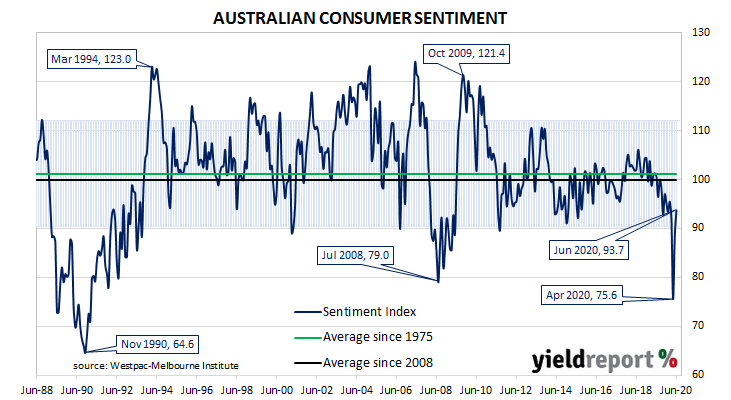

Summary: Household sentiment rises for a second consecutive month; back around pre-pandemic levels but pessimists still outnumber optimists; households anticipate better times ahead.

After a lengthy divergence between measures of consumer sentiment and business confidence in Australia which began in 2014, confidence readings of the two sectors converged again around July 2018. Both readings then deteriorated gradually in trend terms, with consumer confidence leading the way. Household sentiment fell off a cliff in April but it then bounced in May.

According to the latest Westpac-Melbourne Institute survey conducted in the first week of June, average household sentiment has continued to recover from the staggering dive which took place in April. The Consumer Sentiment Index rose from 88.1 to 93.7, taking it back to pre-pandemic levels. UBS economist George Tharenou said, “With sentiment only moderately below average, it’s historically consistent with modestly positive real consumption growth.”

UBS economist George Tharenou said, “With sentiment only moderately below average, it’s historically consistent with modestly positive real consumption growth.”

Any reading below 100 indicates the number of consumers who are pessimistic is greater than the number of consumers who are optimistic. The latest figure is back to the low end of the normal range but it is still noticeably below the long-term average reading of just over 101.

The report came out on the same day as the latest housing finance report. Local Treasury bond yields fell at the long end, broadly following movements in their US Treasury counterparts overnight. By the end of the day, the 3-year ACGB yield was unchanged at 0.28% while the 10-year yield had lost 3bps to 1.01% and the 20-year finished 4bps lower at 1.65%.

In the cash futures market, expectations of a rate cut softened a little for months in the latter part of 2020 and through to late 2021. By the end of the day, July and August contracts implied a rate cut down to zero as 54% and 46% chances respectively, both unchanged from the previous day. September contracts implied a 39% chance of such a move in that month, down from 41%. Contract prices of months in the remainder of 2020 and through to late-2021 implied probabilities ranging between 32% and 45%.