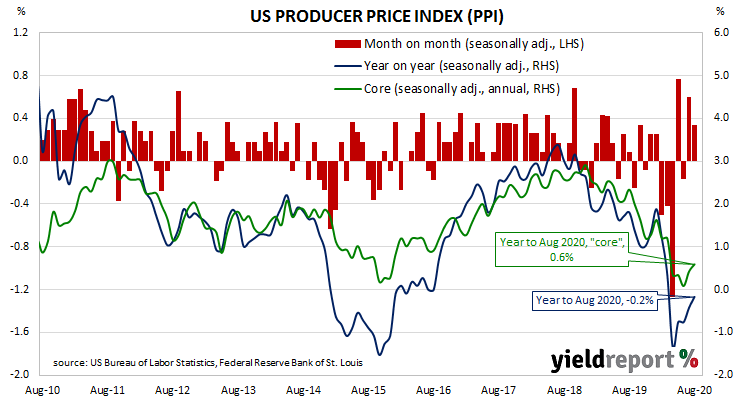

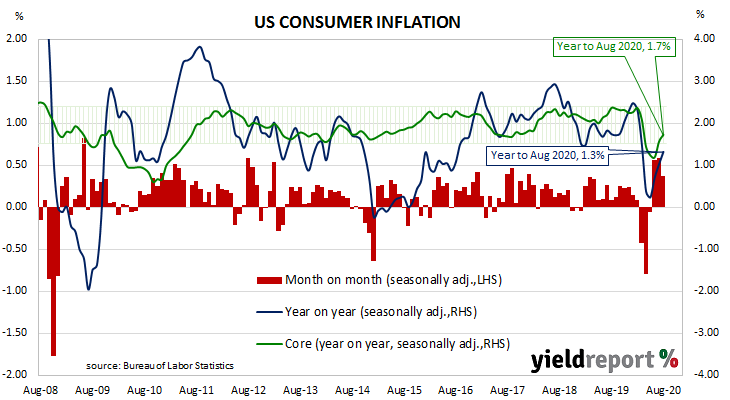

Summary: August CPI increase double expected figure; headline and core figures rise by same amounts; “broad based”, some stability returning to formerly volatile categories; prices of used cars and trucks, fuel up.

The annual rate of US inflation as measured by changes in the consumer price index (CPI) halved from nearly 3% in the period from July 2018 to February 2019. It then fluctuated in a range from 1.5% to 2.0% through 2019 before rising above 2.0% in the final months of that year. “Headline” inflation is known to be volatile and so references are often made to “core” inflation for analytical purposes. Substantially lower rates for both measures were reported from March to May but recent reports indicate consumer inflation has been rekindled.

The latest CPI figures released by the Bureau of Labor Statistics indicated seasonally-adjusted consumer prices increased by 0.4% on average in August. The rise was double the expected figure of 0.2% but less than July’s 0.6% increase. On a 12-month basis, the inflation rate accelerated from July’s rate of 1.0% to 1.3%.

Core inflation, a measure of inflation which strips out the volatile food and energy components of the index, also increased on a seasonally-adjusted basis by 0.4% for the month. The increase was more than the 0.2% rise which had been expected but lower than July’s comparable figure of 0.6%. The seasonally adjusted annual rate ticked up from 1.6% to 1.7%.

“The monthly rise was broad based, with signs that recent gyrations in certain categories are stabilising,” said ANZ economist Hayden Dimes.