Summary: Private sector credit contracts for second consecutive month in June; business lending drops noticeably; owner-occupier lending growth slows; investor lending flat; figures consistent with “past recessions and sharp downturns.”

The pace of lending to the non-bank private sector by financial institutions in Australia has been trending down since October 2015. Private sector credit growth appeared to have stabilised in the September quarter of 2018 but the annual growth rate then continued to deteriorate through to the end of 2019. The early months of 2020 provided some positive signs; these disappeared in April.

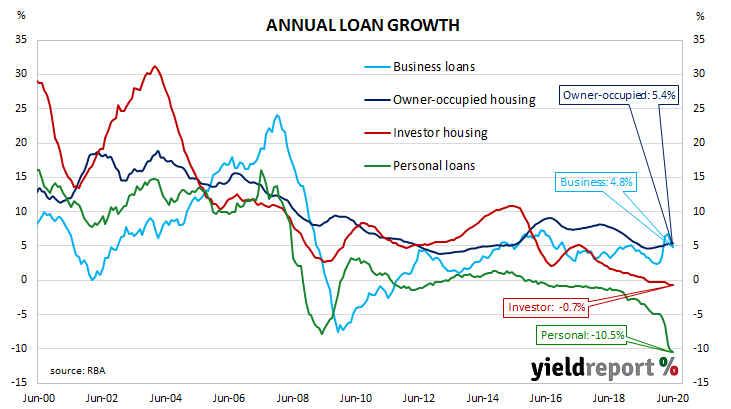

According to the latest RBA figures, private sector credit contracted by 0.2% in June. The result was less than the -0.1% which had been generally expected and less than May’s -0.1%. The annual growth rate slowed to 2.9% from May’s comparable rate of 3.2% after revisions.

“This is the first back-to-back fall since the start of 2009…The cumulative decline of 0.3% is the sharpest drop over a two month period since 1992, during the previous recession,” said Westpac senior economist Andrew Hanlan.

The result was largely driven by a large fall in business loans, with personal debt and investor housing loans also contracting. Owner-occupier loans continued to grow steadily.

Long-term Commonwealth Government bond yields fell harder than their US counterparts had in overnight trading. By the end of the day, the 10-year yield had fallen by 5bps to 0.83% while the 20-year yield finished 6bps lower at 1.41%. The 3-year ACGB yield remained unchanged at 0.30%, 5bps above the RBA’s target yield.

In the cash futures market, expectations of a change in the actual cash rate, currently at 0.13%, continued to remain low. By the end of the day, contracts implied the cash rate would remain in a range of 0.125% to 0.135% through to the latter part of 2021.

The traditional driver of loan growth rates, the owner-occupier segment, grew by 0.3% over the month, lower than May’s revised 0.4%. The sector’s 12-month growth rate remained at 5.4%.