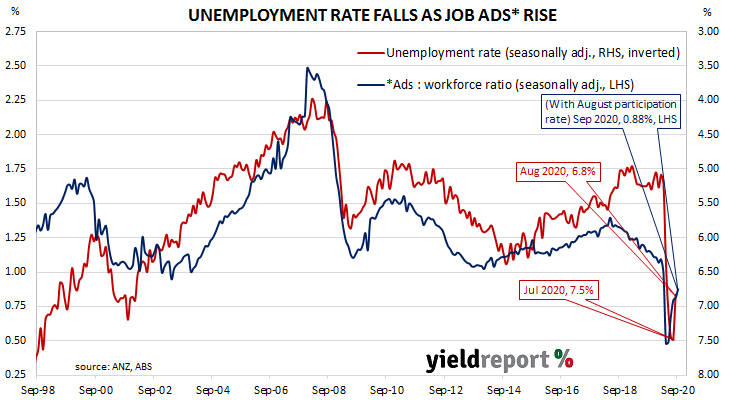

Summary: Job ads increase significantly in September; number of weekly ads increase through month; implies falling jobless rate.

From mid-2017 onwards, year-on-year growth rates in the total number of Australian job advertisements consistently exceeded 10%. That was until mid-2018 when the annual growth rate fell back markedly. 2019 was notable for its reduced employment advertising and this trend continued into the first quarter of 2020. Figures plunged in April as pandemic restrictions took effect but subsequent reports have provided evidence a recovery is taking place.

According to the latest ANZ figures, total advertisements increased by 7.8% in September on a seasonally-adjusted basis. The rise followed a 2.6% increase in August and an 18.7% jump in July after revisions. However, on a 12-month basis, total job advertisements were still 24.8% lower than in September 2019, up from August’s comparable figure of -29.9%.

“There were week-to-week gains throughout the month, which was positive news given the ongoing restrictions in Victoria,” said ANZ senior economist Catherine Birch.

Longer-term Commonwealth bond yields moved higher while short-term yields eased, with the then upcoming 2020/21 Budget and RBA Board meeting weighing on local markets. By the end of the day, the 10-year ACGB yield had inched up 1bp to 0.89% while the 20-year yield finished 5bps higher at 1.47%. The 3-year yield lost 2bps to 0.20%.

The inverse relationship between job advertisements and the unemployment rate has been quite strong (see below chart), although ANZ themselves called the relationship between the two series into question in early 2019. A rising number of job advertisements as a proportion of the labour force is suggestive of lower unemployment rates in the near-future. A falling ratio suggests higher unemployment rates will follow.