Summary: Job ads leap in June; numbers improved steadily over month, as in May; ad numbers still 41% lower than in February; recovery will be “a lot slower”.

From mid-2017 onwards, year-on-year growth rates in the total number of Australian job advertisements consistently exceeded 10%. That was until mid-2018 when the annual growth rate fell back markedly. 2019 was notable for its reduced employment advertising and this trend continued into the first quarter of 2020. April’s numbers set a record of the worst type but subsequent reports have produced a recovery, at least partially.

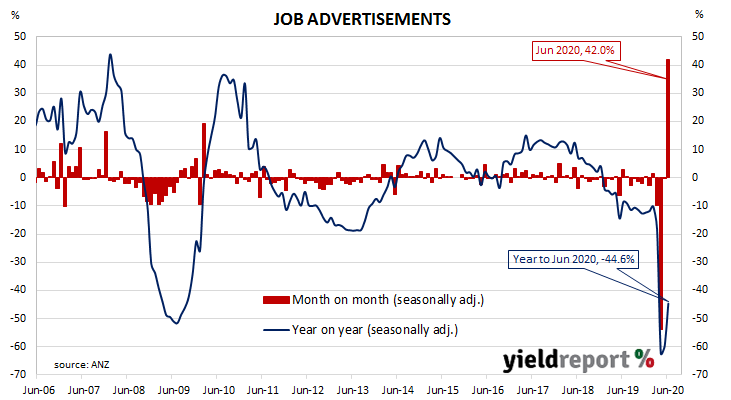

According to the latest ANZ figures, total advertisements increased by 42.0% in June on a seasonally-adjusted basis. The jump followed a 0.3% decline in May and a 53.7% plunge in April after revisions. On a 12-month basis, total job advertisements were 44.6% lower than in June of last year, a significant improvement from May’s comparable figure of -59.9%.

“Week-to-week movements were positive as well, showing consistent improvement throughout the month. This is not overly surprising, given that COVID-19 restrictions continued to ease across most of Australia during June,” said ANZ senior economist Catherine Birch.

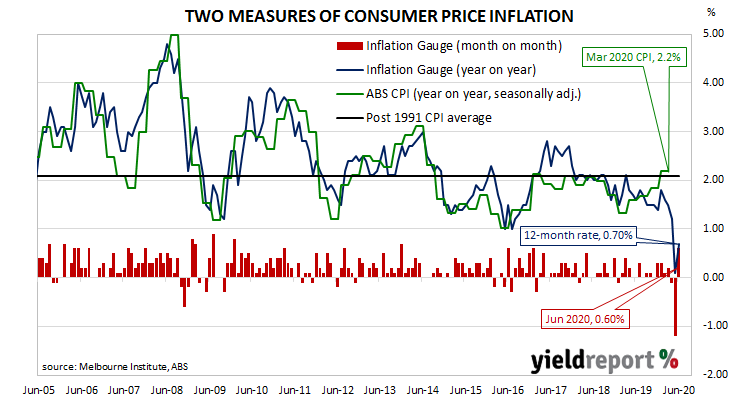

The ANZ report came out on the same day as the Melbourne Institute’s June Inflation Gauge report and long-term Commonwealth bond yields moved modestly higher, ignoring lower US Treasury yields in overnight trading. By the end of the day, the 3-year ACGB yield remained unchanged at 0.30% while 10-year and 20-year yields both finished 2bps higher at 0.94% and 1.58% respectively.

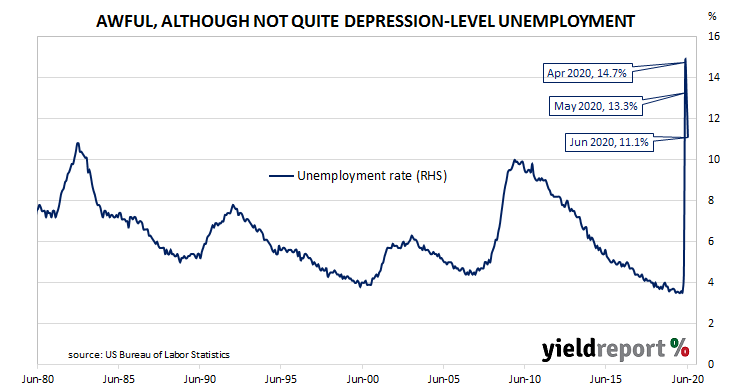

The inverse relationship between job advertisements and the unemployment rate has been quite strong (see below chart), although ANZ themselves called the relationship between the two series into question in early 2019. A rising number of job advertisements as a proportion of the labour force is suggestive of lower unemployment rates in the near future. A falling ratio suggests higher unemployment rates will follow.