19 May 2020

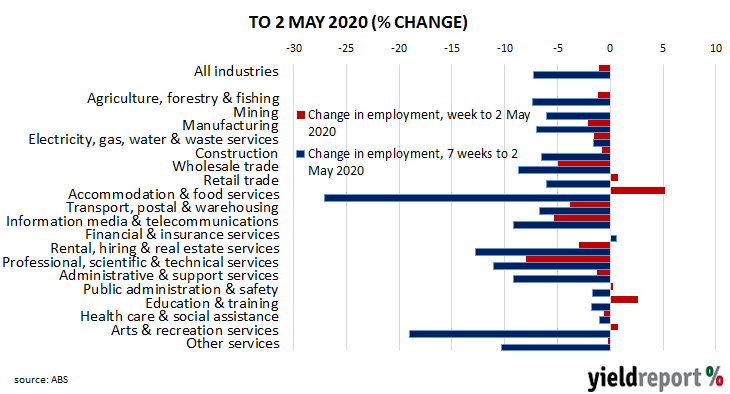

Summary: Job losses continue through to the end of April; JobKeeper programme successful in stemming losses; end of it could see underutilisation rise further.

The ABS has released its latest payroll report containing new statistics on jobs and wages based on Single Touch Payroll data provided by the ATO. Job losses do not directly translate into additional unemployment as some people hold more than one job. The report’s figures are not seasonally adjusted.

Between the week ending 14 March 2020 and the week ending 2 May 2000, the total number of work positions in Australia contracted by 7.3%. Total wages fell by 5.4% over the same seven-week period.

The rate of weekly job losses slowed again. Total jobs fell by 1.1%, another “improvement” when compared with the 1.5% fall in the week ending 18 April. The “Accommodation & food services” and arts/recreation sectors began to see some gains, albeit after suffering heavy losses in previous survey periods. Losses in the “Professional, scientific & technical services” sector admitted it into the ranks of the sectors hardest hit over the past seven weeks.

ANZ senior Head of Australian economics David Plank said the Federal Government’s JobKeeper programme had been successful “in stemming a greater decline in jobs and wages…” However, he noted “there is a risk that the withdrawal of JobKeeper could see underutilisation continue to rise over a longer period…” The underutilisation rate is the sum of the unemployment and underemployment rates and it skyrocketed during April.

15 May 2020

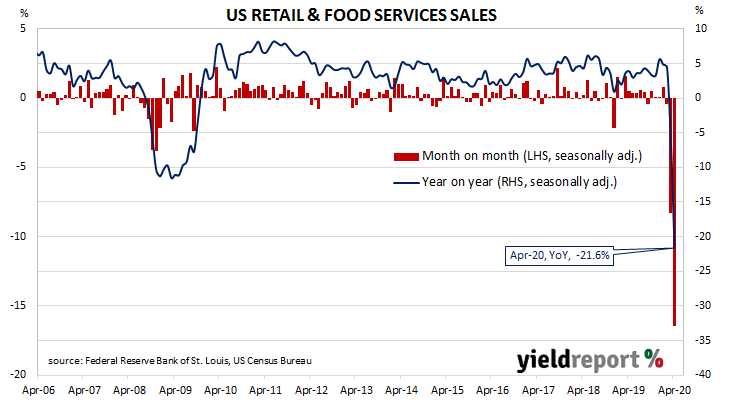

Summary: April retail sales collapse; online sales get boost.

US retail sales had been trending up since late 2015 but, beginning in late 2018, a series of weak or negative monthly results led to a drop-off in the annual growth rate which brought the annual rate below 2.0% by the end of that year. Growth rates then increased in trend terms through 2019 and into early 2020, until restrictions on American households began to take effect in March.

According to the latest “advance” sales numbers released by the US Census Bureau, total retail sales contracted by 16.4% in April. The fall was a much greater one than the -11% which had been expected and it was of a greater magnitude than March’s revised figure of -8.3%. On an annual basis, the growth rate fell to -21.6% from March’s revised rate of -5.7%.

The report came out on the same day as reports on job openings (JOLTS), consumer sentiment and industrial production numbers. US Treasury bond yields finished higher; the US 2-year Treasury yield remained unchanged at 0.15% while 10-year and 30-year yields both finished 4bps higher to 0.65% and 1.33% respectively.

In terms of US Fed policy, expectations of any change in the federal funds rate over the next 12 months remained fairly soft. However, OIS contracts from March 2021 onwards continued to imply a zero effective federal funds rate even after US Fed chief Jerome Powell recently repeated the Fed’s reluctance to embrace negative rates.

15 May 2020

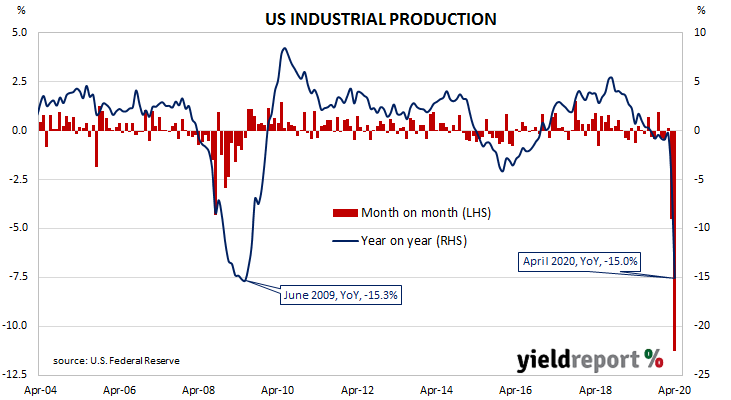

Summary: US output drop larger than March fall; at GFC level; capacity utilisation hits 50-year low.

The Federal Reserve’s industrial production (IP) index measures real output from manufacturing, mining, electricity and gas company facilities located in the United States. These sectors are thought to be sensitive to consumer demand and so some leading indicators of GDP use industrial production figures as a component.

Figures from early-2020 had been suggestive of a possible end to a downtrend which began in late-2018. However, the latest report makes March’s awful figures seem relatively “good”.

According to April figures, US industrial production contracted by 11.2%, roughly in line with the -11.4% which had been expected but also a severe deterioration from March’s revised figure of -4.5%. On an annual basis, the growth rate plunged from March’s revised figure of -4.9% to -15.0%.

The report came out on the same day as reports on retail sales, job openings (JOLTS) and consumer sentiment. US Treasury bond yields finished higher; the US 2-year Treasury yield remained unchanged at 0.15% while 10-year and 30-year yields both finished 4bps higher to 0.65% and 1.33% respectively.

In terms of US Fed policy, expectations of any change in the federal funds rate over the next 12 months remained fairly soft. However, OIS contracts from March 2021 onwards continued to imply a zero effective federal funds rate even after US Fed chief Jerome Powell recently repeated the Fed’s reluctance to embrace negative rates.

15 May 2020

Summary: US quits down; job openings down; total separations up; accommodation & food sales hit hardest

The number of US employees who quit their jobs as a percentage of total employment increased slowly but steadily after the GFC. It peaked in August 2018, stabilised and then remained largely unchanged through the remainder of 2018 before it hit a new peak in July 2019. It then tracked sideways until virus containment measures were introduced in March.

Figures released as part of the most recent JOLTS report show the quit rate has dropped away considerably from just under the record levels reached in July 2019. 1.8% of the non-farm workforce left their jobs voluntarily in March, a marked fall from February’s revised figure of 2.3%.

Quit numbers increased in the “Mining & logging” sector but all other sectors experienced declines, with the largest monthly falls coming from the “Accommodation & food services” and “Retail trade” sectors. Overall, the total number of quits for the month decreased from February’s revised figure of 3.436 million to 2.782 million in March.

Surprisingly, the recent April non-farm payroll report indicated average hourly pay had jumped from USD$28.67 to USD$30.01, a 4.7% increase over the month and a 7.9% increase on April 2019’s comparable number. One explanation is the average pay rate increased as lower-paid jobs bore the brunt of layoffs, thus reducing their influence on the overall average.

Total vacancies at the end of March fell by 813,000, or 11.6%, from February’s revised figure of 7.004 million to 6.191 million, driven by decreases in the “Accommodation and food services” and “Professional and business services” sectors. Overall, 17 out of 19 sectors experienced fewer job openings than in the previous month.

Total separations during the same period increased by 8.922 million from February’s revised figure of 5.595 million to 14.106 million. As with vacancies figures, the increase was led by the “Accommodation and food services” sector, with the “Other services” sector also providing a significant source of job losses. The only sector to reduce separations was the US Federal Government.

15 May 2020

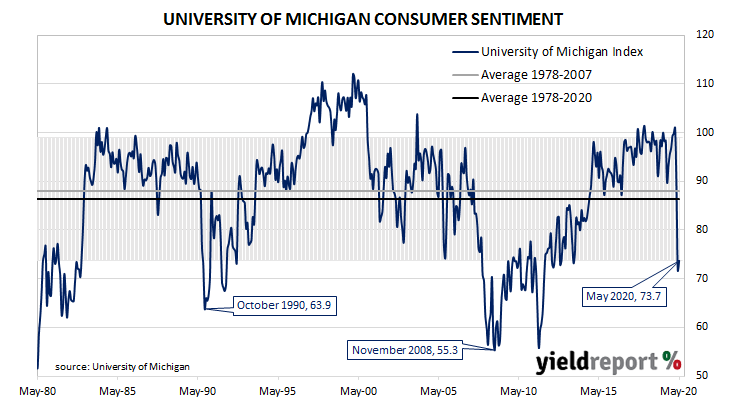

Summary: US consumer confidence improves slightly; still under the lower bound of “normal”; inflation expectations rise despite depressed state of the economy.

US consumer confidence started 2019 at well-above-average levels in a longer-term context, although readings were markedly lower than those which had been typical of most of the previous year. During the rest of 2019, US households maintained historically-high levels of confidence except for two short-lived dips. 2020 started reasonably well but that changed in April.

The latest survey conducted by the University of Michigan indicates the average confidence level of US households improved a little while remaining at depressed levels. The University’s preliminary reading from its Index of Consumer Sentiment registered 73.7 in May, better than the expected figure of 67.5 and a slight rise from April’s final figure of 71.8.

The University’s Surveys of Consumers chief economist, Richard Curtin, said discounted prices and low interest rates had “partially offset” income uncertainty. However, he noted short-term expectations had continued to deteriorate even as households’ perceptions of current conditions improved. “Despite these gains, personal financial prospects for the year ahead continued to weaken, falling to the lowest level in almost six years, with declines especially sharp among upper income households.”

The report came out on the same day as a reports on retail sales, job openings (JOLTS) and industrial production numbers. US Treasury bond yields finished higher; the US 2-year Treasury yield remained unchanged at 0.15% while 10-year and 30-year yields both finished 4bps higher to 0.65% and 1.33% respectively.

In terms of US Fed policy, expectations of any change in the federal funds rate over the next 12 months remained fairly soft. However, OIS contracts from March 2021 onwards continued to imply a zero effective federal funds rate even after US Fed chief Jerome Powell recently repeated the Fed’s reluctance to embrace negative rates.

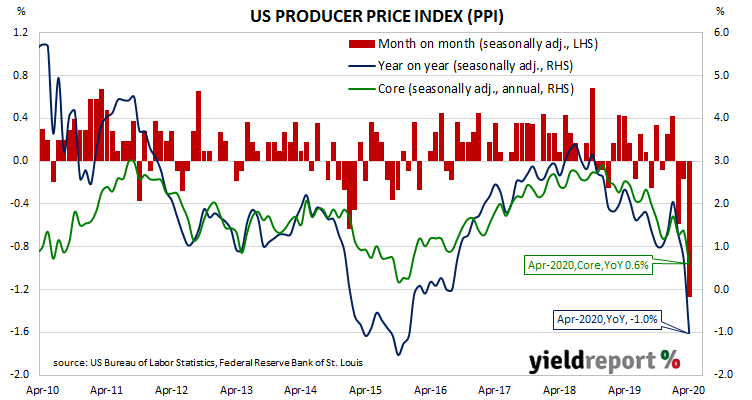

13 May 2020

Summary: Prices received by producers tumble; fall much more than expected; driven by 56.6% fall in petrol price; federal funds rate forecast to fall in 2021 despite Fed reluctance.

Around the end of 2018, the annual inflation rate of the US producer price index (PPI) began a downtrend which then continued through 2019. Months in which prices received by producers increased suggested the trend may have been coming to an end, only for it to continue. There’s really no doubt now.

April figures published by the Bureau of Labor Statistics indicate producer prices dropped by 1.3% after seasonal adjustments. The fall was much harder than the 0.4% decline which had been generally expected and considerably larger in magnitude than March’s -0.2%. On a 12-month basis, the rate of producer price inflation after seasonal adjustments reversed at 1.0% after recording 0.7% in March and 1.3% in February.

“Core” PPI inflation fell by 0.3%, more than just reversing March’s 0.2% increase. The annual rate more than halved from 1.4% to 0.6%.

US Treasury bond yields finished a little lower. By the end of the day, the US 2-year Treasury yield finished unchanged at 0.16% while 10-year and 30-year yields each shed 2bps to 0.65% and 1.35% respectively.

Expectations of any change in the federal funds rate over the next 12 months remained negligible, especially after a speech given by US Fed chief Jerome Powell later that same day. However, OIS contracts from March 2021 onwards continued to imply a zero effective federal funds rate.

13 May 2020

Summary: Euro-zone industrial production suffers huge contraction in March; monthly figure better than consensus estimate; large economies hit hard.

As with other countries’ measures of industrial production, Eurostat’s industrial production index measures the output and activity of industrial sectors in euro-zone countries in aggregate. Following a recession in 2009/2010 and the debt-crisis of 2010-2012 which flowed from it, euro-zone industrial production recovered and then reached a peak four years later in early-2016. Growth rates then fell and recovered through 2016/2017 before beginning a steady and persistent slowdown from the start of 2018. That decline has now turned into a plunge.

According to the latest figures released by Eurostat, euro-zone industrial production contracted by a seasonally-adjusted 11.3% in March. The fall was not as much as the -12% which had been expected but it was still a massive extension on February’s 0.1% decline. On an annual basis, seasonally-adjusted growth in industrial production also plunged from February’s revised rate of -1.9%, registering -12.8%*.

Industrial production fell by double-digit percentages across all four of the largest euro-zone economies. Germany’s industrial production decreased by 11.2%, Spain shrank by 11.9%, France’s comparable rate was -16.4%. Italy’s production collapsed by 28.4%.

French and German 10-year bond yields both eased just a little as the figures had been largely factored in prior to the report’s release. By the close of business, yields on German 10-year bunds and French 10-year OATs had each shed 2bps to -0.53% and -0.05% respectively.

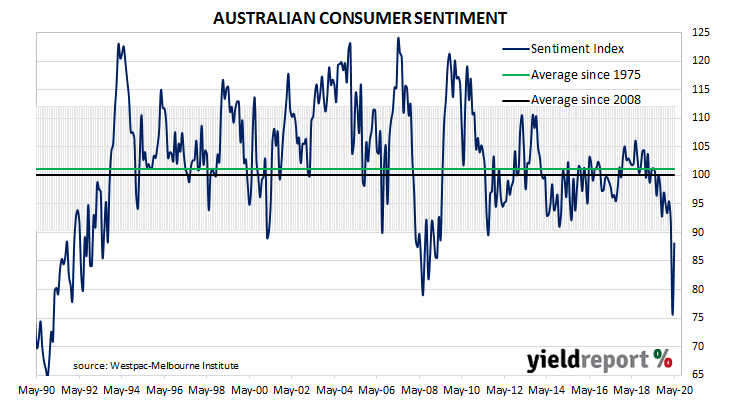

13 May 2020

Summary: Household sentiment bounces after April plunge; number of pessimistic consumers greater than optimistic consumers; Westpac-Melbourne Institute index at 2008/2009 levels

After a lengthy divergence between measures of consumer sentiment and business confidence in Australia which began in 2014, confidence readings of the two sectors converged again around July 2018. Both readings then deteriorated gradually in trend terms, with consumer confidence leading the way. Household sentiment fell off a cliff in April but May’s figures have marked a reduction in pessimism.

According to the latest Westpac-Melbourne Institute survey conducted in the first full week of May, average household sentiment partially recovered from the staggering dive which took place in April. The Consumer Sentiment Index rebounded from 75.6 to 88.1, taking it back to a level on par with some of the readings from 2008 and 2009 when the GFC was unfolding.

Westpac chief economist Bill Evans said, “The May turnaround marks the biggest monthly gain in the Index since the survey began nearly fifty years ago. That has gone a long way towards reversing the record monthly fall we saw last month.”

Any reading below 100 indicates the number of consumers who are pessimistic is greater than the number of consumers who are optimistic. The latest figure is still below the low end of the normal range and it is substantially below the long-term average reading of just over 101.

The report came out on the same day as the latest quarterly wage cost indices. Local Treasury bond yields were almost unchanged, ignoring moderate falls in US Treasury markets overnight. By the end of the day, the 3-year ACGB yield had inched up 1bp to 0.24% while 10-year and 20-year yields finished unchanged at 0.95% and 1.61% respectively.

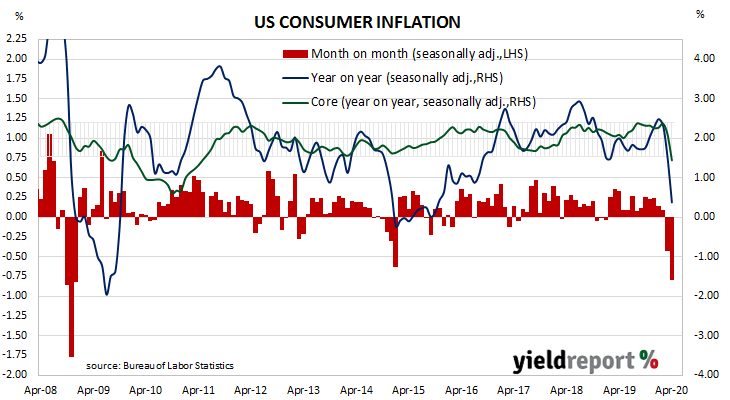

12 May 2020

Summary: April CPI figures fall at GFC-type rates; food and medical prices up while fuel prices drop; core inflation falls more than expected.

The annual rate of US inflation as measured by changes in the consumer price index (CPI) halved from nearly 3% in the period from July 2018 to February 2019. It then fluctuated in a range from 1.5% to 2.0% through 2019 before rising above 2.0% in the final months of that year. “Headline” inflation is known to be volatile and so references are often made to “core” inflation for analytical purposes. Substantially lower rates for both measures are now starting to be reported.

The latest CPI figures released by the Bureau of Labor Statistics indicated seasonally-adjusted consumer prices decreased by 0.8% on average in April. The fall was lower than the 0.7% fall which had been expected and a larger drop than the -0.4% recorded in March. On a 12-month basis, the inflation rate slowed from March’s annual rate of 1.5% to 0.4%.

Core inflation, a measure of inflation which strips out the volatile food and energy components of the index, decreased on a seasonally-adjusted basis by 0.4% for the month. This was a larger drop than the -0.2% which had been expected and less than March’s -0.1%. The annual rate slowed from 2.1% in March to 1.4%, seasonally adjusted.

ANZ economist Daniel Been said the report “highlighted the scale of the deflationary shock to hit the economy” which he predicted “will be a major focus for the US Fed going forward.”

US Treasury bond yields fell moderately. The 2-year yield shed 2bps to 0.16%, the 10-year yield lost 4bps to 0.67% and the 30-year yield finished 5bps lower at 1.37%.

In terms of likely US monetary policy, expectations of any change in the federal funds rate over the next 12 months remained negligible. However, March 2021 OIS contracts implied a zero effective federal funds rate.

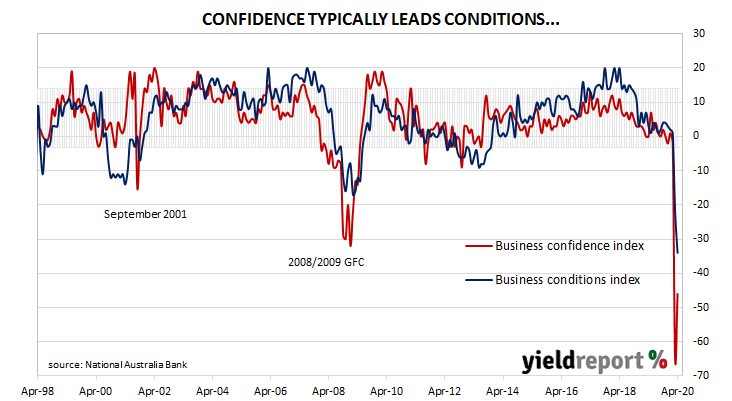

12 May 2020

Summary: Business confidence bounce in April after March’s plunge; business conditions dropped heavily again; capacity usage drops; capex spending down in an attempt to conserve cash.

NAB’s business survey indicated Australian business conditions were robust in the first half of 2018, with a cyclical-peak reached in April of that year. Readings from NAB’s conditions index then began to slip and, by the end of 2018, they had dropped to below-average levels. Forecasts of a slowdown in the domestic economy began to emerge in the first half of 2019 and NAB’s business confidence index began trending lower, with the conditions index following. In March 2020, vastly lower readings began to reflect coronavirus containment measures.

According to NAB’s latest monthly business survey of 400 firms conducted in the last week of April, business conditions extended on March’s drastic fall. NAB’s conditions index registered -34, down from March’s revised reading of -22.

NAB chief economist Alan Oster said, “Business conditions weakened further in April and are now well below the levels seen in the GFC”. Westpac senior economist Andrew Hanlan noted the conditions index reading “is approaching the early 1990s recession low, -38.8.”

However, business confidence rebounded, albeit back to a still-recessionary level. NAB’s confidence index rose from March’s revised reading of -65 to -46. Typically, NAB’s confidence index leads the conditions index by approximately one month, although some divergences appear from time to time. NAB’s Oster said the improvement “was broad based” while remaining “deeply negative across all industries and states.”

US Treasury bond yields increased by moderate amounts in overnight trading but local Treasury yields largely ignored the increases and had a quiet day. By the end of it, 3-year and 10-year ACGB yields both remained unchanged at 0.23% and 0.95% respectively while the 20-year yield finished 2bps higher at 1.61%.

US Treasury bond yields increased by moderate amounts in overnight trading but local Treasury yields largely ignored the increases and had a quiet day. By the end of it, 3-year and 10-year ACGB yields both remained unchanged at 0.23% and 0.95% respectively while the 20-year yield finished 2bps higher at 1.61%.