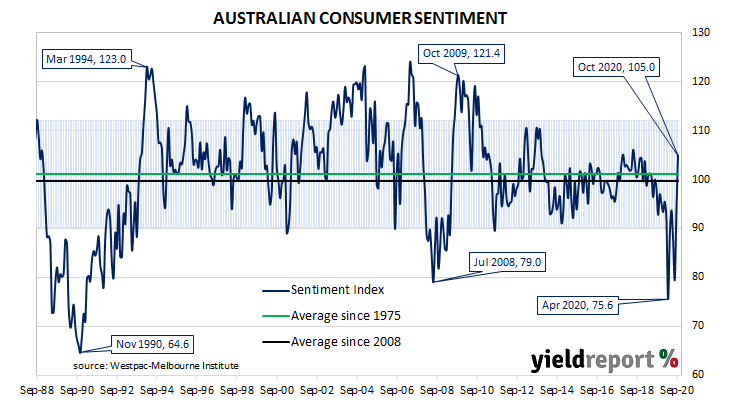

Summary: Leading index improves substantially for second consecutive month in September; reading in line with 12-month average prior to the pandemic; index reading implies annual GDP growth to rise to around +2.25% later this year/early next year; RBA forecast implies 1.3% growth in second half of 2020.

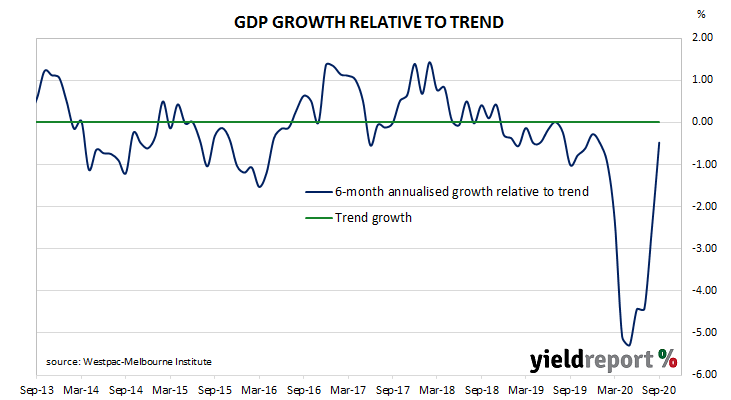

Westpac and the Melbourne Institute describe their Leading Index as a composite measure which attempts to estimate the likely pace of Australian economic growth over the next three to six months. After reaching a peak in early 2018, the index trended lower through 2018, 2019 and the early months of 2020 before plunging to recessionary levels in the second quarter. Readings from the third quarter have been markedly higher.

The latest reading of the six month annualised growth rate of the indicator increased substantially, from August’s revised figure of –2.28% to -0.48% in September.

“While the index growth rate remains negative, it is now well above the lows seen in the first half of the year when the COVID shock saw it drop well below –5%. Indeed, at –0.48%, the latest reading is in line with the average recorded over the twelve months prior to the pandemic,” said Westpac chief economist Bill Evans.

Index figures represent rates relative to trend-GDP growth, which is generally thought to be around 2.75% per annum. The index is said to lead GDP by three to six months, so theoretically the current reading represents an annualised GDP growth rate of around 2.25% in the last quarter of 2020 and/or the first quarter of 2021.

Long-term Commonwealth Government bond yields moved noticeably higher. By the end of the day, 10-year and 20-year ACGB yields both had each increased by 5bps to 0.81% and 1.41% respectively. The 3-year yield remained unchanged at 0.17%.

In the cash futures market, expectations of a change in the actual cash rate, currently at 0.13%, continued to favour a slight easing. At the end of the day, contract prices implied the cash rate would fall below 0.10% in November and then decline a little further before trickling down to 0.035% by mid-2021.

In his opening statement to the House of Representatives Standing Committee on Economics on 14 August, RBA chief Philip Lowe said he expected GDP to contract by 6% over the 2020 calendar year. Taking into account a 7.2% contraction in the first half of 2020, a 6% contraction over the full year implies growth of 1.3% in the second half. Evans expects growth in both the September and December quarters to “be clearly in positive territory…”