Summary: Melbourne Institute inflation index plummets; annual rate just north of zero; bond yields, cash rates rise anyway.

Despite the RBA’s desire for a higher inflation rate, ostensibly to combat recessions, attempts to accelerate inflation through record-low interest rates have failed to date. In the current environment, the RBA would be satisfied just to avoid deflation. The RBA’s stated objective is to achieve an inflation rate of between 2% and 3%, “on average, over time.” Since the GFC, Australia’s inflation rate has been trending lower and lower and it has been below the RBA’s target band for some years now.

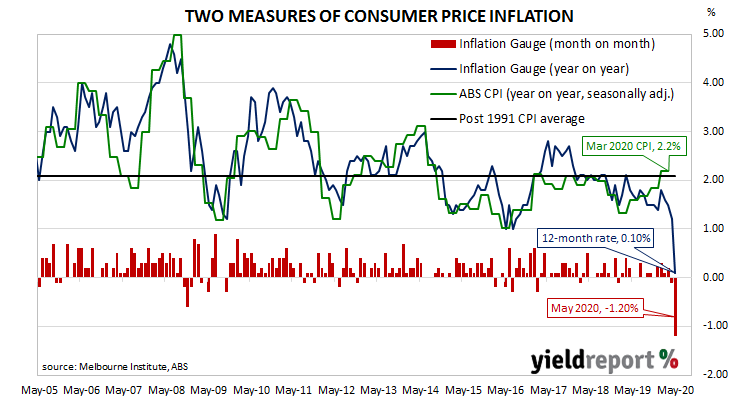

The Melbourne Institute’s latest Inflation Gauge index dropped by 1.2% through May. The large fall follows a 0.1% decline in April and a 0.2% increase in March. On an annual basis, the index increased by just 0.1%, a big fall from April’s comparable rate of 1.2%. Commonwealth Government bond yields moved modestly higher, ignoring lower US Treasury yields in overnight trading. By the end of the day, the 3-year ACGB yield remained unchanged at 0.27%, the 10-year yield had crept up 1bp to 0.89% while the 20-year yield finished 3bps higher at 1.52%.

Commonwealth Government bond yields moved modestly higher, ignoring lower US Treasury yields in overnight trading. By the end of the day, the 3-year ACGB yield remained unchanged at 0.27%, the 10-year yield had crept up 1bp to 0.89% while the 20-year yield finished 3bps higher at 1.52%.

In the cash futures market, expectations of a rate cut softened a touch. By the end of the day, July contracts implied a rate cut down to zero as a 54% chance, down from the previous day’s 57%. August contracts implied a 48% chance of such a move in that month, unchanged from the previous day. Contract prices of months in the remainder of 2020 and through to late-2021 implied probabilities ranging between 33% and 52%.