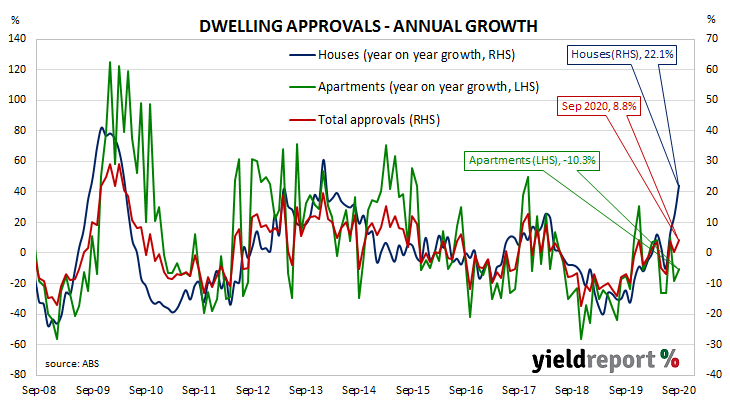

Summary: Home approval numbers increase noticeably; rise considerably more than expected figure; up 8.8% compared to September 2019; no discernible impact from Victoria; “suggests confidence in housing market recovering strongly, despite weak fundamentals”; house, apartment approvals both up; underlying momentum “in reasonably good shape.”

Approvals for dwellings, that is apartments and houses, had been heading south since mid-2018. As an indicator of investor confidence, falling approvals had presented a worrying signal, not just for the building sector but for the overall economy. However, approval figures from late-2019 and the early months of 2020 painted a picture of a recovery taking place, even as late as April. Recent months’ figures have been volatile.

The Australian Bureau of Statistics has released the latest figures from September and total residential approvals increased by 15.4% on a seasonally-adjusted basis. The large rise over the month was considerably more than the 1.5% increase which had been generally expected and in contrast with August’s 2.3% fall after revisions. Total approvals increased by 8.8% on an annual basis, an acceleration from August’s revised figure of 0.7%. Monthly growth rates are often volatile.

“Dwelling approvals came in well above expectations in September with no discernible impact from Victoria’s second wave lockdown and the detail suggesting a strong boost from the Federal Government’s HomeBuilder scheme,” said Westpac senior economist Matthew Hassan.

“Building and lending indicators suggest confidence in the housing market is recovering strongly, despite weak fundamentals including lower population growth and higher unemployment in 2021,” said ANZ economist Adelaide Timbrell. UBS economist George Tharenou raised his 2020 forecast for dwelling commencements from 160,000 to 170,000 after the report.