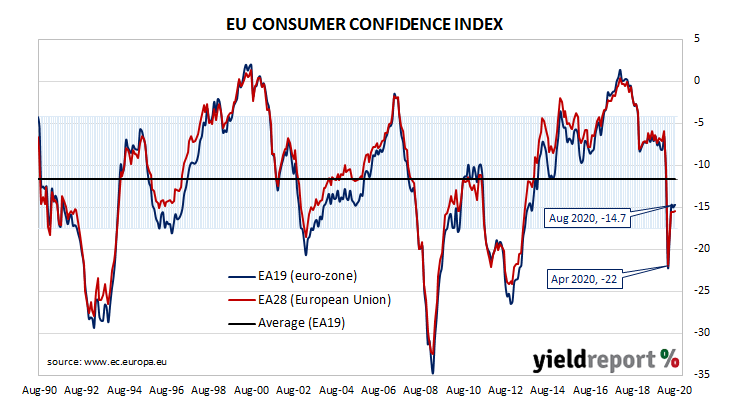

Summary: European Union households slightly less pessimistic in August; confidence index back to June level, above consensus expectation; still significantly below long-term average; euro-zone bond yields largely unchanged.

EU consumer confidence plunged during the GFC and again in 2011/12 during the European debt crisis. Since early 2014, it has been at average or above-average levels, rising to a cyclical peak at the beginning of 2018. Even after it dropped back significantly in late 2018, the index remained at a level which corresponds to significant optimism among households until a substantial drop took place in April 2020. The latest reading indicates households still remain somewhat pessimistic.

The August survey conducted by the European Commission indicated its Consumer Confidence index has crept up to -14.7, the same value as in June. The figure was above the -15.0 which had been expected and a little higher than July’s final figure, also -15.0. The average reading since the beginning of 1985 has been -11.6.

The report had a trivial effect on major European bond markets, the spotlight largely on “flash” Markit PMIs. By the end of the day, the German 10-year bund yield had slipped 1bp to -0.51% while the French 10-year OAT yield remained unchanged at -0.20%.