Summary: ISM purchasing managers index moves further above 50; reading above consensus expectation; manufacturing continues recovery; employment sub-index still shows “factories are cutting jobs”; US economy growing at fast pace.

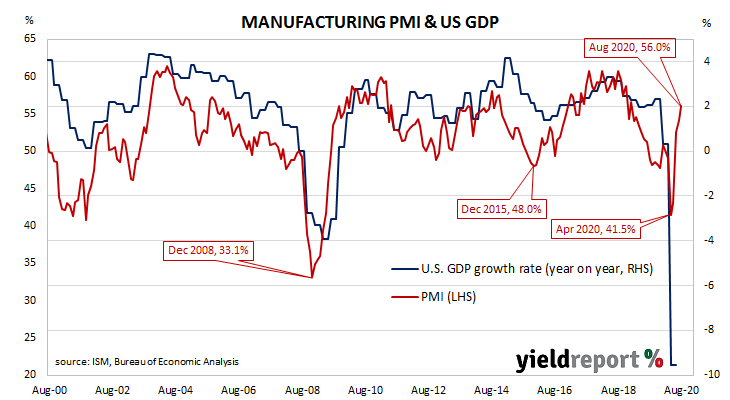

US purchasing managers’ indices (PMIs) reached a cyclical peak in September 2017 before they started a downtrend which stabilised in late 2019 after a truce of sorts was made with the Chinese regarding trade. March’s report signalled a contraction in US manufacturing activity had begun; it stayed in this state until June.

According to the latest Institute of Supply Management (ISM) survey, its Purchasing Managers Index recorded a reading of 56.0% in August. The result was above the expected figure of 54.4% and higher than July’s final reading of 54.2%. The average reading since 1948 is 52.9% and any reading above 50% implies an expansion in the manufacturing sector. A reading “above 42.8%, over a period of time, generally indicates an expansion of the overall economy,” according to the ISM.

“The data confirmed manufacturing has been able to continue its recovery despite the summer surge in COVID-19 infections,” said ANZ analyst Rahul Khare.

Long-term US Treasury yields fell on the day. By the close of business, the 10-year Treasury bond yield had shed 3bps to 0.68% and the 30-year yield had dropped 6bps to 1.42%. The 2-year remained unchanged at 0.12%.

In terms of US Fed policy, expectations of any change in the federal funds rate over the next 12 months retained a slight easing bias. OIS contracts for September implied an effective federal funds rate of 0.074%, about 2bps below the current spot rate.

NAB currency strategist Rodrigo Catril noted the employment sub-index, at 46.4%, “continued to show factories are cutting jobs. So the rebound from very depressed levels continues, but unfortunately we are not yet seeing an improvement strong enough to add new jobs to the US manufacturing sector.”

Purchasing Managers’ Indices (PMIs) are economic indicators derived from monthly surveys of executives in private-sector companies. They are diffusion indices, which means a reading of 50% represents no change from the previous period, while a reading under 50% implies respondents reported a deterioration on average. They are particularly useful as a leading indicator.