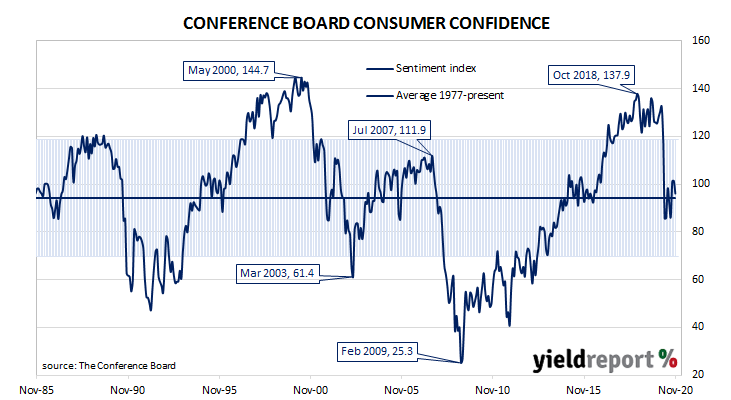

Summary: US consumer confidence lower; Conference Board index falls, less than expected; views of present conditions, future conditions both deteriorate; consumers do not expect economy, labour market gaining strength; reading likely result from COVID-19 resurgence, Republican voter disappointment; survey taken before vaccine news.

After the GFC in 2008/09, US consumer confidence clawed its way back to neutral over a number of years and then went from strength to strength until late 2018. Measures of consumer confidence then oscillated within a fairly narrow band at historically high levels until they plunged earlier this year. Subsequent readings have oscillated around the long-term average.

The latest Conference Board survey held during the first half of November indicated US consumer confidence was lower than in the previous month. November’s Consumer Confidence Index registered 96.1, below the median consensus figure of 98.0 and less than October’s final figure of 101.4. Consumers’ views of present conditions declined slightly but their views regarding future conditions deteriorated more noticeably compared to those held at the time of the October survey.

“Heading into 2021, consumers do not foresee the economy, nor the labour market, gaining strength. In addition, the resurgence of COVID-19 is further increasing uncertainty and exacerbating concerns about the outlook,” said Lynn Franco, a senior director at The Conference Board.

Longer-term US Treasury bond yields rose. By the end of the day, the 10-year Treasury bond yield had gained 3bps to 0.88% and the 30-year yield had increased by 6bps to 1.61%. The 2-year yield finished unchanged at 0.16%.

In terms of US Fed policy, expectations of any change in the federal funds rate over the next 12 months maintained a neutral bias. Federal funds futures contracts for December 2021 implied an effective federal funds rate of 0.07%, just under the current spot rate.

NAB currency strategist Rodrigo Catril put the lower index down “to the resurgence in Covid-19 in the country and disappointment among Republican voters around the election outcome, the mirror image of the post-2016 surge in confidence.” ANZ senior economist Catherine Birch noted the index “fell more than expected in November but the survey was conducted before the vaccine news came out.”