Summary: US consumer confidence retreats in July; index close to April low as US virus infections surge; declines “more likely” in months ahead.

US consumer confidence started 2020 at an elevated level. However, by March, surveys had begun to reflect a growing uneasiness with the global spread of COVID-19 and its reach into the US. After a plunge in April, US household confidence began to recover.

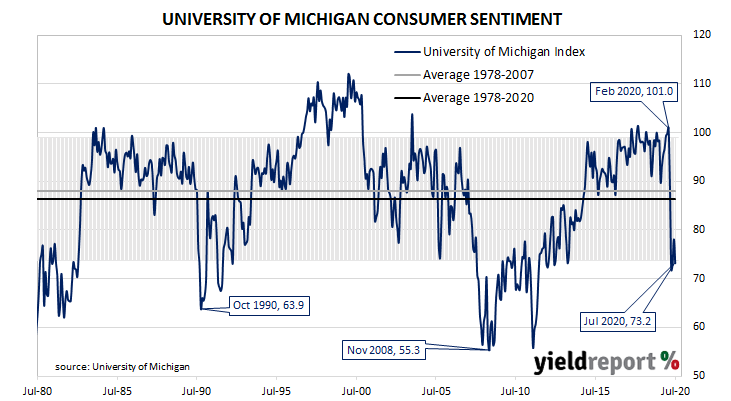

The latest survey conducted by the University of Michigan indicates the average confidence level of US households deteriorated in July after improving in May and June. The University’s preliminary reading from its Index of Consumer Sentiment registered 73.2 in July, less than the expected figure of 80.

The result represented a deterioration from June’s final figure of 78.1. “Consumer sentiment retreated in the first half of July due to the widespread resurgence of the coronavirus,” said the University’s Surveys of Consumers chief economist, Richard Curtin.

Despite the report, US Treasury bond yields moved a little higher. By the end of the day; the US 2-year Treasury yield was unchanged at 0.14%, the 10-year yield had inched up 1bp to 0.63% and the 30-year yield finished 2bps higher at 1.33%.

Curtin was pessimistic in the short-term. “Unfortunately, declines are more likely in the months ahead as the coronavirus spreads and causes continued economic harm, social disruptions, and permanent scarring.” He said “another aggressive fiscal response” by the US government was required “urgently” and without it “another plunge in confidence and a longer recession is likely to occur.”

Less-confident households are generally inclined to spend less and save more; some drop off in household spending could be expected to follow. As private consumption expenditures account for a majority of GDP in advanced economies, a lower rate of household spending growth would flow through to lower GDP growth if other GDP components did not compensate.